Renting Vs. Buying a Home in 2025: What’s the Smarter Financial Move?

Let’s be honest—you’ve probably asked yourself this more than once lately:

“Should I rent or finally buy a home?”

With soaring home prices, rising mortgage rates, and a cost of living that seems to never take a break, it’s no wonder you’re on the fence. Renting feels safer, easier—heck, maybe it’s even your only option right now.

But here’s the kicker: what feels right in the short term could quietly cost you big time in the long run.

Let’s break it down—no jargon, no fluff. Just real talk about renting vs. buying, and what it means for your wallet and your future.

Renting Feels Easy—But Is It Really the Smarter Choice?

Look, renting does have its perks.

You don’t need to worry about property taxes, repairs, or locking in a 30-year mortgage. Monthly payments can even be lower depending on where you live. Plus, flexibility? Renters have that in spades. You can pick up and move with relatively little hassle.

But here’s the thing that often gets overlooked…

When you rent, you’re literally helping someone else build wealth—your landlord.

That monthly rent check? It’s paying their mortgage, not yours. And while it may feel like you’re saving money now, you’re not building anything for your future.

Buying a Home: Not Just Shelter, But a Wealth-Building Tool

Let’s shift the perspective for a second.

Owning a home isn’t just about having a roof over your head—it’s about investing in your financial future.

When you buy a home, you start building something called equity. That’s the value of your home minus what you owe on it. And with each monthly mortgage payment, your equity grows. It’s like a forced savings account—except you can live in it.

And get this:

