Unlocking Homeownership: How FHA Loans Make Buying Your First Home Easier Than You Think

Buying your first home is a big deal. It’s exciting. It’s nerve-wracking. And let’s be real—it can feel downright impossible with today’s housing prices. But guess what? You’re not alone, and you’re definitely not out of luck. There’s a little-known hero in the world of real estate that’s been helping first-time buyers for decades: the FHA loan.

Let’s break down what FHA loans are, why they’re perfect for first-time buyers, and how they can help you kickstart your journey toward owning a place you can finally call home.

What Is an FHA Loan, Really?

Let’s start with the basics. FHA stands for Federal Housing Administration. An FHA loan is a government-backed mortgage that’s specifically designed to make homeownership more accessible—especially for first-time buyers or people with less-than-perfect credit.

Think of it like a supportive friend in the homebuying process—one that’s willing to vouch for you when traditional lenders might hesitate. Because these loans are insured by the government, lenders are more willing to work with buyers who might not meet the strict standards required for conventional loans.

Why Are FHA Loans a Game Changer for First-Time Buyers?

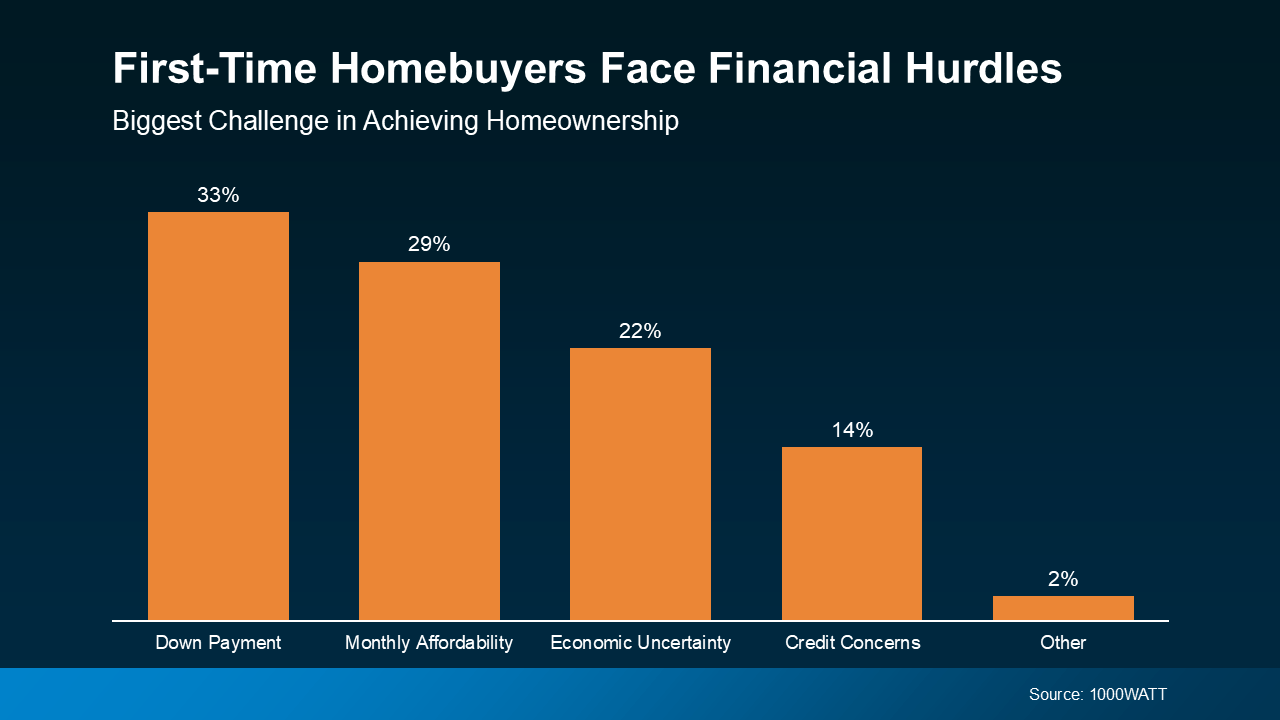

Let’s face it—saving for a down payment and affording a monthly mortgage payment can feel like climbing Mount Everest in flip-flops. And for many new buyers, that’s exactly what’s stopping them from taking the leap.

