The Credit Score Myth That’s Quietly Keeping Homebuyers on the Sidelines

Let’s clear the air right away: most people who want to buy a home aren’t waiting because they’re indecisive or lazy. They’re waiting because they believe they’re disqualified before they even start. And more often than not, the culprit is a misunderstood credit score.

Sound familiar?

You check your credit, see a number that isn’t magazine-cover perfect, and instantly think, “Welp, homeownership isn’t for me… at least not anytime soon.” So you keep renting. You keep waiting. And you keep assuming the door is closed.

But what if that door has been unlocked this whole time?

Let’s talk about the credit score myth that’s holding would-be buyers back—and why it’s time to stop letting it run the show.

Why So Many Buyers Think Their Credit Isn’t Good Enough

Here’s the surprising truth: people aren’t opting out of buying homes because they don’t want to buy. They’re opting out because they think they can’t.

According to a Bankrate survey, about 42% of Americans believe you need excellent credit to qualify for a mortgage. That’s nearly half the population walking around with a false assumption.

So when renters are asked why they haven’t purchased a home yet, one answer keeps popping up like a bad song on repeat:

“My credit isn’t good enough.”

Maybe that’s your answer too.

You see stories online about buyers with flawless 800+ scores. You hear friends say lenders are “super strict now.” And suddenly, buying a home feels like trying to get into an exclusive club where your name will never be on the list.

But here’s the thing—those assumptions are doing way more damage than your actual credit score ever could.

The Truth: You Don’t Need Perfect Credit to Buy a Home

Let’s bust the biggest myth first.

You do not need perfect—or even excellent—credit to buy a home.