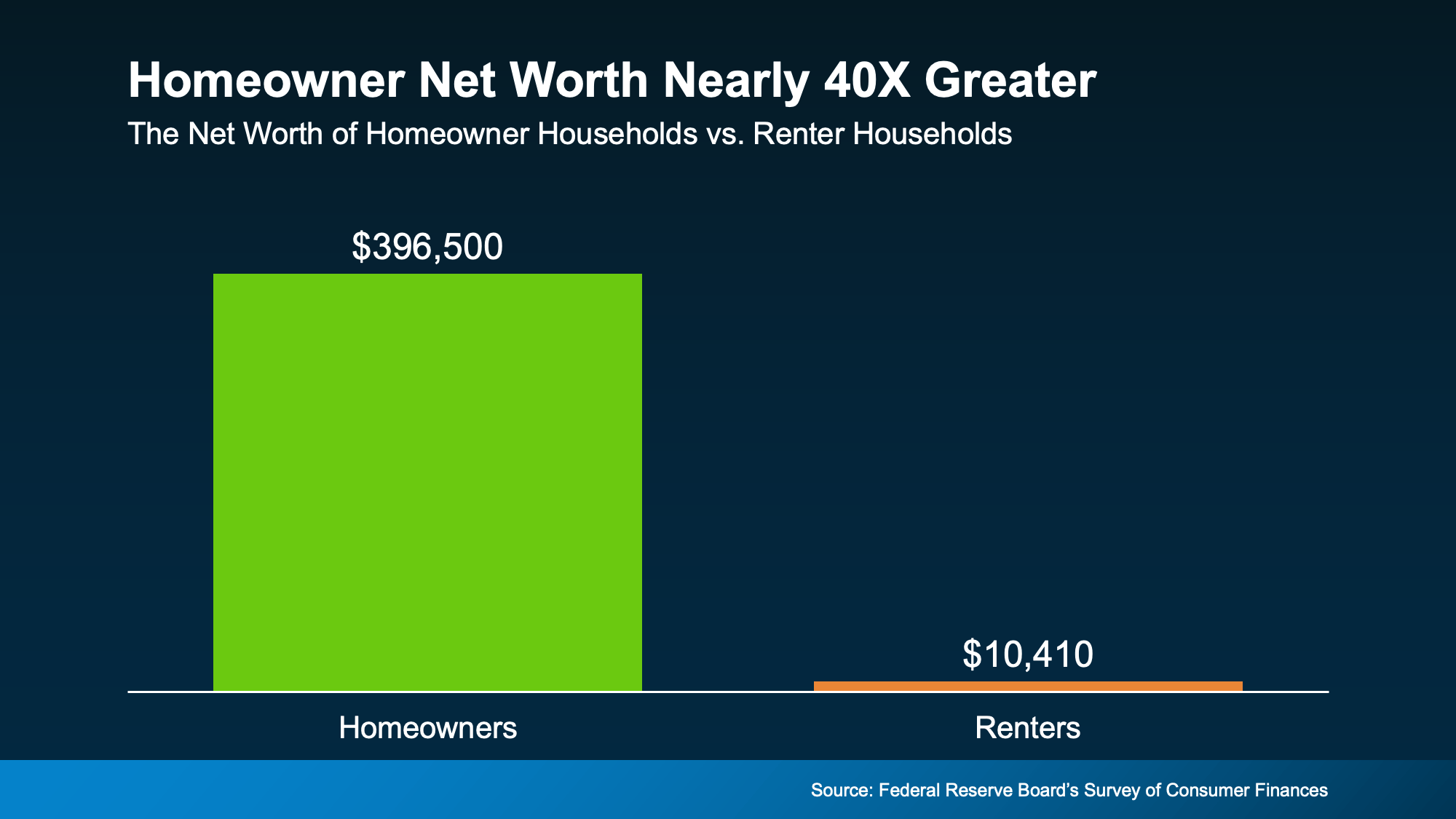

💡 The average homeowner’s net worth is almost 40 times greater than a renter’s.

That’s not a typo. 40 times.

