3 Powerful Reasons Home Affordability Is Finally Improving This Fall

For the last few years, buying a home has felt like chasing a moving train—you’re running as fast as you can, but the numbers just don’t add up. Home prices soared to record highs, mortgage rates climbed, and a lot of hopeful buyers hit the brakes. If that sounds like you, you weren’t alone.

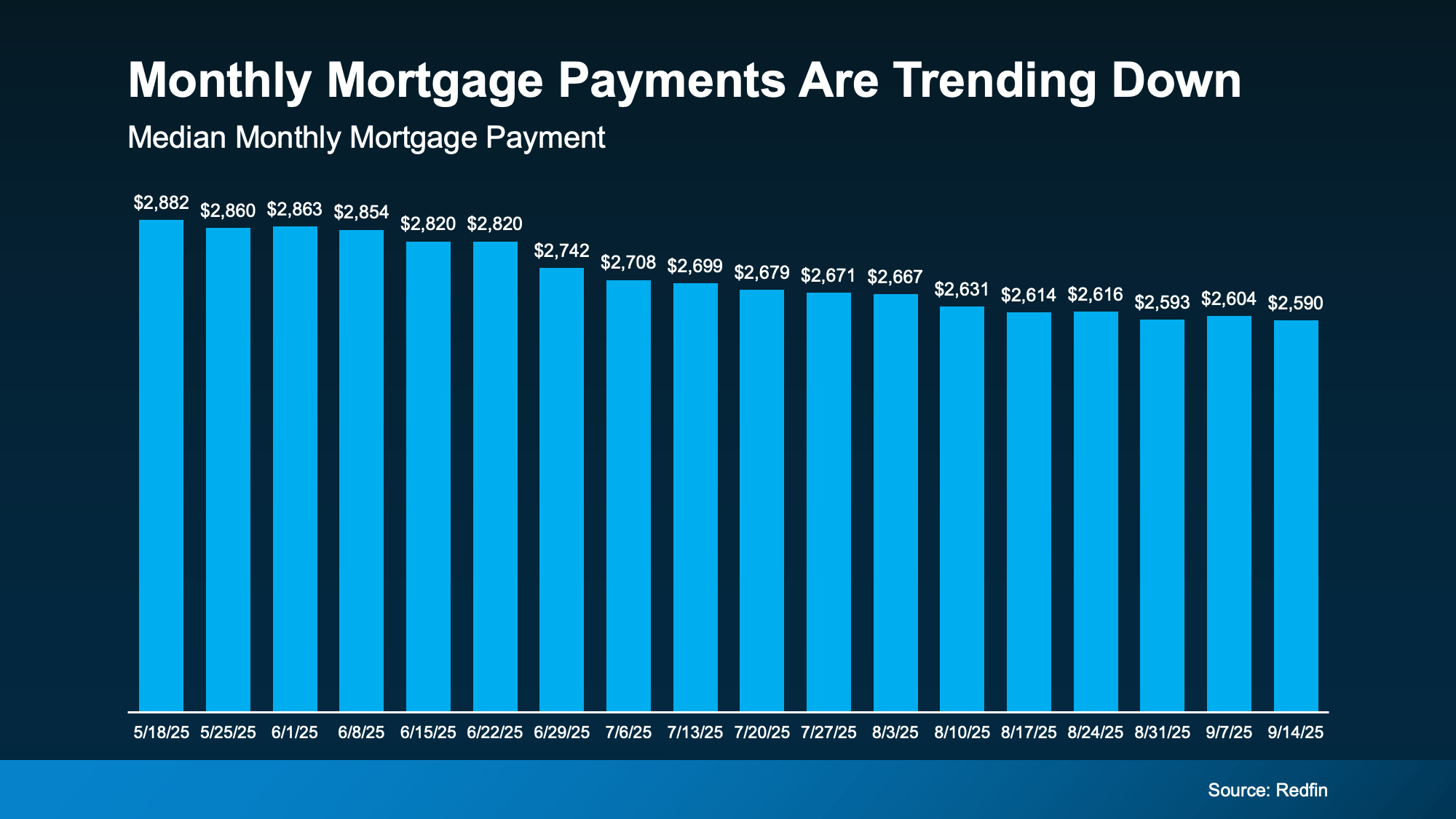

But here’s the good news: this fall, the housing market is showing some promising signs that affordability is finally heading in the right direction. The shift isn’t dramatic overnight, but it’s enough to make a real difference in your wallet. According to recent data from Redfin, the typical monthly mortgage payment has dropped by nearly $290 compared to just a few months ago. That’s not pocket change—that’s money you can actually feel each month.

