How an Economic Slowdown Could Actually Affect the Housing Market (Spoiler: It’s Not What You Think)

When you hear “recession,” what’s the first thing that comes to mind? Job losses, stock market dips, shrinking wallets—and yes, a potential hit to the housing market. The media loves to stir the pot with scary headlines, but here’s the truth: a recession doesn't automatically mean the value of your home is going down.

In fact, history tells a different story. So before you panic-sell or put your house hunt on pause, let’s dig into what really happens to the housing market when the economy hits the brakes.

Recession ≠ Housing Market Crash (Let That Sink In)

It’s easy to think back to 2008 and assume another recession would bring a tidal wave of plummeting home prices. But guess what? That crash was an outlier, not the norm.

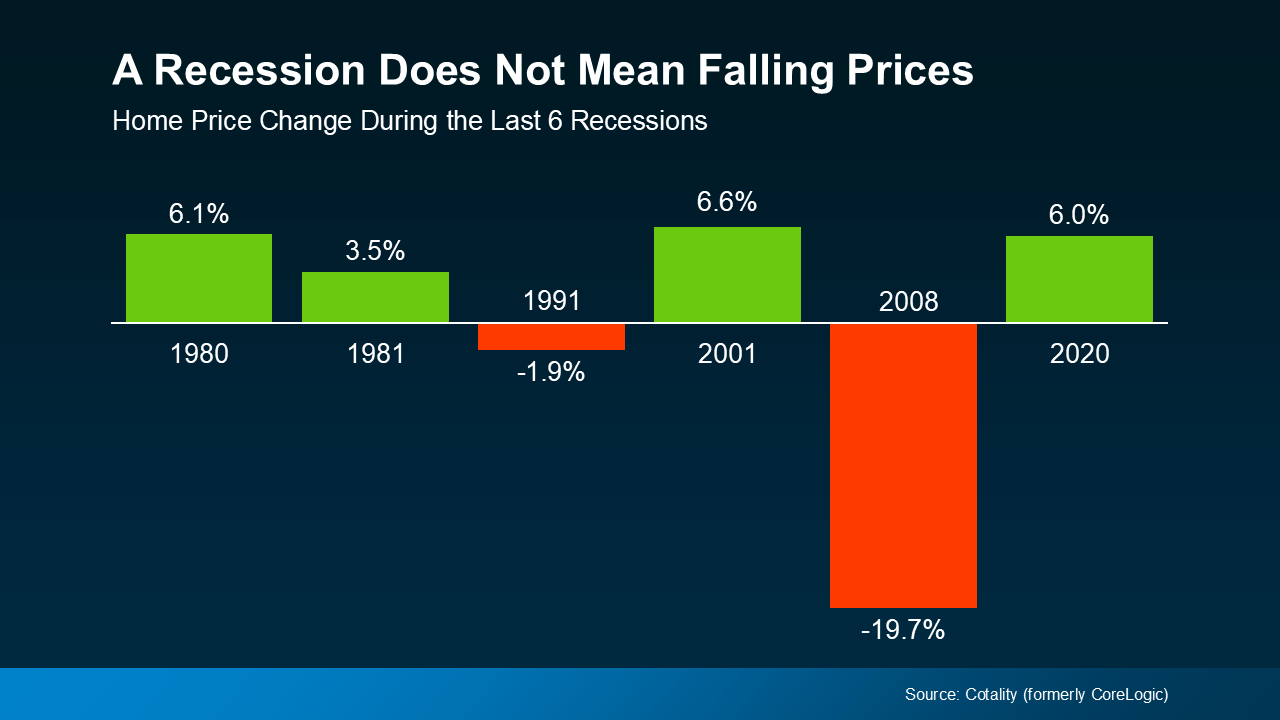

Let’s rewind to the last six U.S. recessions—starting all the way back in the early 1980s. What did home prices do? In four out of six of those downturns, they actually increased. Surprised? You're not alone.

Here’s the reality: the 2008 housing meltdown was driven by an oversupply of homes, risky lending practices, and a full-blown mortgage crisis. It wasn’t just a bad economy—it was a housing market gone wild. Fast forward to today, and we’re in a completely different environment.

Inventory is still tight. Even in cities where listings have climbed a bit, we’re nowhere near the massive oversupply that led to the 2008 crash. So no, we’re not headed for a repeat performance.

Key takeaway: An economic slowdown doesn’t equal a housing collapse. Don’t let one bad memory overshadow decades of more stable trends.

Home Prices Don’t Always Fall—Here’s What They Do Instead

So, what actually happens to home prices during a recession?

Generally speaking, they follow the same trend they were on before the slowdown hit. If prices were climbing (as they are now), they’ll likely keep climbing—but at a more moderate pace. If the market was already cooling, a recession might slow things further.

Think of it like a car coasting on cruise control. A recession might ease up on the gas pedal, but it doesn’t necessarily slam on the brakes.

Why? Because housing isn’t just driven by the economy—it’s also shaped by demand, supply, local markets, and interest rates.

Mortgage Rates Tend to Drop (A Silver Lining?)

