What to Expect from This Week’s Fed Meeting: Key Insights for the Housing Market

This week, the Fed is meeting again to discuss the future of the Federal Funds Rate – an important tool they use to manage economic stability. Here’s a breakdown of the key elements driving the Fed’s decision-making process and what you should be watching if you're navigating the housing market.

Understanding the Federal Funds Rate and Its Influence on Mortgage Rates

Before diving into the specifics, let’s quickly revisit what the Federal Funds Rate is. This rate determines how much banks charge each other for overnight loans, and while it doesn’t directly set mortgage rates, it has a significant indirect influence. When the Fed adjusts the Federal Funds Rate, it impacts the cost of borrowing across the economy, including home loans.

For homebuyers and sellers, the question on everyone's mind is: will mortgage rates go down soon? Let’s take a closer look at the current economic indicators that the Fed is focused on, and how they might affect mortgage rates moving forward.

What’s Driving the Fed’s Decisions: Key Economic Indicators

The Fed’s primary mission is to maintain a stable economy, and they do this by monitoring three key indicators: inflation, job growth, and unemployment. Each of these factors plays a critical role in how the Fed will adjust interest rates in the future.

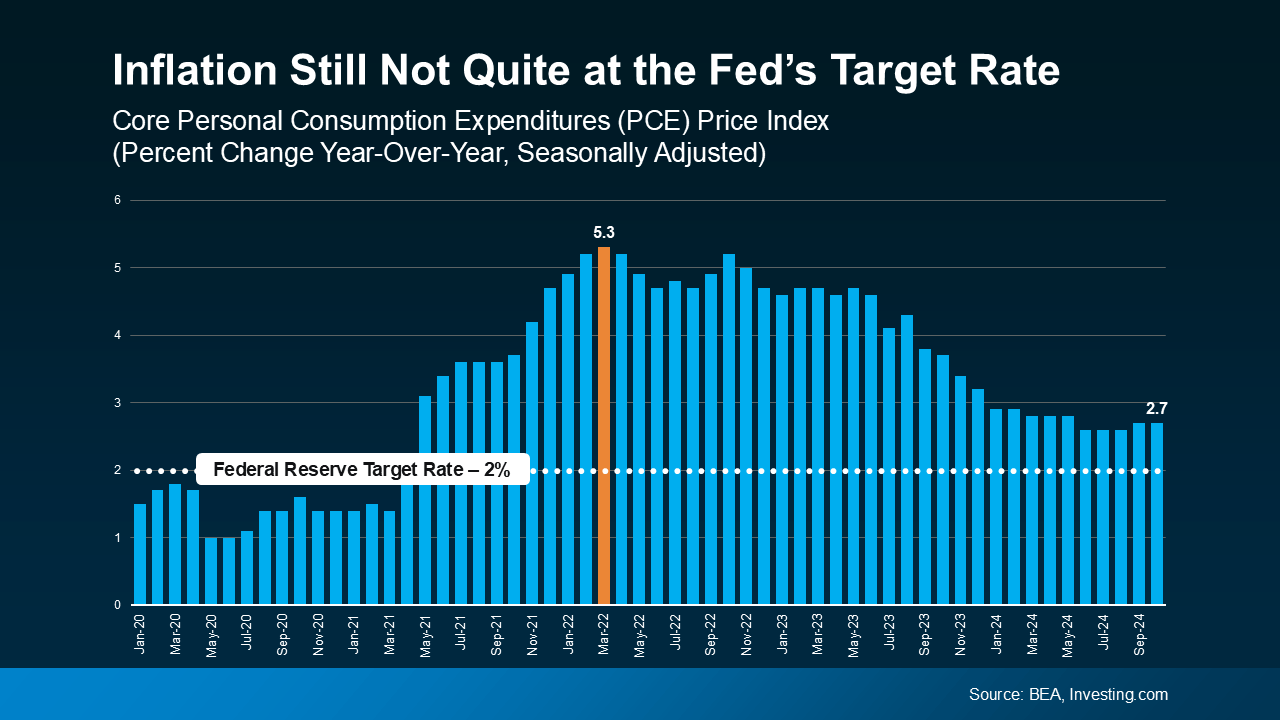

1. The Direction of Inflation: Is It Finally Cooling?

Inflation has been a hot topic for a while now. You’ve probably noticed higher prices at the grocery store and gas station – that’s inflation at work. The Fed targets a 2% inflation rate, and right now, inflation is still above that level, but it's been gradually coming down over the past two years.