So, what’s behind this change? It all comes down to three major players: mortgage rates, home prices, and wages. And for the first time in a while, all three are finally leaning in favor of buyers.

Let’s break down what this means for you and why now may be the opportunity you’ve been waiting for.

1. Mortgage Rates Are Finally Cooling Down

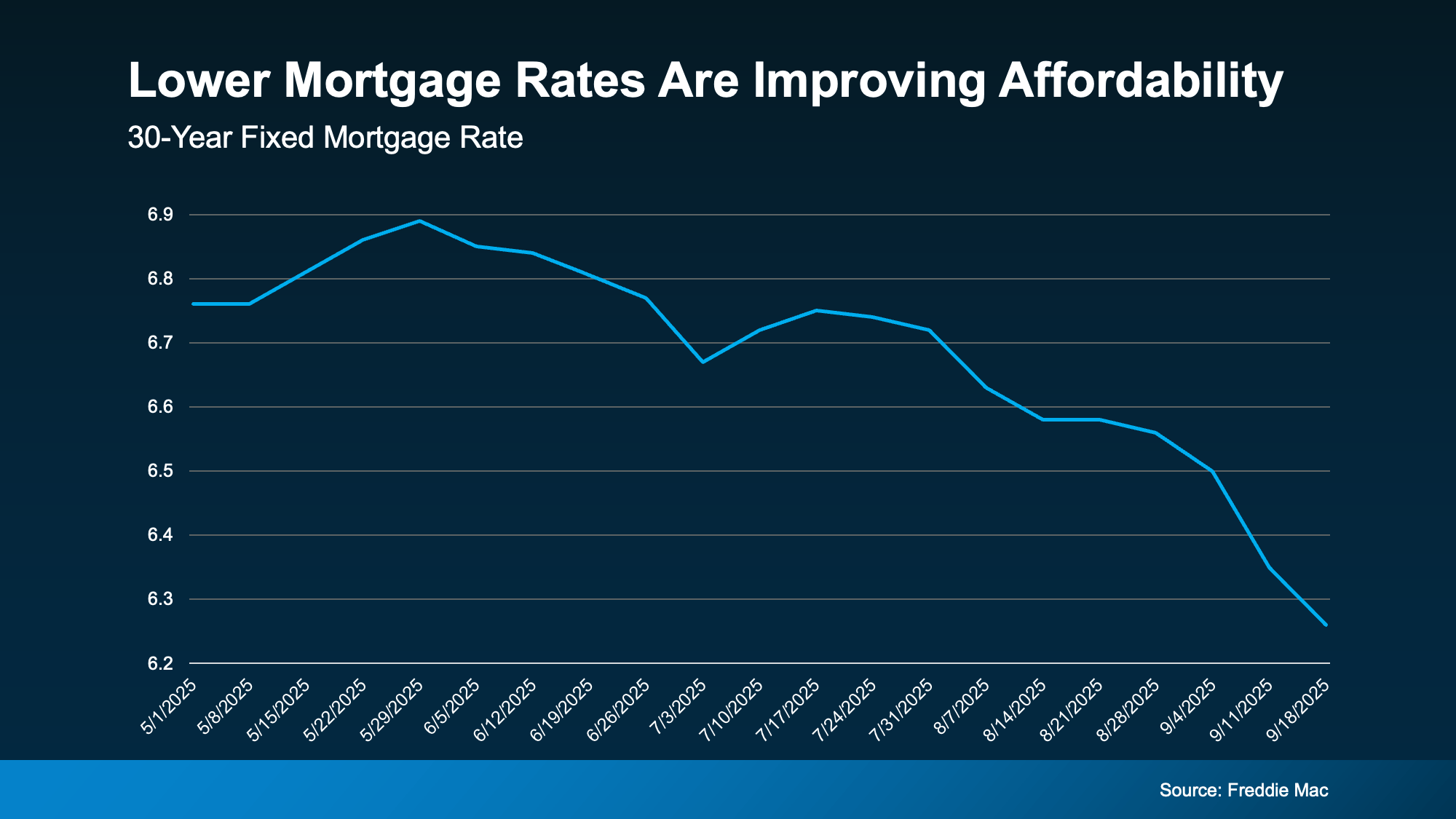

If you’ve been watching mortgage rates this year, you know the rollercoaster has been wild. Back in May, average rates hovered around 7%—enough to make many buyers rethink their plans. Fast forward to now, and rates have eased closer to 6.3%. At first glance, that might not seem like a game-changer, but in real estate, even small rate drops can create big savings.