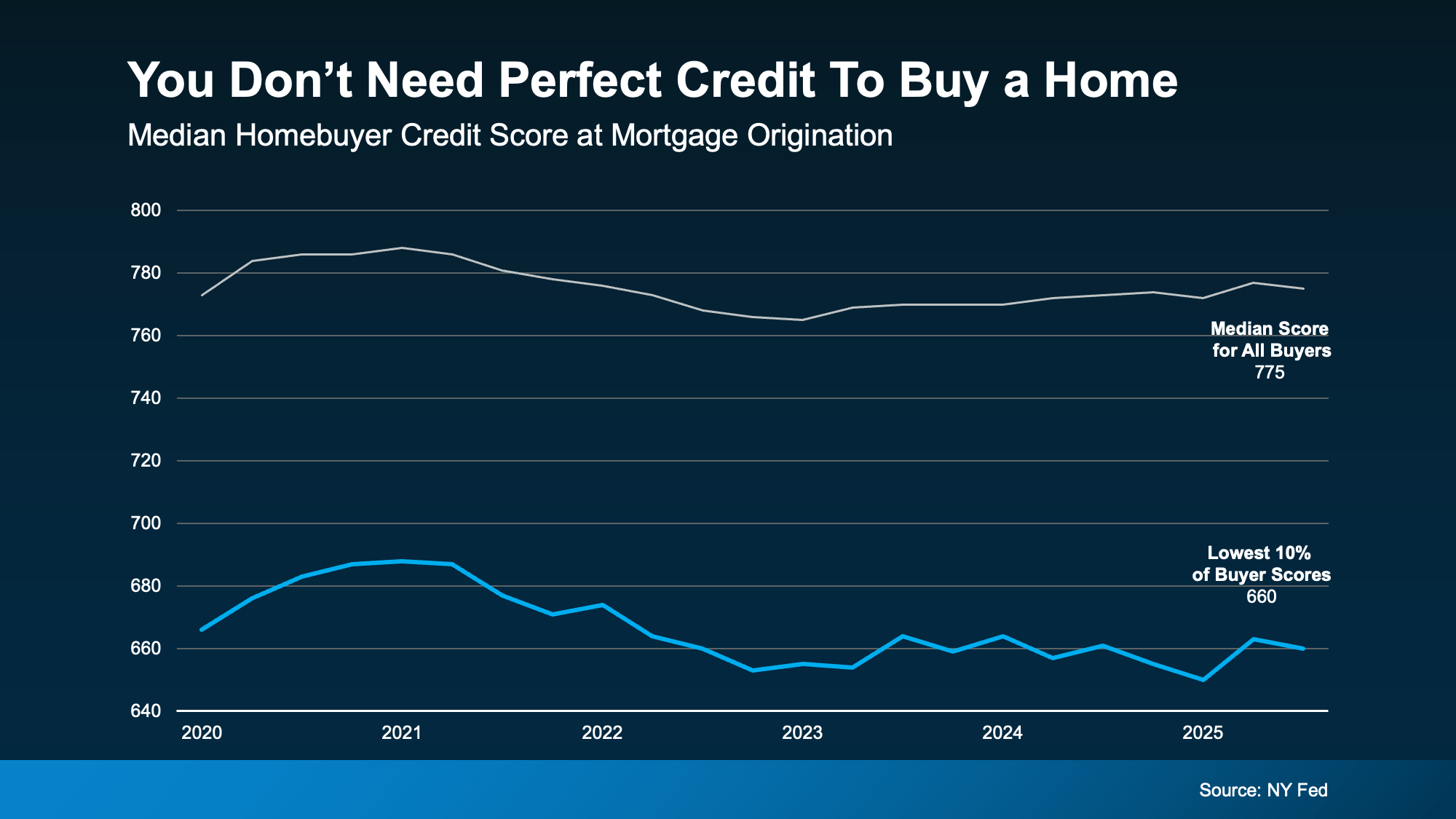

Yes, many buyers today have strong credit. According to data from the New York Federal Reserve, the median credit score for recent homebuyers is around 775. That number gets thrown around a lot, and understandably so. It sounds official. It sounds intimidating.

But here’s what most people miss:

A median is not a minimum.

Just because the average buyer has a higher score doesn’t mean lenders require that score from everyone. That’s like saying you can’t join a gym unless you already have a six-pack. Makes no sense, right?

Real Buyers Are Getting Approved With Lower Credit Scores

Let’s look beyond the averages.

Data shows that around 10% of recent homebuyers had credit scores hovering near 660. Some were a little higher. Some were lower. But the point is this: buyers with scores in the 600s are still getting mortgages.

Read that again.

If your credit score starts with a “6,” the door isn’t slammed shut. It’s not even locked.

This alone should be a wake-up call for anyone who’s been self-rejecting before ever speaking to a lender.

Why There’s No “Magic” Credit Score Cutoff

One of the biggest misconceptions in real estate is the idea that there’s a single, universal credit score you must have to qualify for a mortgage.

There isn’t.

In fact, FICO itself explains it best:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single ‘cutoff score’ used by all lenders, and there are many additional factors that lenders may use…”

In plain English?

Every lender is different.

They look at:

-

Your income

-

Your employment history

-

Your debt-to-income ratio

-

Your savings

-

Your payment patterns

Your credit score is important, yes—but it’s just one piece of a much bigger puzzle.

Why Credit Scores Feel Scarier Than They Actually Are

Credit scores have a funny way of messing with our heads.

They’re numerical, judgmental, and oddly emotional. A single number makes us feel responsible, behind, or “not adult enough.” It’s like getting a report card that follows you everywhere.

But here’s the thing: lenders don’t see your credit score the way you do.

You see it as a verdict.

They see it as data.

And data can be worked with.

A slightly lower score doesn’t automatically mean “no.” Often, it just means different loan options, different rates, or a different strategy.

That’s not failure—that’s flexibility.

What Really Matters More Than a “Perfect” Score

Think of your credit score like a first impression at a job interview. It matters—but it’s not the whole conversation.

Lenders care deeply about consistency.

Do you pay your bills on time?

Is your debt manageable?

Is your income stable?

Someone with a 660 score who pays consistently and earns reliable income may be seen as less risky than someone with a 780 score and unstable finances.

Numbers don’t tell the full story—patterns do.

Why Talking to a Lender Changes Everything

Here’s the step most would-be buyers skip—and it’s costing them years of waiting.

They never talk to a lender.

Instead, they assume. They Google. They compare themselves to strangers online. And they quietly decide they’re “not ready.”

But a quick conversation with a trusted local lender can completely flip the script.

A lender can:

-

Tell you what loan programs you qualify for

-

Explain realistic credit score expectations

-

Show you how close (or already eligible) you are

-

Help you create a simple improvement plan if needed

And no, this doesn’t mean you’re committing to buy tomorrow. It just means you’re replacing assumptions with actual information.

Waiting for “Perfect” Credit Can Cost You More Than You Think

Here’s a tough but honest question:

How much is waiting costing you?

While you’re sitting on the sidelines trying to “fix” your credit:

-

Rents keep rising

-

Home prices continue to change

-

You’re paying someone else’s mortgage instead of building equity

Waiting for a perfect score is like waiting for the “perfect time” to start a family or switch careers. That moment rarely arrives. And even if it does, it often arrives too late to matter.

Progress beats perfection—every single time.

You Don’t Need All the Answers to Start

Let’s make this crystal clear.

You don’t need:

-

A flawless credit score

-

A massive savings account

-

A 10-year plan

-

Everything figured out

You just need a starting point.

Buying a home isn’t a test you either pass or fail. It’s a process. And the first step is simply understanding where you stand today—not where you think you should be.

The Bottom Line: Don’t Let a Myth Make the Decision for You

Your credit score matters—but it doesn’t have to be perfect.

If credit has been the reason you’ve been waiting, it may be time to challenge that assumption. Plenty of buyers with less-than-ideal scores are already homeowners. There’s a real chance you could be one of them.

The only way to know for sure?

Start the conversation.

Ask the questions.

Get real answers—not myths.

Because sometimes, the biggest thing holding you back isn’t your credit score at all.

It’s the story you’ve been telling yourself about it.

Recent Posts

GET MORE INFORMATION