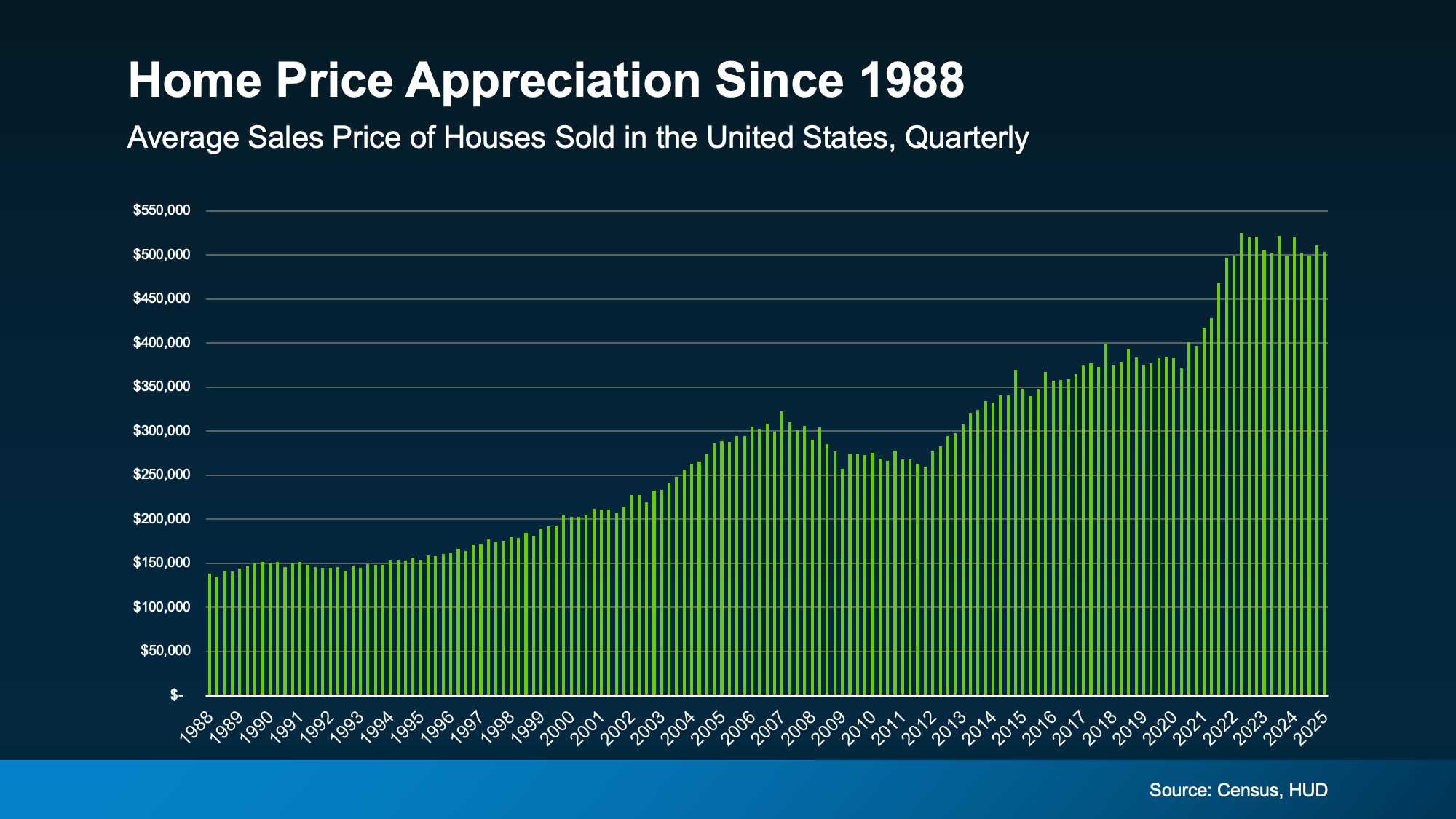

How? It’s simple math. Home values tend to rise over time. When you own, you benefit from that appreciation. When you rent, you don’t.

Renting Means No Return On Investment (ROI)

Let’s use an analogy here.

Imagine you’re pouring your hard-earned money into a bucket every month. If you own your home, that bucket has a bottom—it holds your money and turns it into wealth over time.

If you rent? That bucket’s got a hole in it. Every dollar you pour in just leaks right out.

Sure, renting may feel “cheaper” today. But fast forward a few years, and you’ll realize you’ve spent tens of thousands of dollars without gaining a single dollar in return.

