Mortgage Approval Just Got Easier: Here’s What Every Homebuyer Should Know Right Now

Are you sitting on the sidelines, waiting for the “right time” to buy a home? Maybe you’ve been telling yourself, “I probably won’t even qualify for a mortgage, so why bother?” Well, here’s the truth: getting approved for a home loan isn’t as out of reach as you might think. In fact, it’s getting easier—and that could be your cue to jump in.

Let’s break down what’s really happening in the mortgage world right now, why it matters, and what it means for you.

Mortgage Approval Is No Longer Mission Impossible

For a while, mortgage lenders were locked up tighter than a vault. And with good reason—nobody wanted a repeat of the 2008 housing crisis. But in 2025, things are shifting. Lending standards are still responsible, yes, but for qualified buyers? The doors are opening.

Lenders are slowly loosening the reins and making it easier for people with solid finances to get approved. That includes folks with slightly lower credit scores or modest down payments. Translation? If you’ve been waiting for the “perfect” lending climate, this might just be it.

Credit Is Becoming More Accessible—But Still Controlled

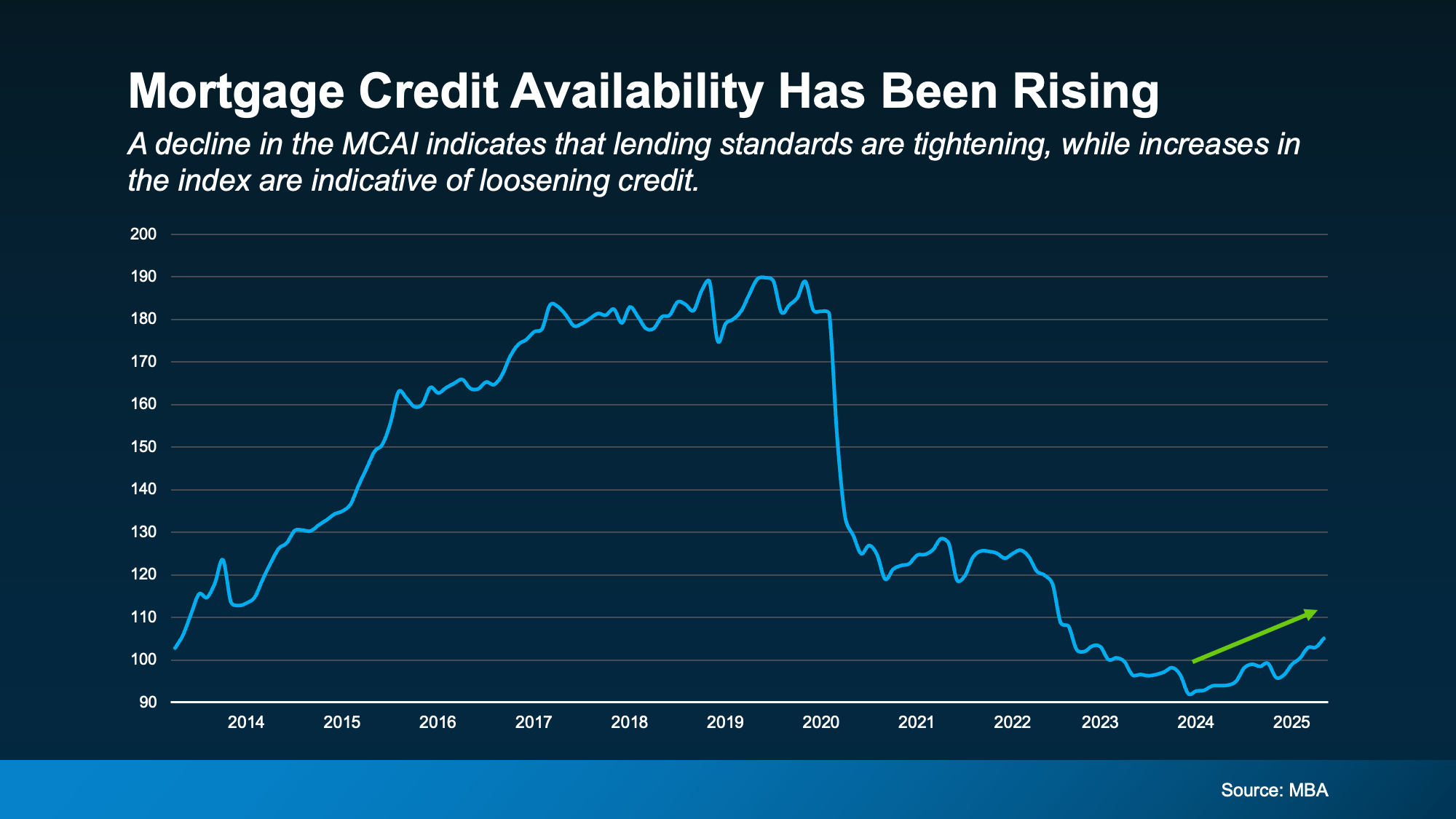

Think of mortgage lending like a faucet: in 2008, it was on full blast—too much, too fast. Then the crash happened, and the faucet was turned off almost completely. Now? It’s flowing again, but just enough to fill the glass without overflowing.

