The 20% Down Payment Myth: What You Really Need to Know Before Buying Your Home

For many first-time homebuyers, the thought of saving up for a down payment can seem overwhelming. You’ve probably heard the common rule of thumb that you need to put down 20% of the home’s purchase price. But here’s the thing: that’s not necessarily true. In fact, the 20% down payment myth is one of the biggest misconceptions that stops people from diving into homeownership. Let’s debunk this myth and look at the truth behind what it really takes to buy a home in today’s market.

Do You Really Need to Put 20% Down?

The short answer is no – you don’t have to put 20% down when buying a home, unless your specific loan or lender requires it. In fact, there are several types of loans available that allow first-time homebuyers to purchase a property with much smaller down payments.

If you're struggling to save up a large amount, rest assured there are options. For example, FHA loans only require a down payment as low as 3.5%, while VA loans and USDA loans often come with zero down payment requirements for qualified buyers. So, while it may be ideal to save up more to lower your monthly mortgage payments, putting down 20% is far from mandatory.

According to The Mortgage Reports, “many homebuyers are able to secure a home with as little as 3% or even no down payment at all… the 20 percent down rule is really a myth.”

What’s the Real Median Down Payment?

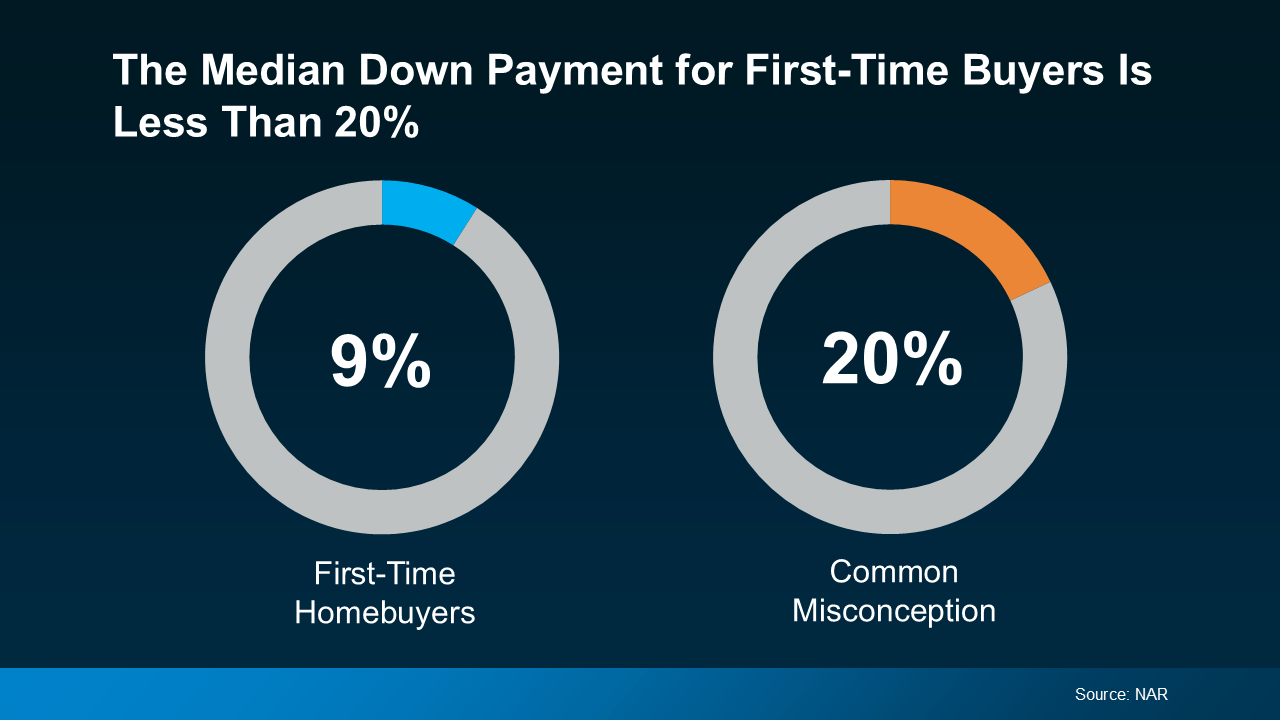

If you’re wondering where the truth lies, look no further than the National Association of Realtors (NAR). They’ve found that the median down payment for first-time homebuyers is just 9%. That’s right – most people don’t put down anywhere near 20%.

The takeaway here is clear: you might not need to save up as much as you originally thought. In fact, you could be closer to owning your dream home than you realize.