The Rise of Rent: Why Renting Isn't the Long-Term Budget Hack You Think It Is

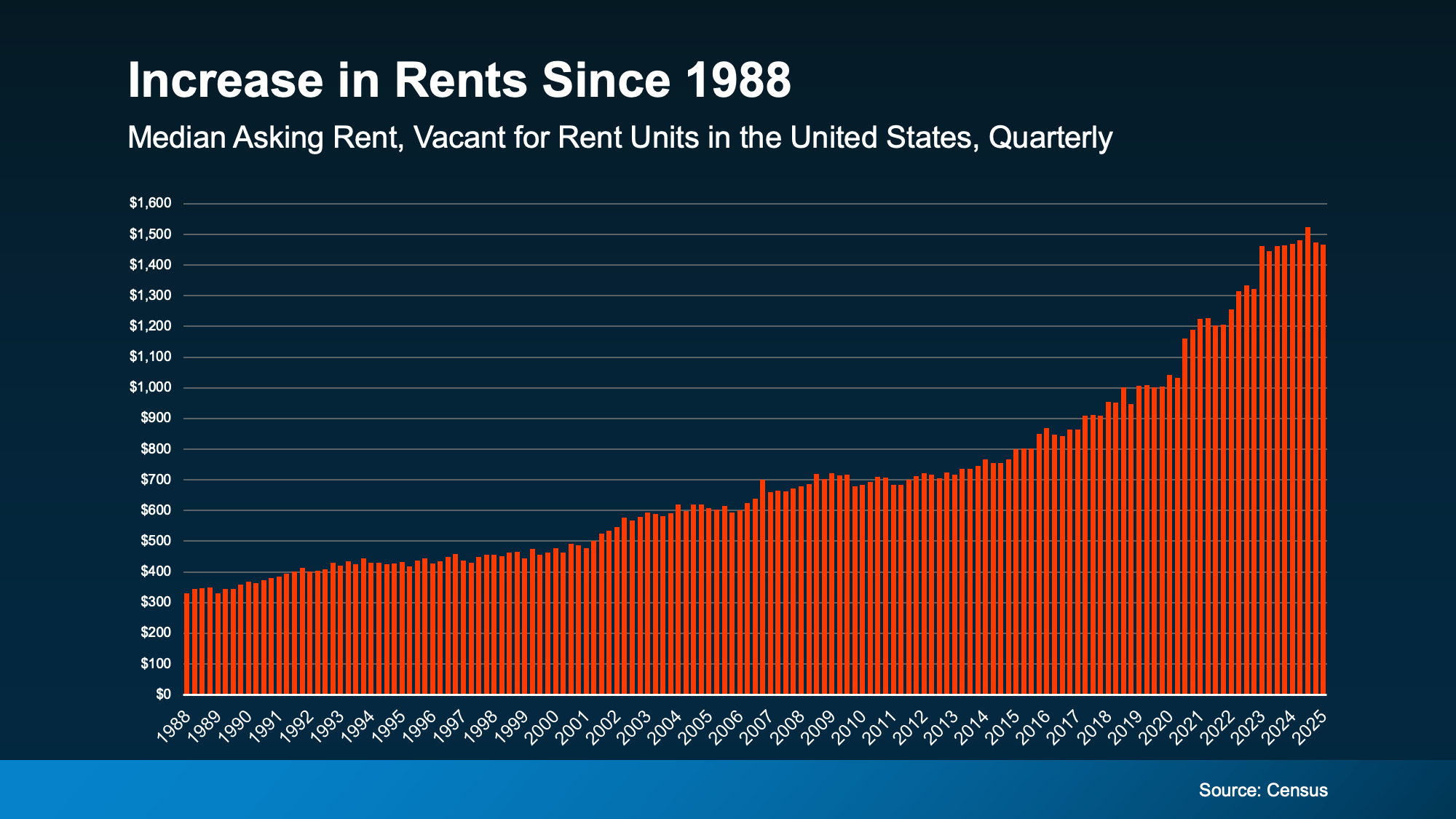

Let’s not sugarcoat it—rent keeps going up.

Sure, it might seem stable right now in some areas, but history doesn’t lie. Rent has climbed steadily over the years, and it’s not slowing down anytime soon.

Here’s what that means for you:

The longer you rent, the harder it gets to save for a home.

That rising rent eats into your budget, leaving less room to build up a down payment or boost your credit. It’s a cycle—and it’s tough to break.

In fact, a recent Bank of America survey revealed that 72% of renters are worried that rising rents are impacting their finances now—and in the future.

The Equity Factor: What Makes Owning a Home So Powerful?

Still on the fence? Let’s talk about equity, the quiet wealth builder that turns ordinary homeowners into financially secure individuals.

Here’s what makes equity so awesome:

-

It grows over time – As you pay down your mortgage and as your home's value increases, your equity snowballs.

-

It’s accessible – Home equity can be used for big goals: renovations, education, or even as collateral for loans.

-

It boosts your net worth – Unlike rent payments that vanish into thin air, mortgage payments work for you.

It’s no wonder Forbes still calls homeownership a “cornerstone of the American Dream.”

Renting vs. Buying in 2025: What’s the Real Cost?

Let’s break it down one more time:

| Factor | Renting | Buying |

|---|---|---|

| Monthly Payment | May be lower initially | Higher upfront, more stable long-term |

| Equity Building | ❌ None | ✅ Yes |

| Stability | ❌ Subject to rent increases | ✅ Fixed mortgage (in most cases) |

| ROI | ❌ No return | ✅ Property appreciation |

| Flexibility | ✅ Easy to move | ❌ Harder to relocate quickly |

| Maintenance Responsibility | ✅ Landlord’s problem | ❌ Yours (but adds value too) |

So yes, buying comes with more responsibility and a steeper initial price tag. But it also comes with rewards renting simply can’t match.

Can’t Buy Now? Here’s What You Can Do

Let’s keep it real—not everyone is ready to buy a home today, and that’s okay.

But if homeownership is a long-term goal, the best time to start planning was yesterday. The second-best time? Right now.

Here’s what you can do to get on the path:

-

Check your credit score – It’s the first step to mortgage approval.

-

Create a savings plan – Start stashing away for a down payment, even if it’s just a little at a time.

-

Talk to a professional – A real estate agent or financial advisor can help map out a plan that fits your life.

Remember: renting doesn’t have to be forever—it can be a stepping stone.

Final Thoughts: Choose the Path That Builds Your Future

So, what’s the bottom line?

Renting may be easier today—but buying builds a better tomorrow.

It’s not just about dollars and cents. It’s about building something that’s yours. Creating stability. Growing your wealth. Leaving a legacy.

If you’re feeling stuck in the rental loop, don’t lose hope. Owning a home might feel out of reach now, but with the right strategy and a little patience, it’s entirely possible.

So ask yourself: do you want to keep paying your landlord’s mortgage—or start investing in your own future?

Need help figuring out your next step? Let's talk about your goals, your budget, and what it’ll take to make homeownership a reality. Your dream home is out there—and with the right plan, it can be yours.

Recent Posts

GET MORE INFORMATION