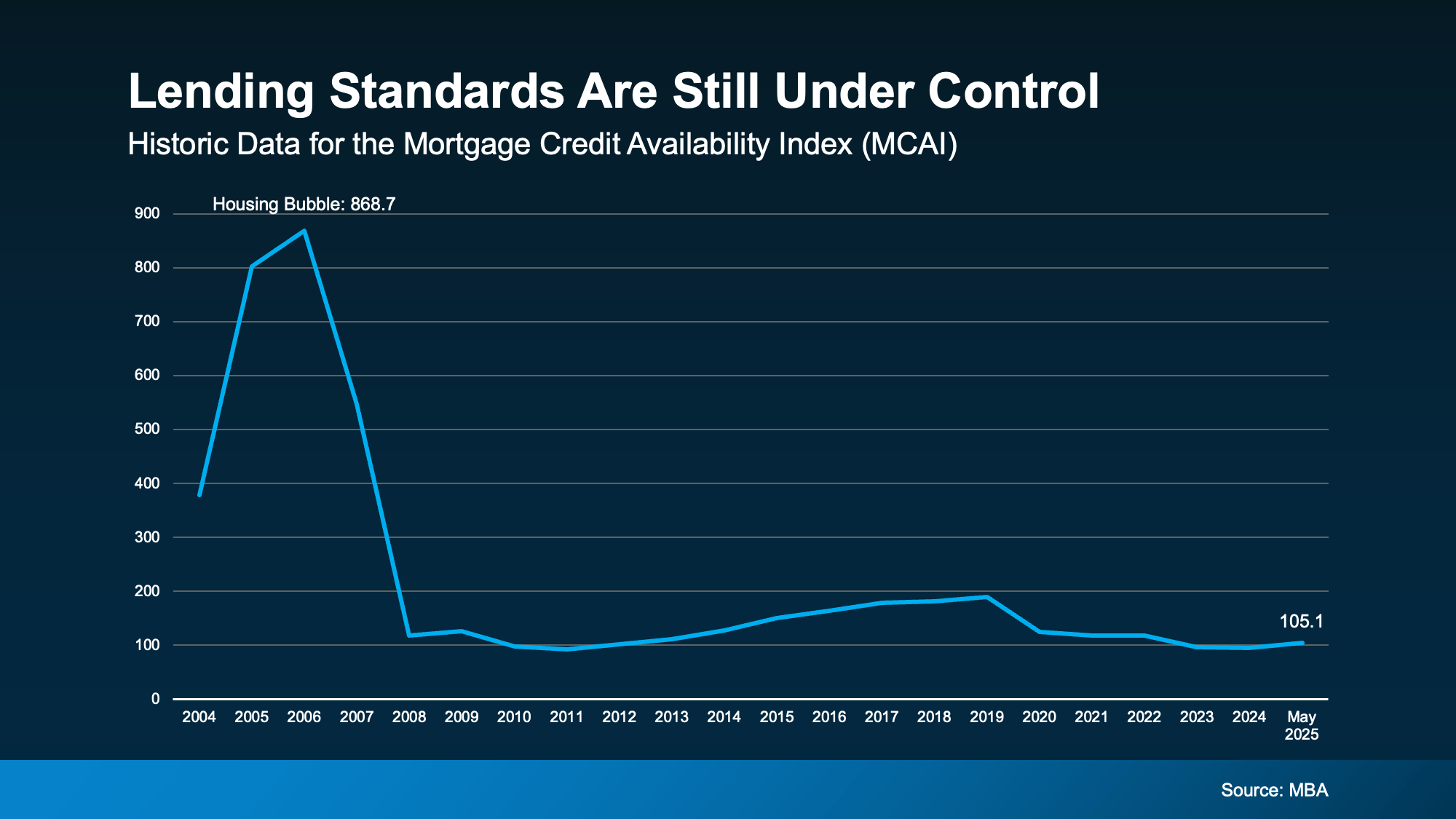

According to the Mortgage Bankers Association (MBA), their Mortgage Credit Availability Index (MCAI)—which tracks how easy or hard it is to get a mortgage—is climbing. In May, it hit its highest point since August 2022. That’s a strong indicator that banks are becoming more flexible, without being reckless.

What Does This Mean For You?

Let’s cut to the chase: if you’ve been worried that your financial profile isn’t “perfect,” this trend could work in your favor. As mortgage credit availability increases, so do your chances of approval.

The National Association of Mortgage Underwriters (NAMU) even confirmed it:

“Mortgage credit availability surged in May, reaching its highest level since August 2022. The uptick signals that lenders are increasingly willing to loosen underwriting standards, providing borrowers with greater access to financing options.”

So whether you’re a first-time buyer or someone looking to move or refinance, this might be the break you’ve been waiting for.

But Wait—Isn’t This How We Got Into Trouble in 2008?

Great question. And no, we’re not walking into another financial firestorm.

Yes, looser lending standards were a big reason behind the 2008 housing collapse. But here’s the difference: today’s lending environment is way more cautious. Even with the recent easing, standards are still nowhere near the risky levels we saw before the crash.

In fact, if you look at MCAI data going back to 2004, today’s credit availability is significantly lower than the pre-crisis peak. That means lenders are still thoroughly vetting buyers. They’re just not slamming the door on anyone who doesn’t have a flawless credit report.

Why Lenders Are Making This Move Now

You might be wondering—why the change?

It’s all about momentum. The real estate market needs movement. When buyers can access loans more easily, they buy homes. When homes are bought, the economy benefits. It’s a strategic push to keep the housing market alive and healthy without risking a repeat of past mistakes.

