How the Federal Reserve's Upcoming Rate Cut Could Transform the Housing Market

As we dive into September, all eyes are fixated on the Federal Reserve (often referred to as the Fed). There’s a strong buzz that a Federal Funds Rate cut is on the horizon, mainly fueled by recent signs showing inflation cooling and the job market showing some signs of slowdown. Mark Zandi, Chief Economist at Moody’s Analytics, recently stated:

“They’re ready to cut, just as long as we don’t get an inflation surprise between now and September, which we won’t.”

But what does this mean for the housing market, especially for you as a potential buyer or seller? Let’s break it down.

Why a Federal Funds Rate Cut Matters

The Federal Funds Rate is a pivotal driver of mortgage rates, though it’s not the only player in the game. Factors like the overall economy and geopolitical uncertainties also come into play. When the Fed lowers the Federal Funds Rate, it sends a clear message about the economic landscape, and mortgage rates usually respond accordingly.

While a single rate cut might not lead to an immediate plummet in mortgage rates, it can contribute to a gradual decline that’s already in motion. As Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), aptly puts it:

“Once the Fed kicks off a rate-cutting cycle, we do expect that mortgage rates will move somewhat lower.”

And it’s crucial to note that this anticipated Federal Funds Rate cut likely won’t be a one-off occurrence. According to Lawrence Yun, Chief Economist at the National Association of Realtors (NAR):

“Generally, the rate-cutting cycle is not one-and-done. Six to eight rounds of rate cuts all through 2025 look likely.”

Projected Impacts on Mortgage Rates

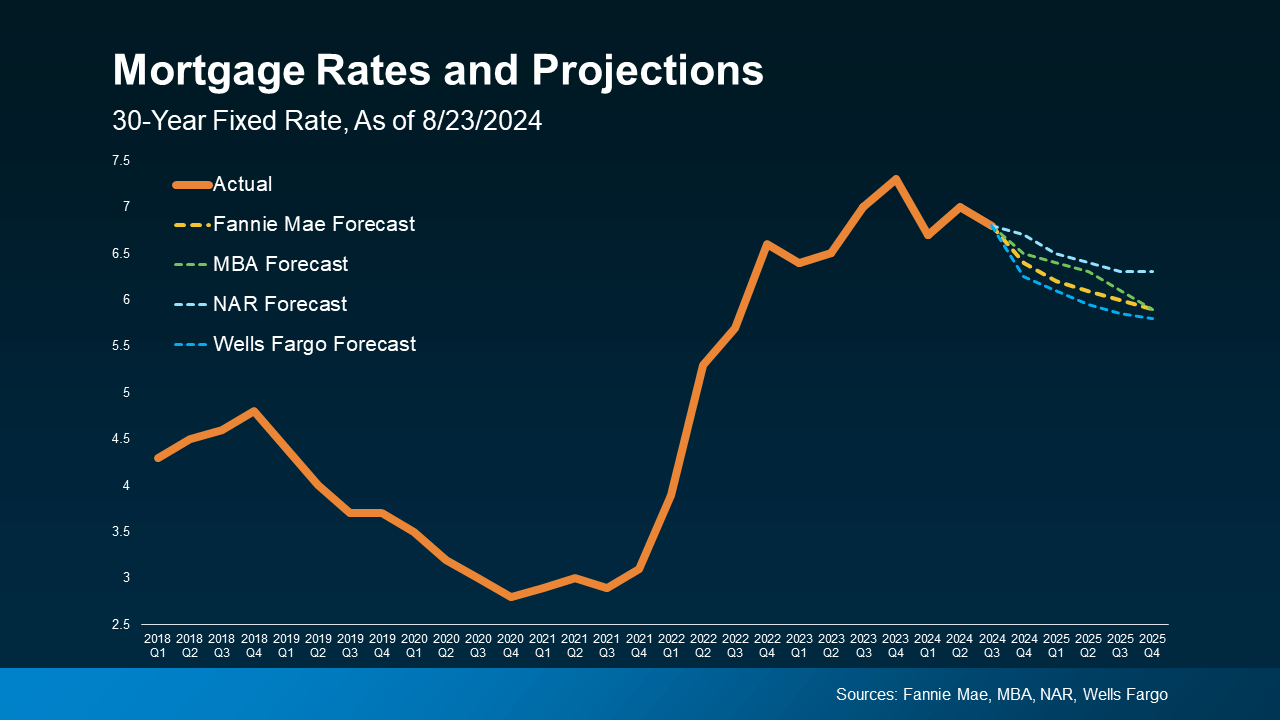

So, what do experts predict for mortgage rates as we look ahead to 2025? With the expected cuts from the Fed, we can anticipate a continued gradual decline in mortgage rates. While a visual graph would typically accompany these insights, let’s stick to the main takeaways.

With the recent easing of inflation and indications of a cooling job market, a Federal Funds Rate cut is set to positively influence mortgage rates. Here are two significant reasons why this is great news for both buyers and sellers:

1. Easing the Lock-In Effect

Current homeowners may feel “locked-in” due to higher current rates compared to their original mortgages. This “lock-in effect” can deter homeowners from selling, fearing they’ll lose their lower-rate mortgages. A slight reduction in rates could change the game, making selling more attractive once again.

However, don’t expect a massive influx of sellers hitting the market. Many homeowners might still hesitate to part ways with their existing mortgage rates.

2. Boosting Buyer Activity

For prospective homebuyers, any dip in mortgage rates will make the housing market feel much more inviting. Lower rates can significantly decrease the overall cost of homeownership, making it a more feasible option if you’ve been biding your time.

What Should You Do?

While we may not see drastic reductions in mortgage rates right away, the anticipated Federal Funds Rate cut will likely contribute to the ongoing gradual decrease.

As the housing market shifts, it's vital to evaluate your personal situation. Jacob Channel, Senior Economist at LendingTree, puts it succinctly:

“Timing the market is basically impossible. If you’re always waiting for perfect market conditions, you’re going to be waiting forever. Buy now only if it’s a good idea for you.”

Bottom Line

The projected Federal Funds Rate cut, spurred by improving inflation and a slowing job market, is poised to have a beneficial, albeit gradual, impact on mortgage rates. This shift could unlock new opportunities for you in the housing market.

Whenever you feel ready to make a move, let’s connect. Being prepared is key, so when the moment is right, you’ll be poised to take action!

Recent Posts

GET MORE INFORMATION