Why More Homeowners Are Finally Letting Go of Their 3% Mortgage Rate

For the past few years, millions of homeowners have shared the same thought:

“I’d love to move… but I can’t give up my 3% mortgage rate.”

And honestly? That feeling makes total sense. Locking in a record-low interest rate felt like winning the financial lottery. For many, it was the smartest money move of their lifetime. Giving that up can feel like tossing a winning ticket in the trash.

But here’s the bigger truth most homeowners are now realizing:

A great interest rate can’t fix a home that no longer fits your life.

Life evolves. Families grow, careers change, priorities shift. What once felt like the perfect home might now feel too small, too far away, or simply out of sync with where you are today. And increasingly, homeowners across the country are choosing progress over perfection—even if it means trading a lower rate for a better life fit.

Let’s explore why more homeowners are finally breaking free from the so-called “lock-in effect,” what’s driving this shift, and how you can decide what’s right for your next move.

The Lock-In Effect: Why So Many Homeowners Stayed Put

The term lock-in effect became popular when mortgage rates surged after their historic lows. Homeowners with rates below 3% felt “locked” into their homes. Why?

Because selling meant buying again at a much higher interest rate—often double what they were paying.

For many, the math didn’t seem appealing:

-

Moving meant higher monthly payments.

-

Staying meant financial stability—even if the home wasn’t ideal anymore.

So homeowners froze. Moves were delayed. Houses went unsold. Life plans sat on hold.

But that freeze is starting to thaw.