The recent trend shows inflation moving in the right direction, although not exactly where the Fed would like it just yet. A little bit of volatility is still in play, but the overall trajectory seems positive. This is why the Fed is likely to cut the Federal Funds Rate by a small amount this week. By lowering borrowing costs, they hope to help keep inflation on a steady decline without stalling economic growth.

2. How Many Jobs Are Being Added to the Economy?

Job growth is another important factor in the Fed’s decision-making. The Fed doesn’t want the economy to overheat, which is why they look at the number of jobs being added each month. When job growth slows down, it signals that the economy is cooling off slightly, which can help curb inflationary pressures.

According to a recent Reuters report, "Any doubts the Federal Reserve will go ahead with an interest-rate cut…fell away on Friday after a government report showed U.S. employers added fewer workers in October than in any month since December 2020." Fewer jobs being created means the economy is beginning to cool, which is exactly what the Fed wants to see as they look to adjust rates.

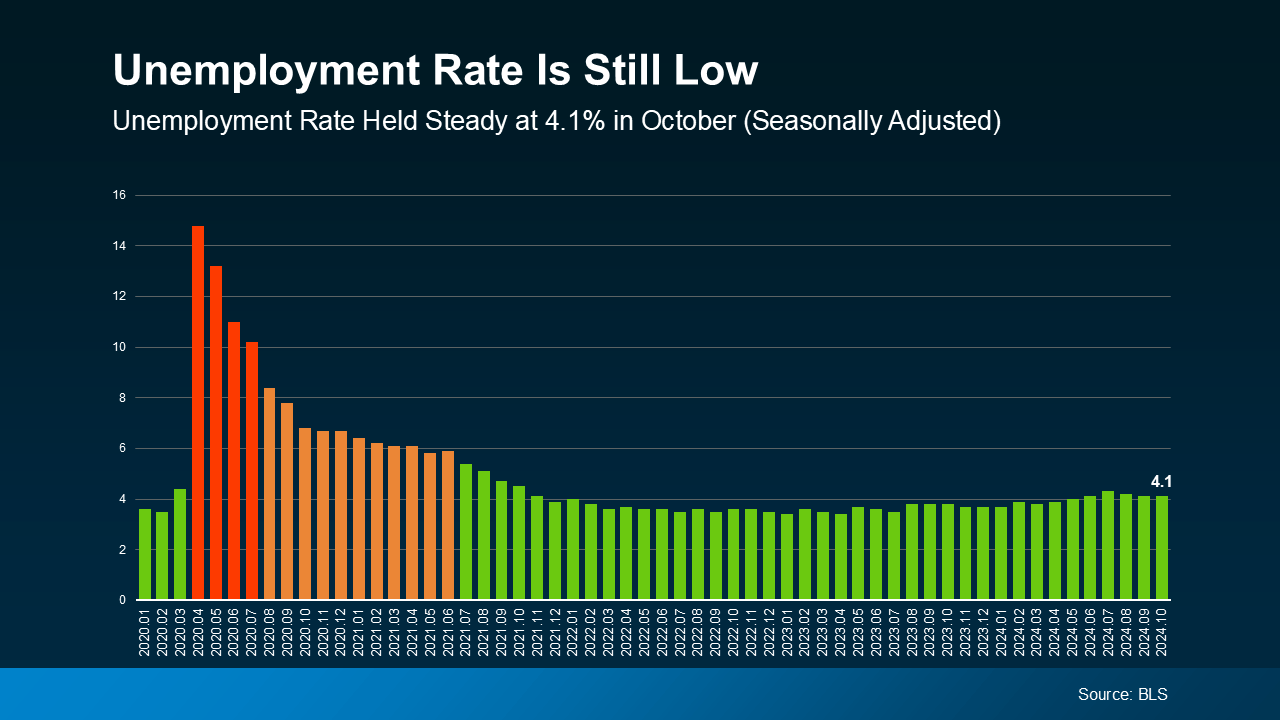

3. Unemployment Rate: Are People Still Employed?

The unemployment rate is a lagging indicator of economic health. A low unemployment rate means most people who want a job can find one, which is great for individuals and families. However, a low unemployment rate can also lead to higher wages and more spending, which puts upward pressure on inflation. That’s why the Fed keeps a close eye on unemployment numbers.

The current unemployment rate sits at 4.1%, which is considered quite low. Most economists view an unemployment rate below 5% as a sign of a strong labor market. While this is great news for workers, it can also make it harder for the Fed to keep inflation under control. In this context, the Fed will be looking for signs that the labor market is starting to cool down a bit, which might give them more room to cut rates without sparking inflation.

What Does This Mean for Mortgage Rates?

With all these factors in mind, what can we expect from mortgage rates in the near future? If the Fed cuts the Federal Funds Rate, it could help push mortgage rates lower, but don’t expect an immediate or dramatic drop. Mortgage rates are influenced by a wide range of factors, and while the Fed’s actions are important, they don’t dictate the rates you’ll see at your local bank.

Experts predict that if the Fed cuts the Federal Funds Rate by a quarter of a percentage point, mortgage rates might start to ease, but this will be a gradual process. As Ralph McLaughlin, Senior Economist at Realtor.com, points out, “The trajectory of rates over the coming months will be largely dependent on three key factors: (1) the performance of the labor market, (2) the outcome of the presidential election, and (3) any possible reemergence of inflationary pressure.”