As Brett Hively, SVP of Mortgage, Finance, and Strategy at Ameris Bancorp, explains:

“This uptick is opening the door for many borrowers to move forward with a home purchase or a refinance program.”

This is more than just good news—it’s a shift that could change your life.

Here’s What You Can Do Right Now

Feeling a bit more hopeful? You should be. But don’t just sit there. Here’s what you need to do to take advantage of this mortgage-friendly environment:

-

Check Your Credit Score: You don’t need a perfect 800. Many lenders approve buyers with scores in the 600s—sometimes lower with a strong overall financial profile.

-

Evaluate Your Budget: Know how much you can afford for a monthly mortgage payment. Use an online calculator to get a rough idea.

-

Talk to a Lender or Mortgage Broker: Seriously—this is key. They’ll assess your financial situation and let you know exactly what loan products you might qualify for.

-

Get Pre-Approved: If you’re serious about buying, this gives you a clear idea of your buying power—and makes you look stronger to sellers.

Final Thoughts: This Could Be Your Window of Opportunity

Look, no one’s saying it’s easy to buy a home right now. Prices are still high in many places, and competition can be fierce. But from a lending standpoint? Things are shifting in your favor.

This isn’t a flash-in-the-pan moment either—it’s part of a larger trend that reflects a healthy balance between access and accountability. You’re not being set up for failure. You’re being given a chance.

So, if you’ve been hesitating, thinking, “I’ll never qualify for a mortgage,” it might be time to rethink that mindset.

Your dream of owning a home may be closer than you think.

Ready to explore your options? It all starts with a conversation. Find a lender, crunch the numbers, and take that first step toward turning the key to your future front door.

Recent Posts

GET MORE INFORMATION