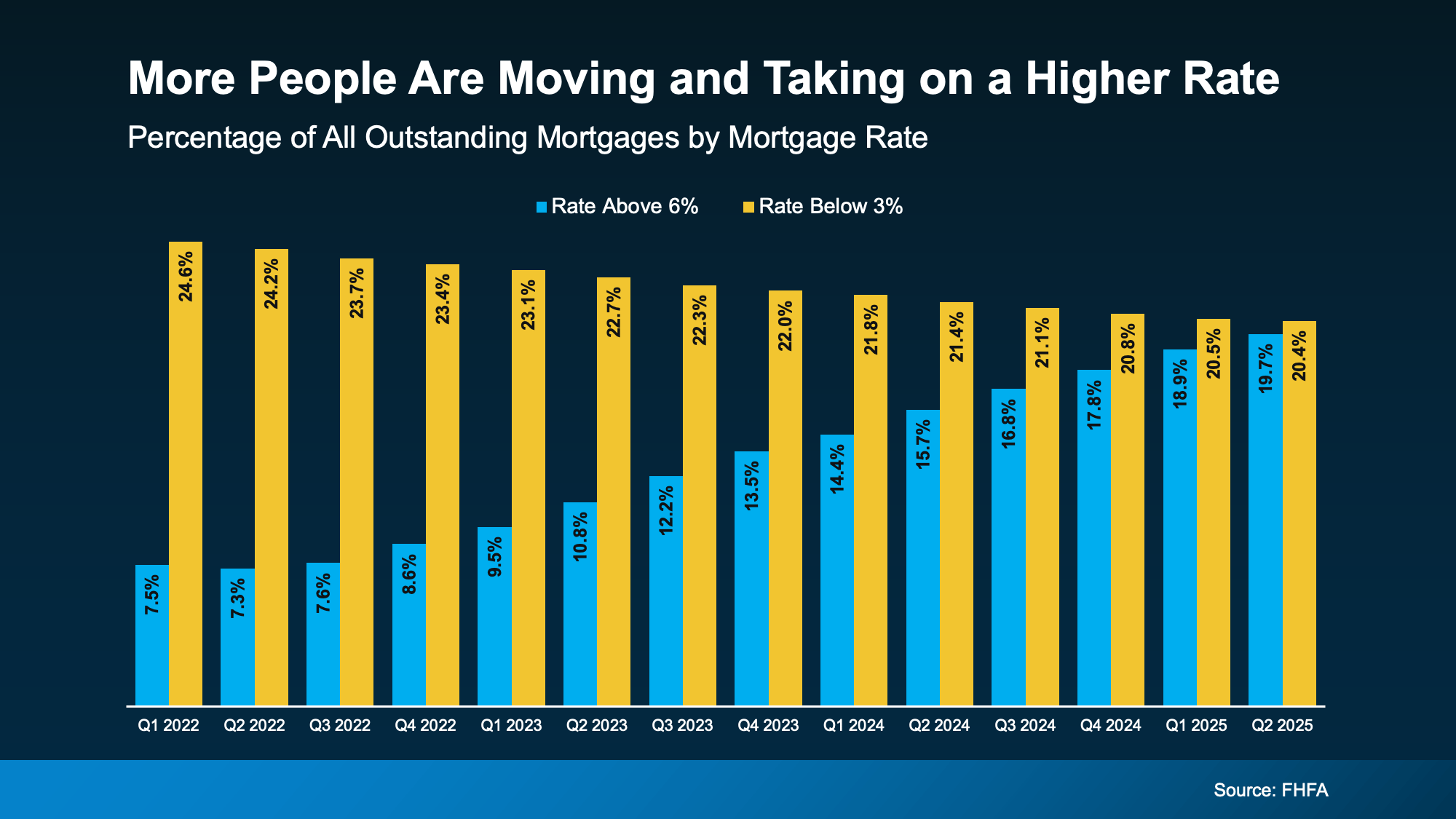

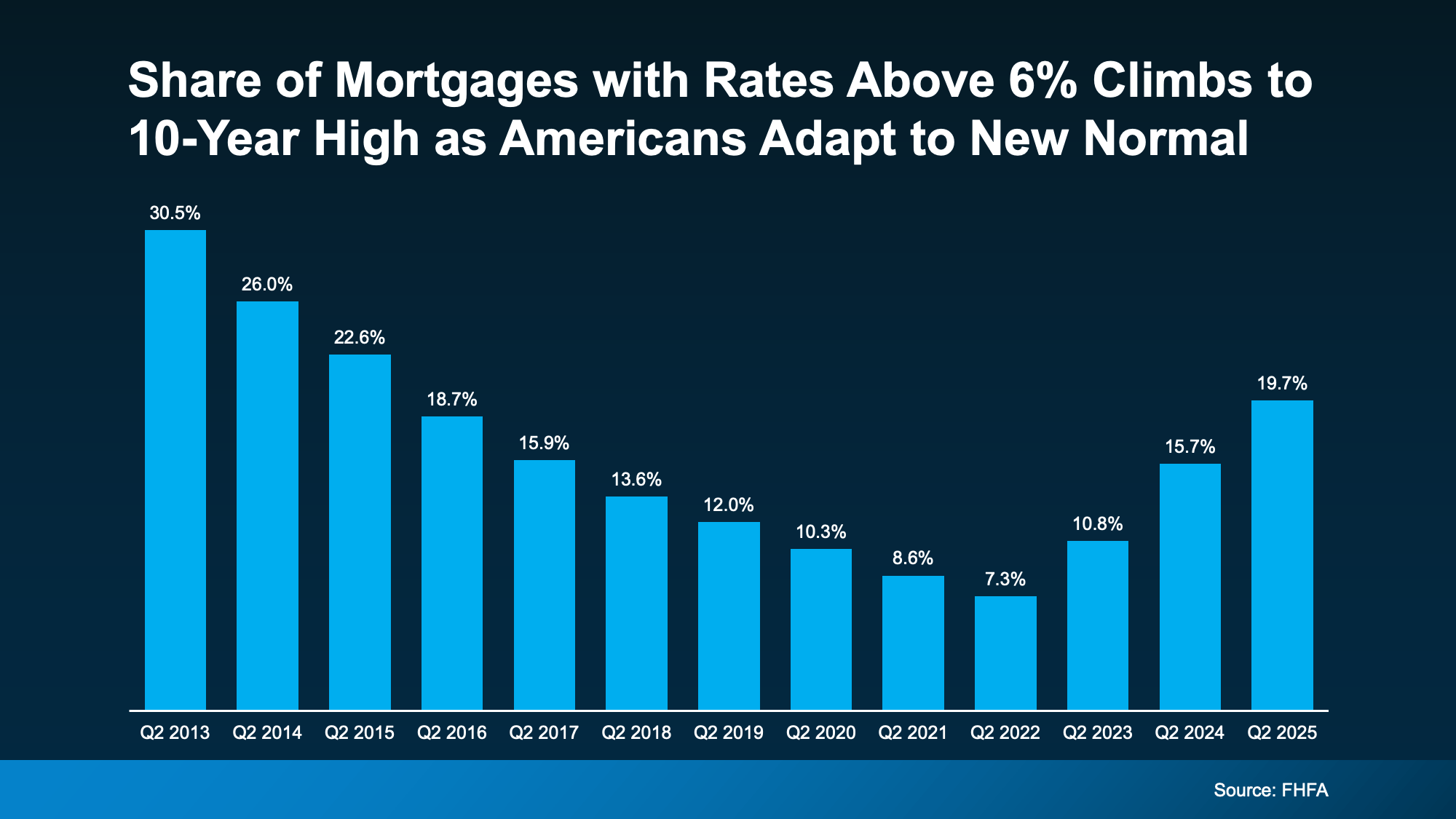

Data from the Federal Housing Finance Agency (FHFA) shows the percentage of homeowners holding sub-3% mortgage rates has been gradually shrinking. Meanwhile, the number of homeowners taking on rates above 6%—many of them existing homeowners making their next move—has been climbing.

Even more telling?

The share of mortgages with rates above 6% recently hit a 10-year high. This signals something important: people are adapting to modern mortgage rates as the new normal.

Why More Homeowners Are Choosing to Move Anyway

So what changed?

Life happened.

No one expects real life to pause for the sake of a financial optimization strategy. Your home isn’t just a spreadsheet entry—it’s where real moments unfold.