It’s important to remember that the Fed’s actions are only one piece of the puzzle. Mortgage rates will continue to fluctuate based on these other factors, and there could still be some volatility ahead. However, as the economy continues to stabilize and the Fed adjusts its policies, we could see mortgage rates trending lower over the course of 2024 and 2025.

The Bigger Picture: What to Expect in the Coming Months

While the Fed is taking steps to address inflation, slow down the economy, and stabilize the labor market, there’s still plenty of uncertainty in the air. Economic conditions are always in flux, and even small changes in key indicators can lead to shifts in market sentiment. Here’s what you can expect as we move through the rest of 2024:

- Mortgage Rate Volatility: Even if the Fed cuts the Federal Funds Rate, mortgage rates won’t necessarily fall immediately or consistently. There will likely be ups and downs, especially as inflation, the labor market, and political events come into play.

- Stabilization Toward the End of the Year: Experts predict that by late November or early December, mortgage rates may start to stabilize. As volatility settles down, more clarity should emerge about where rates are headed in 2025.

- Gradual Rate Declines in 2025: If the Fed continues to cut rates and the economy stays on track, we could see mortgage rates gradually decline in the coming year. However, this will depend on several factors, including how inflation and job growth continue to evolve.

Bottom Line: Stay Informed and Be Prepared

While the Fed’s actions have a significant impact on mortgage rates, it’s important to understand that they’re just one part of a larger picture. Economic data, job reports, and inflation trends all play a role in determining how mortgage rates move.

If you’re thinking about buying or selling a home, now is a great time to stay informed. Keep an eye on economic indicators, work with a trusted mortgage lender to stay on top of rate changes, and be prepared for some volatility in the coming months. As long as you’re staying informed and working with professionals, you’ll be able to make the best decisions for your financial future – no matter what the Fed decides this week.

So, while the future is a bit uncertain, with a solid strategy and the right information, you can turn this volatility into an opportunity. Keep your eyes on the Fed, and stay ready to act when the time is right for you.

Recent Posts

GET MORE INFORMATION