Unlocking the Mystery of Mortgage Rates

Ever wondered why mortgage rates seem to be playing a game of seesaw lately? Strap in, because we're about to decode the economic puzzle behind it all. From inflation hikes to Federal Reserve whispers, let's delve into the whirlwind world of mortgage rates.

Deciphering the Economic Puzzle

Mortgage rates aren't solitary creatures; they dance to the rhythm of various economic factors. Picture this: the job market's heartbeat, the pulse of inflation, the sway of consumer spending, and the ever-looming shadow of geopolitical uncertainty. Add to that mix the Federal Reserve, the conductor orchestrating the symphony of monetary policy. Intrigued? Here's the lowdown.

Federal Reserve’s Influence

Enter the Federal Reserve, or as insiders call it, the Fed. When the Fed decides to tweak the Federal Funds Rate—essentially the cost of banks borrowing money from each other—it sends ripples through the financial landscape. Though this rate doesn't directly dictate mortgage rates, it sets the stage for their performance. Cue the recent spike in mortgage rates as the Fed raised the curtain on its tightening monetary policy.

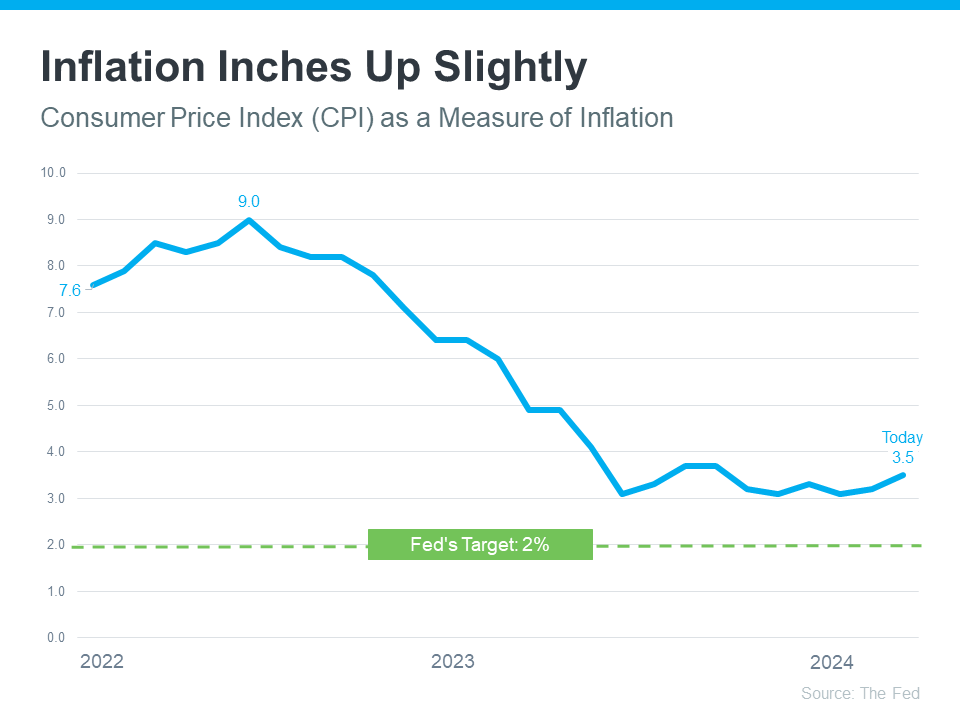

Inflation: The Central Player

Ah, inflation—the elusive specter haunting economic forecasts. While we've made strides in taming its voracious appetite since the early 2022 surge, we're still a hair's breadth away from the Fed's coveted 2% target. Take a glance at the graph; it's a rollercoaster ride of ups and downs. Sam Khater, Freddie Mac's Chief Economist, sums it up succinctly:

“Strong incoming economic and inflation data has caused the market to re-evaluate the path of monetary policy, leading to higher mortgage rates.”

In simpler terms, inflation's stubborn grip on the economy is like a stubborn stain on your favorite shirt—tough to remove and even tougher to predict.

Anticipating the Descent of Mortgage Rates

So, when can we expect mortgage rates to take a nosedive? Experts predict a gradual descent, but patience is key. Mike Fratantoni, Chief Economist at the Mortgage Bankers Association, offers insights into the waiting game:

“The FOMC did not change the federal funds target at its May meeting, as incoming data regarding the strength of the economy and stubbornly high inflation have resulted in a shift in the timing of a first rate cut. We expect mortgage rates to drop later this year, but not as far or as fast as we previously had predicted.”

Translation? Brace yourself for lower mortgage rates, but don't hold your breath just yet. Economic forecasts resemble weather predictions—always subject to change.

Navigating the Market: A Buyer’s Guide

In a market swirling with uncertainty, timing becomes a perilous gamble. Should you jump into homeownership now or wait for the winds of change to favor your sails? Bankrate offers sage advice:

“ . . . trying to time the market is generally a bad idea. If buying a house is the right move for you now, don’t stress about trends or economic outlooks.”

In essence, focus on the present—whether it's the right time for you to embark on the journey of homeownership.

Conclusion

The enigma of mortgage rates unfolds against a backdrop of economic intricacies and Federal Reserve maneuvers. While the road ahead may seem fraught with uncertainty, one thing remains certain: understanding the economic symphony orchestrating mortgage rates can help you navigate the waves of homeownership with confidence. So, buckle up and brace yourself for the ride—it's bound to be an exhilarating one!

Recent Posts

GET MORE INFORMATION