According to Redfin’s Head of Economic Research, Chen Zhao:

“More homeowners are deciding it’s worth moving even if it means giving up a lower mortgage rate. Life doesn’t stand still—people get new jobs, grow their families, downsize after retirement, or simply want to live in a different neighborhood. Those needs are starting to outweigh the financial benefit of clinging to a rock-bottom mortgage rate.”

Translation?

People are choosing lifestyle over loan numbers.

And increasingly, that choice is bringing peace—not regret.

The “5 Ds” That Push People to Move

Real estate experts often describe the life events that motivate people to move as the 5 Ds:

1. Diplomas – Career Growth

After finishing school or advancing professionally, earning potential increases. Your once-perfect starter home may feel too limiting as your career—and income—expand. You might want a home office, a shorter commute, or space that matches your upgraded lifestyle.

2. Diapers – Growing Families

Nothing highlights the need for space quite like welcoming a child. Suddenly, that cozy two-bedroom feels crowded. Storage disappears. Noise multiplies. And suddenly, more bedrooms, bigger yards, or access to better schools becomes non-negotiable.

3. Divorce – New Beginnings

Major relationship changes almost always mean housing changes, too. Whether merging households or starting fresh solo, these moments often demand a new living arrangement that aligns with your new chapter.

4. Downsizing – Simplifying Life

For empty nesters or retirees, the dream shifts. Maintaining a large home loses appeal. Smaller spaces, single-level floor plans, and lower maintenance feel freeing rather than limiting.

5. Death – Relocating for What Matters

Losing a loved one changes perspective. Many homeowners choose to move closer to family or into communities offering support and connection. When life shortens emotionally, distance loses its appeal.

All five reasons have one thing in common:

They’re personal, emotional, and impossible to postpone forever.

Why Staying for the Rate Can Cost You More Than You Think

At first glance, staying put can seem like the financially smarter move. But consider the hidden costs:

-

Living too far from work raises commuting expenses and stress.

-

Outgrowing your home means sacrificing comfort and functionality.

-

Waiting for market “perfection” delays meeting your family’s actual needs.

-

Emotional stagnation slows personal growth and happiness.

A low mortgage rate doesn’t cure dissatisfaction.

Think of it like wearing a perfectly priced pair of shoes… that don’t fit anymore. The deal doesn’t matter if the comfort is gone.

The Reality: Most Sellers Have Already Been Waiting Long Enough

According to Realtor.com, nearly two out of three homeowners considering selling have already delayed their move for over a year.

That’s not a tactical pause—that’s a full lifestyle delay.

One year turns into two. Two become three. And suddenly, real life has been postponed in favor of holding onto a number on paper.

So maybe the better question isn’t:

“Should I move?”

But rather:

“How much longer am I willing to stay somewhere that doesn’t truly serve my life?”

Mortgage Rates Are Easing—And So Is the Pressure

The financial picture isn’t as bleak as many fear.

Mortgage rates have already come down slightly from their earlier peaks. Industry forecasts suggest rates may continue easing modestly into 2026, making future purchases more manageable.

Is that 3% coming back tomorrow? Probably not.

But today’s rates aren’t the crisis headlines made them out to be. They’re workable—and when paired with rising incomes and life-driven motivation, many homeowners see that the move finally makes sense.

How to Decide If Now Is Your Moment

Before deciding whether to stay or move, ask yourself:

-

Does my home still match my lifestyle?

-

Am I sacrificing comfort, time, or family needs to keep a low rate?

-

Have I been waiting because it’s truly best—or because it’s comfortable to wait?

Remember:

A home should support your life—not trap it.

When your daily reality no longer aligns with your living space, the decision begins to clarify itself.

Why Lifestyle Often Beats the Loan Rate

Emotionally fit homes deliver more than ROI:

-

Better mental health

-

Improved family harmony

-

Reduced stress

-

Greater work-life balance

These benefits don’t show up in spreadsheets—but they shape everyday quality of life.

A slightly higher mortgage payment can be quickly outweighed by:

-

Shorter commutes

-

Better neighborhood alignment

-

Increased space and comfort

-

Proximity to loved ones

And those are returns that compound daily.

Bottom Line: Life Doesn’t Wait for the Perfect Rate—And You Shouldn’t Either

The era of waiting for the “perfect mortgage rate” has begun to fade. More homeowners are realizing that waiting indefinitely costs more in life satisfaction than any rate increase ever could.

Your time, happiness, and personal growth matter more than squeezing the last decimal out of your interest rate.

With mortgage rates already down from their peak and expected to dip slightly further in 2026, moving is more feasible now than many realize.

So if you’ve been holding onto a rate that no longer matches your reality, maybe it’s time to shift your focus from numbers… to living the life you actually want.

Because a great life is worth far more than a perfectly low interest rate.

If you’re ready to explore what’s possible in your market and see how your next move could work for you, let’s start the conversation.

Recent Posts

GET MORE INFORMATION