Closing Costs Explained: A State-by-State Guide Every Homebuyer Needs in 2025

Buying a home is one of life’s biggest milestones—but it also comes with a few financial surprises that can catch you off guard if you’re not prepared. One of the most overlooked? Closing costs.

You’ve probably heard the term before, but do you know what it actually covers? Or why your friend in another state might have paid thousands more—or less—than you? Let’s pull back the curtain and break down everything you need to know, including a state-by-state look at closing costs, what’s included, and tips on how to reduce them.

What Exactly Are Closing Costs?

Think of closing costs as the “final handshake” fees that wrap up your home purchase. They’re the expenses beyond your down payment that make your deal official and legal.

According to Freddie Mac, closing costs often include:

-

Loan application fees – the price of starting your mortgage paperwork

-

Credit report fees – so lenders know your financial story

-

Loan origination fees – basically, the cost of processing your loan

-

Appraisal fees – confirming your new home is worth what you’re paying

-

Home inspection – checking that the place is safe and sound

-

Title search and title insurance – ensuring you’re the rightful new owner

-

Attorney fees – required in some states for legal review

-

Homeowner’s insurance – protecting your new investment

-

Property survey – confirming boundaries and land details

In short, these aren’t optional add-ons—they’re essential for protecting both you and the lender.

National Averages vs. Local Realities

When you Google “closing costs,” you’ll usually see an estimate that says they range from 2% to 5% of the purchase price. That’s helpful as a broad guideline, but here’s the truth: those numbers don’t tell the full story.

Closing costs vary wildly depending on:

-

Local taxes and fees (like transfer taxes or recording fees)

-

Service costs in your area (title companies, lawyers, inspectors)

-

State regulations (laws differ on what must be included)

Imagine you’re ordering coffee. In some places, a latte might cost $3. In others, that same latte is $7—same product, different location. Closing costs work the same way.

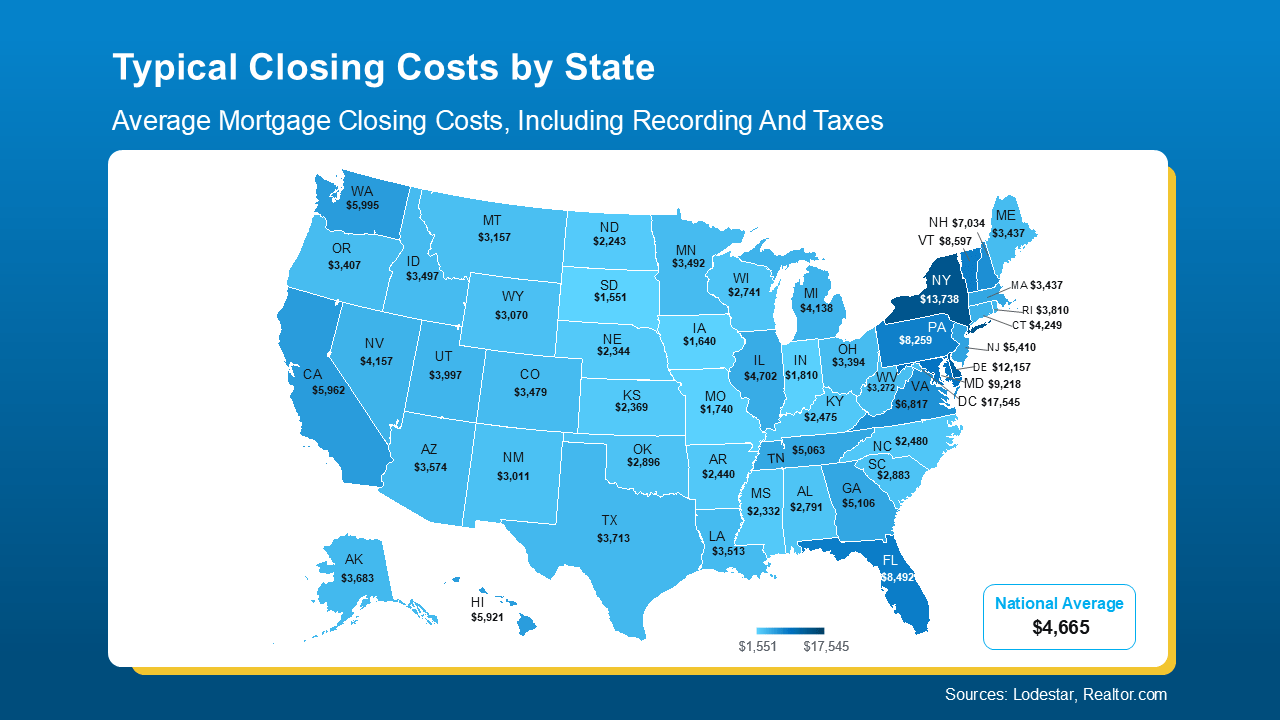

State-by-State Closing Costs: Why the Numbers Swing

For a median-priced home, some states have typical closing costs as low as $1,500 to $3,000. In others, you could be staring at a bill closer to $10,000 to $15,000.

Why such a big gap? It usually comes down to:

-

Taxes – High transfer or property taxes = higher closing costs.

-

Attorney requirements – Some states require lawyers, others don’t.

-

Local service rates – A title search in rural Kansas costs a lot less than one in New York City.

That’s why you can’t just rely on a national chart. If you’re planning to buy this year, you need to know what’s typical where you live (or plan to buy).

How to Estimate Your Closing Costs Like a Pro

Here’s the good news: you don’t have to guess. The best way to get a real number is to connect with:

-

A local real estate agent who knows the norms in your area

-

A trusted lender who can run the math for your loan type and location

They’ll give you a breakdown tailored to your situation—so you can budget with confidence before you even start house hunting.

Can You Lower Your Closing Costs? Absolutely.

While you can’t erase closing costs altogether, you can definitely shave them down. Here are a few tried-and-true strategies:

1. Negotiate With the Seller

Ask for concessions like a credit toward your closing costs. Sellers eager to close the deal may agree.

2. Shop Around for Homeowner’s Insurance

Don’t just go with the first quote. Comparing coverage and rates could save you hundreds.

3. Explore Assistance Programs

Many states, professions (like teachers or first responders), and even specific neighborhoods offer programs that help with closing costs. Ask your agent and lender what’s available locally.

4. Compare Lender Fees

Not all lenders charge the same for origination or application fees. A little comparison shopping can pay off big.

The Bottom Line

Closing costs aren’t just small add-ons—they’re a crucial part of your home-buying budget. And since they can swing dramatically depending on your state, the smartest move you can make is to learn your numbers early.

When you understand what’s included, why your location matters, and how to bring those costs down, you’re no longer walking into closing day blind—you’re walking in prepared and confident.

So, if buying a home is in your plans this year, start by asking your local agent or lender for a personalized estimate. Think of it as your roadmap to a smoother, less stressful closing.

Because at the end of the day, the keys to your dream home feel a lot lighter when you already know what’s waiting on the final bill.

Ready to see typical closing costs in your state? Let’s take a look and build a budget that works for you.

Recent Posts

GET MORE INFORMATION