But here’s the good news: FHA loans were built to solve those exact problems.

1. Lower Down Payment Requirements

When you go the conventional route, lenders typically ask for 10% to 20% of the home price as a down payment. That can add up to a mountain of cash.

But with an FHA loan? You can put down as little as 3.5% if your credit score is at least 580. According to recent data, the average down payment for FHA loan users is just $16,000, compared to $77,000 for those using conventional loans.

Imagine keeping $60,000 in your pocket—or using it for furniture, repairs, or that dream kitchen upgrade.

2. More Flexible Credit Score Requirements

Got a less-than-perfect credit score? Don’t sweat it. FHA loans are far more forgiving. While conventional loans often require credit scores of 700 or higher, FHA loans may be available to buyers with scores as low as 500 (with a 10% down payment) or 580 (with 3.5% down).

In a world where credit scores can feel like your financial report card, this kind of flexibility is a breath of fresh air.

3. Lower Mortgage Interest Rates

This might surprise you: FHA loan interest rates can often be lower than those for conventional mortgages. That’s because the government backing reduces risk for lenders, so they’re more willing to offer competitive rates.

And when your rate is lower, your monthly mortgage payment drops too. That means more money in your wallet every month—which makes affording your dream home a whole lot easier.

Let’s Talk Monthly Payments: Can FHA Loans Really Save You Money?

Absolutely. Between the lower interest rates and the smaller down payments, FHA loans can ease the two biggest financial pressures most first-time buyers face:

-

Saving up enough cash upfront

-

Managing the monthly payment once you move in

And remember, while FHA loans do require mortgage insurance (both an upfront premium and a monthly one), the overall affordability often still beats out conventional loans—especially for buyers with lower credit scores or limited savings.

It’s all about weighing your options. And sometimes, the FHA route makes a whole lot more sense.

When Is an FHA Loan the Right Move?

FHA loans aren’t one-size-fits-all, but they’re ideal if:

-

You’re buying your first home

-

You have a lower credit score

-

You don’t have a huge amount saved for a down payment

-

You want lower monthly payments

-

You’re okay with a few extra conditions (like mortgage insurance)

If you check any of these boxes, it’s worth having a conversation with a lender who knows the ins and outs of FHA lending.

What’s the Catch?

Alright, no program is perfect—and FHA loans do come with a few strings attached. Here’s what you need to know:

-

Mortgage Insurance is Required: You’ll pay two types of mortgage insurance—an upfront premium and a monthly fee.

-

Loan Limits Apply: You can’t buy a mansion with an FHA loan. There are caps based on where you live, so make sure your dream home fits the budget.

-

The Home Must Be Your Primary Residence: Investment properties and second homes aren’t eligible.

But for most first-time buyers, these trade-offs are totally manageable—especially when you weigh them against the benefits.

How to Get Started with an FHA Loan

Ready to take the plunge? Here’s your step-by-step guide:

-

Check Your Credit Score: Knowing where you stand helps you prepare.

-

Set Your Budget: Look at your income, expenses, and how much home you can realistically afford.

-

Find a Trusted Lender: Look for a lender experienced with FHA loans—they’ll walk you through the process and help you get pre-approved.

-

Start House Hunting: With pre-approval in hand, you’re ready to find the home that checks all your boxes.

-

Make an Offer and Close: Your lender will handle the rest—getting you from offer to keys-in-hand in a few weeks.

Bottom Line: FHA Loans Could Be Your Ticket to Homeownership

If the idea of buying your first home feels overwhelming, you’re not alone. Between sky-high prices and rising interest rates, it’s no wonder first-time buyers are feeling the pressure.

But FHA loans are a powerful tool that could make your dream of homeownership a reality—even if your credit isn’t perfect or your savings account isn’t stacked.

So, why not explore your options? Talk to a lender, run the numbers, and see if an FHA loan makes sense for you.

Because owning a home isn’t just a dream—it’s a goal you can actually reach.

P.S. Curious about your options or ready to talk to someone? A trusted lender can help you map out your journey and find the loan that fits your needs. Don’t wait—your dream home might be closer than you think.

Recent Posts

GET MORE INFORMATION