Here’s a quick example:

Imagine you’re taking out a $400,000 mortgage. At 7%, your monthly principal and interest payment would be a lot steeper compared to locking in at 6.3%. In fact, the difference comes out to roughly $190 less every month. That’s over $2,200 saved in a year, just from the rate shift alone.

Think of it like filling up your gas tank. A 70-cent drop per gallon may not sound like much, but after a few weeks, your wallet definitely notices the difference.

And you’re not the only one noticing. Joel Kan, Vice President and Deputy Chief Economist at the Mortgage Bankers Association (MBA), shared that the recent dip in rates has triggered a surge in demand:

“The downward rate movement spurred the strongest week of borrower demand since 2022 . . . Purchase applications increased to the highest level since July and continued to run more than 20 percent ahead of last year’s pace.”

That means more buyers are jumping back in—and for good reason. Lower rates don’t just make homes more affordable; they can also give you an edge in securing financing before competition heats up further.

2. Home Prices Are Slowing Down

For years, it felt like home prices were racing ahead without looking back. Double-digit growth became the norm in many markets, leaving buyers frustrated and stretched thin. But now? That trend is cooling.

Nationally, home price growth has slowed to the low single digits, and according to Odeta Kushi, Deputy Chief Economist at First American:

“National home price growth remains positive, but muted — low single digits — and we expect this trend to continue in the second half of the year.”

This moderation is a breath of fresh air. For buyers, slower growth means stability—you can plan your budget with more confidence without worrying that prices will skyrocket in the next few months. In some local markets, prices have even dipped slightly, creating rare pockets of opportunity where homes are more attainable than they were just last year.

Think of it like grocery shopping. When prices of your favorite products rise every single week, it’s exhausting to keep up. But when prices stabilize—or even drop—you can finally plan meals without stretching your budget. That’s exactly what’s happening in housing right now.

For first-time buyers, this shift is particularly valuable. It doesn’t mean homes are suddenly “cheap,” but it does mean they’re no longer racing out of reach at the same pace they were before.

3. Wages Are Rising Faster Than Prices

Here’s the third piece of the puzzle: your paycheck. According to the Bureau of Labor Statistics (BLS), wages have been climbing at an annual pace of about 4%. That’s significant because, for once, income growth is outpacing home price growth.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains why that matters:

“Wage growth is now comfortably outpacing home price growth, and buyers have more choices.”

In simple terms, your dollar stretches a little further than it did before. Even if it’s not a massive jump, every percentage point of wage growth matters when you’re trying to save for a down payment, cover closing costs, or handle monthly payments.

Picture it this way: imagine you’re filling a leaky bucket (your budget). For years, rising prices meant more water was draining out than going in. Now, with wages rising faster, you’re finally putting in more than you’re losing. It doesn’t fix the problem instantly, but it helps you keep up.

What This Means for Buyers This Fall

Put it all together—lower mortgage rates, slower home price growth, and stronger wages—and you’ve got a housing market that feels more approachable than it did earlier this year. Affordability is still tight (no sugarcoating that), but it’s improving, and the numbers are starting to work out better for many buyers.

According to Redfin’s data, the typical monthly mortgage payment is already about $290 lower than it was just months ago. That’s a tangible improvement that could open the door for buyers who were previously priced out.

So, what does this mean for you? It might be the right time to dust off your home-buying plans. Whether you’ve been casually browsing Zillow at midnight or actively saving for a down payment, the landscape is shifting in your favor.

Should You Buy Now or Wait?

This is the million-dollar question—and the answer depends on your situation. If you’re financially ready (steady income, manageable debt, and a solid down payment), now could be an excellent time to move forward before rates or prices shift again. Remember, real estate markets are constantly in flux.

If you wait, there’s always the chance that rates could rise back up or competition could intensify as more buyers re-enter the market. On the flip side, if you need more time to save or improve your credit, waiting could still pay off, especially since affordability trends are moving in a positive direction.

The key is to run the numbers. Compare what your budget looked like six months ago versus today. With rates, prices, and wages all aligning more favorably, you might find that what felt impossible earlier this year is now within reach.

Bottom Line

The housing market isn’t suddenly “cheap,” but it’s finally bending in favor of buyers this fall. With mortgage rates easing, home prices stabilizing, and wages on the rise, the dream of homeownership feels a little less out of reach.

So, if you’ve been wondering whether now is the time to turn window-shopping into key-turning, it might be worth revisiting your options.

Ready to find out if the numbers work for you? Let’s crunch them together. We’ll look at your budget, review current market conditions, and see if this fall is the season you finally step into the home you’ve been waiting for.

Recent Posts

GET MORE INFORMATION