The Power of Down Payment Assistance Programs

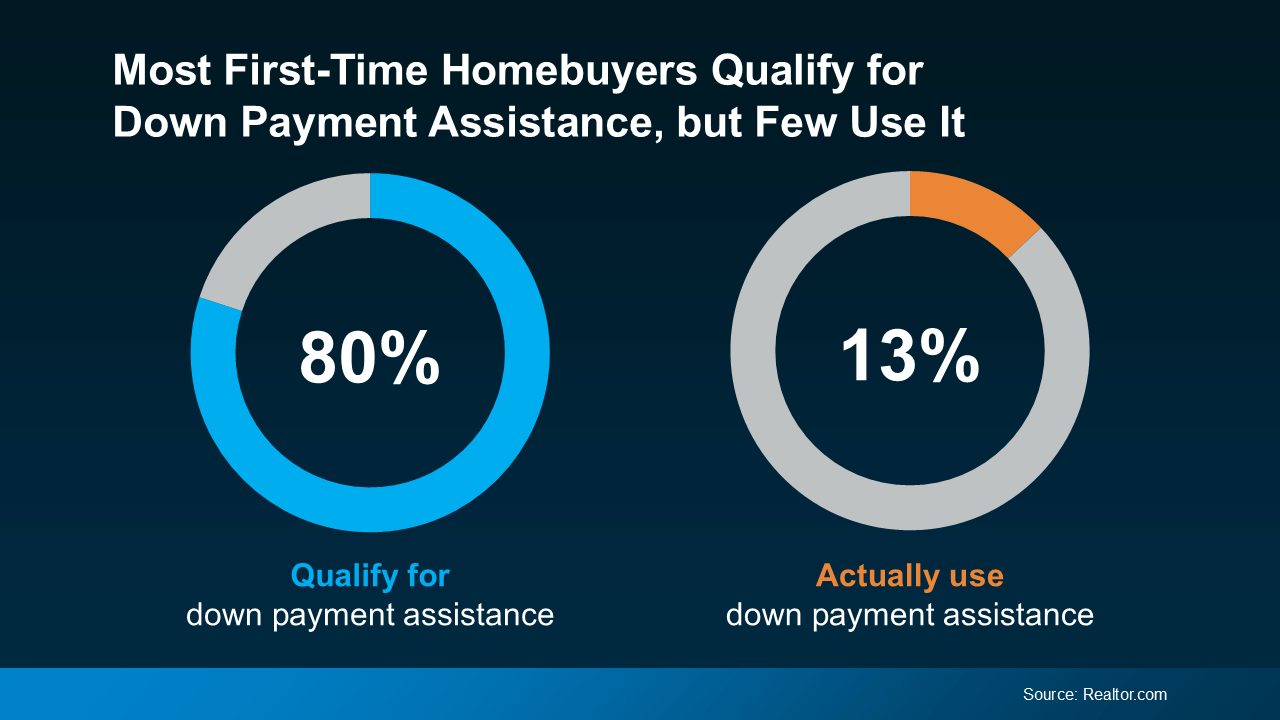

Here’s something most first-time homebuyers aren’t aware of: down payment assistance programs (DPA). Believe it or not, nearly 80% of first-time buyers qualify for DPA, but only 13% actually take advantage of it. This is a major missed opportunity!

These programs can provide significant financial help, sometimes offering thousands of dollars to go toward your down payment. As Rob Chrane, founder and CEO of Down Payment Resource, says, “Our data shows the average DPA benefit is roughly $17,000. That can be a nice jump-start for saving for a down payment and other costs of homeownership.”

Imagine qualifying for $17,000 in assistance! That could make a world of difference when it comes to reaching your down payment goal. And in some cases, you may even be able to combine multiple programs, which can provide an even bigger boost to your savings.

Types of Loans and Programs to Consider

Not all loans are created equal. Some loans are designed specifically for first-time homebuyers or individuals with certain financial needs. Here’s a breakdown of some of the most common options that may help you achieve your homeownership dream:

-

FHA Loans: If you’re a first-time buyer with less-than-perfect credit, an FHA loan might be your best bet. This type of loan allows for a down payment as low as 3.5%. It’s an excellent option for buyers with limited savings.

-

VA Loans: Veterans, active-duty service members, and certain surviving spouses are eligible for VA loans. These loans don’t require a down payment at all, which makes them one of the most appealing options for those who qualify.

-

USDA Loans: If you’re looking to buy in a rural or suburban area, a USDA loan could help you purchase a home with no down payment. These loans are designed to assist low- to moderate-income buyers.

-

Conventional Loans: Conventional loans typically require a 5% to 20% down payment. However, if you can manage a 5% down payment, you may qualify for private mortgage insurance (PMI), which helps lower your risk in the eyes of lenders.

The Hidden Advantage of Smaller Down Payments

While the idea of putting down a large sum of money might seem appealing, there are also some major advantages to opting for a smaller down payment. Here’s why:

-

More Cash Flow for Other Expenses: By saving less for the down payment, you can have more funds available for other important costs like closing fees, moving expenses, or home improvements.

-

Building Equity Faster: The more money you put down, the less you’ll owe on your mortgage. However, a smaller down payment can actually work in your favor by allowing you to invest that money elsewhere—perhaps in stocks or a retirement fund—where it could generate higher returns over time.

-

Faster Homeownership: For many, saving up a large down payment can delay their homebuying goals. If you don’t need to wait for the full 20%, you could be in your new home much sooner.

Common Myths About the 20% Down Payment

Let’s clear up some common misconceptions about the 20% down payment rule. Here are some of the most persistent myths:

-

Myth: You Can’t Buy Without 20% Down

Fact: As we’ve already covered, there are multiple loan programs that allow for much lower down payments. You can often buy a home with as little as 3% down. -

Myth: A Large Down Payment Guarantees Better Loan Terms

Fact: While a larger down payment may give you more favorable loan terms, it doesn’t necessarily guarantee them. Lenders look at other factors like your credit score and debt-to-income ratio when making loan decisions. -

Myth: You’ll Pay Higher Mortgage Insurance if You Don’t Put Down 20%

Fact: Private mortgage insurance (PMI) is required for down payments under 20%, but it’s not as scary as it sounds. It’s typically a small monthly cost, and once you’ve paid off enough of your mortgage, you can have PMI removed.

Bottom Line: It’s Time to Rethink Your Homebuying Strategy

Buying a home is one of the biggest financial decisions you’ll ever make, but it doesn’t have to be as daunting as you might think. The 20% down payment myth has held too many people back, but now that you know the truth, it’s time to rethink your homebuying strategy.

There are plenty of options out there—whether it’s a loan with a low down payment requirement or a down payment assistance program that can help boost your savings. And by understanding the real requirements and options available, you can feel more confident about stepping into the world of homeownership.

So, don’t let the 20% down payment myth hold you back from buying your first home. The home you’ve been dreaming about might be closer than you think!

Recent Posts