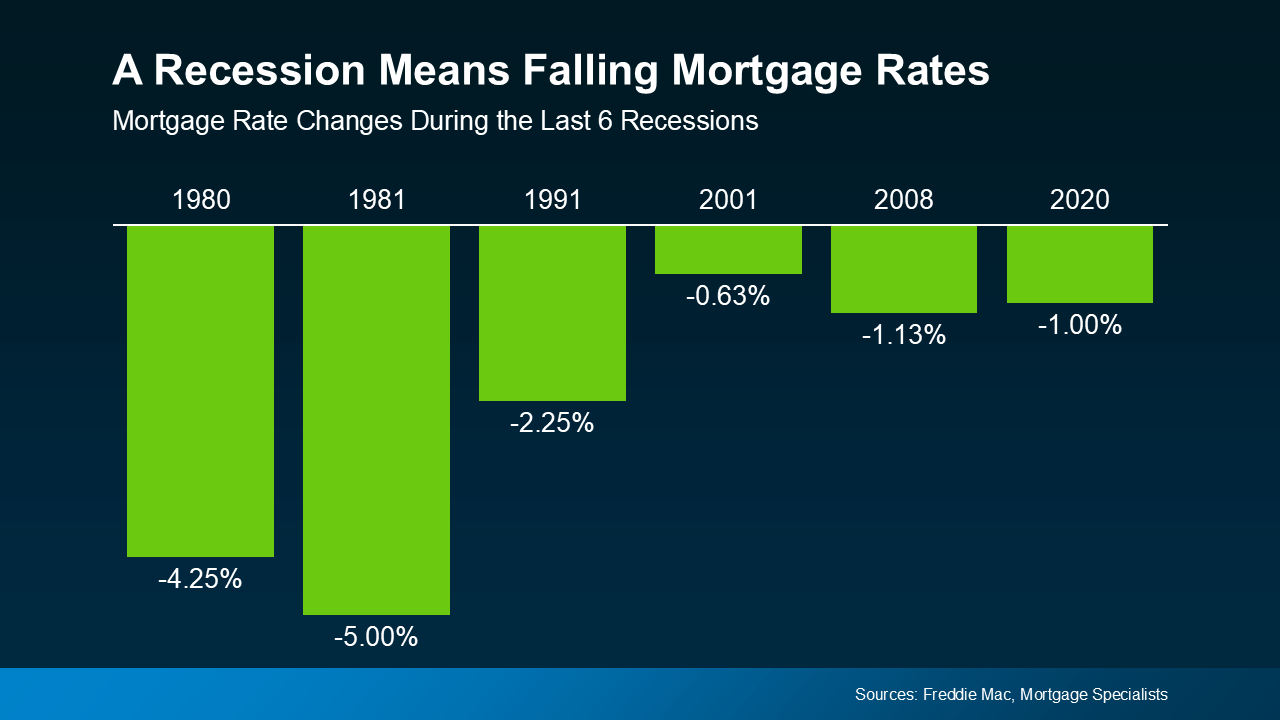

Here’s some good news: while home prices tend to stay steady (or climb modestly), mortgage rates usually go down during recessions.

Yep, history has receipts. In every one of the last six recessions, mortgage rates dropped. And when rates drop, your buying power goes up.

Let’s break that down: if rates fall even just 1%, that can translate into hundreds of dollars saved per month on your mortgage. Over the life of a loan? We’re talking tens of thousands of dollars in savings.

Now, don’t expect to see the ultra-low 3% rates we had in 2020—that was a unicorn moment. But even a modest dip could make a big difference in affordability.

Bottom line: If a recession cools the economy, it might heat up opportunities for buyers.

Should You Buy or Sell During a Slowdown?

This is the million-dollar question. And here’s the not-so-secret answer: it depends on your personal situation.

If you’re a buyer, a recession could mean:

-

Lower mortgage rates

-

Less competition

-

More room to negotiate with sellers

If you’re a seller, remember:

-

Inventory is still tight, so demand is holding up

-

Home values are generally stable

-

Serious buyers are still out there

The truth is, the best time to buy or sell isn’t about the economy—it’s about your goals, your finances, and your timeline. Don’t let fear-based headlines dictate your moves.

The Bigger Picture: What to Watch for

While we’re busting myths, it’s worth keeping an eye on a few key indicators:

-

Inventory levels: More homes on the market could cool price growth, but we’re far from oversupply territory.

-

Interest rate trends: The Federal Reserve may adjust rates in response to economic signals, and that directly affects mortgage rates.

-

Consumer confidence: If people feel secure in their jobs and finances, the housing market stays active—even during a slowdown.

Keep in mind that real estate is hyper-local. One city might be booming while another feels the chill. Talk to a local real estate expert to get the lay of the land in your area.

What You Can Do Now

Whether you’re buying, selling, or just sitting tight, here’s how to stay ahead of the curve:

- Get pre-approved if you’re planning to buy. A rate lock could save you money.

- Track home values in your neighborhood. Knowledge is power.

- Talk to a financial advisor before making big moves. Recessions can be tricky to navigate.

- Stay calm and skip the hype. Real estate is a long game, and short-term headlines shouldn’t derail your strategy.

Final Thoughts: Don’t Fear the “R” Word

Sure, the thought of a recession can make your stomach drop. But when it comes to housing? The data doesn’t lie.

Most of the time, recessions don’t send home values into freefall. They don’t stop people from buying homes. And they definitely don’t spell doom for homeowners.

If anything, a slowdown might just give buyers a breather and sellers a chance to capitalize before the next upswing. So, breathe easy. Stay informed. And remember—housing is built to weather the storm.

Want the inside scoop on your local market? Reach out to a trusted real estate agent or mortgage advisor. Knowledge is the best defense against fear-driven decisions.

Recent Posts