Adjustable-Rate Mortgages: The Risky-Smart Strategy Homebuyers Are Turning To in 2025

Thinking about getting a mortgage but paralyzed by today’s sky-high interest rates? You're not alone. With soaring home prices and painfully steep borrowing costs, buyers are getting creative—and one financing option making a serious comeback is the Adjustable-Rate Mortgage, or ARM.

Now, before you start having flashbacks to the 2008 housing crash, hear me out. Modern ARMs aren’t the ticking time bombs they once were. In fact, under the right circumstances, they could be a smart move. So, buckle in—we’re diving deep into how ARMs work, their benefits and risks, and whether this flexible mortgage might just be your ticket to homeownership in today’s volatile market.

What Is an Adjustable-Rate Mortgage (ARM), Really?

Let’s break it down without the jargon.

A fixed-rate mortgage is like getting married to your interest rate—you’re in it for the long haul. It doesn’t change, and your monthly payment stays predictable for 15, 20, or even 30 years.

But an adjustable-rate mortgage is more like dating. It starts out sweet—with a low introductory interest rate (cue the romance)—but after a set period (usually 5, 7, or 10 years), it can change. And depending on the market, that rate could go up... or down.

How It Works: Fixed Period vs Adjustment Period

With an ARM, your loan has two phases:

-

Introductory Fixed Period: For the first few years (say 5, 7, or 10), your interest rate stays low and stable.

-

Adjustment Period: After that, your rate resets—usually once a year—and it’s tied to a financial index (like the SOFR or the Treasury Index). This means your monthly payments could rise or fall based on market conditions.

For example: You get a 5/1 ARM. That means your rate is fixed for the first 5 years, then adjusts annually after that.

Sounds risky? Yes and no. Let’s keep going.

Why Are Homebuyers Suddenly Flirting With ARMs Again?

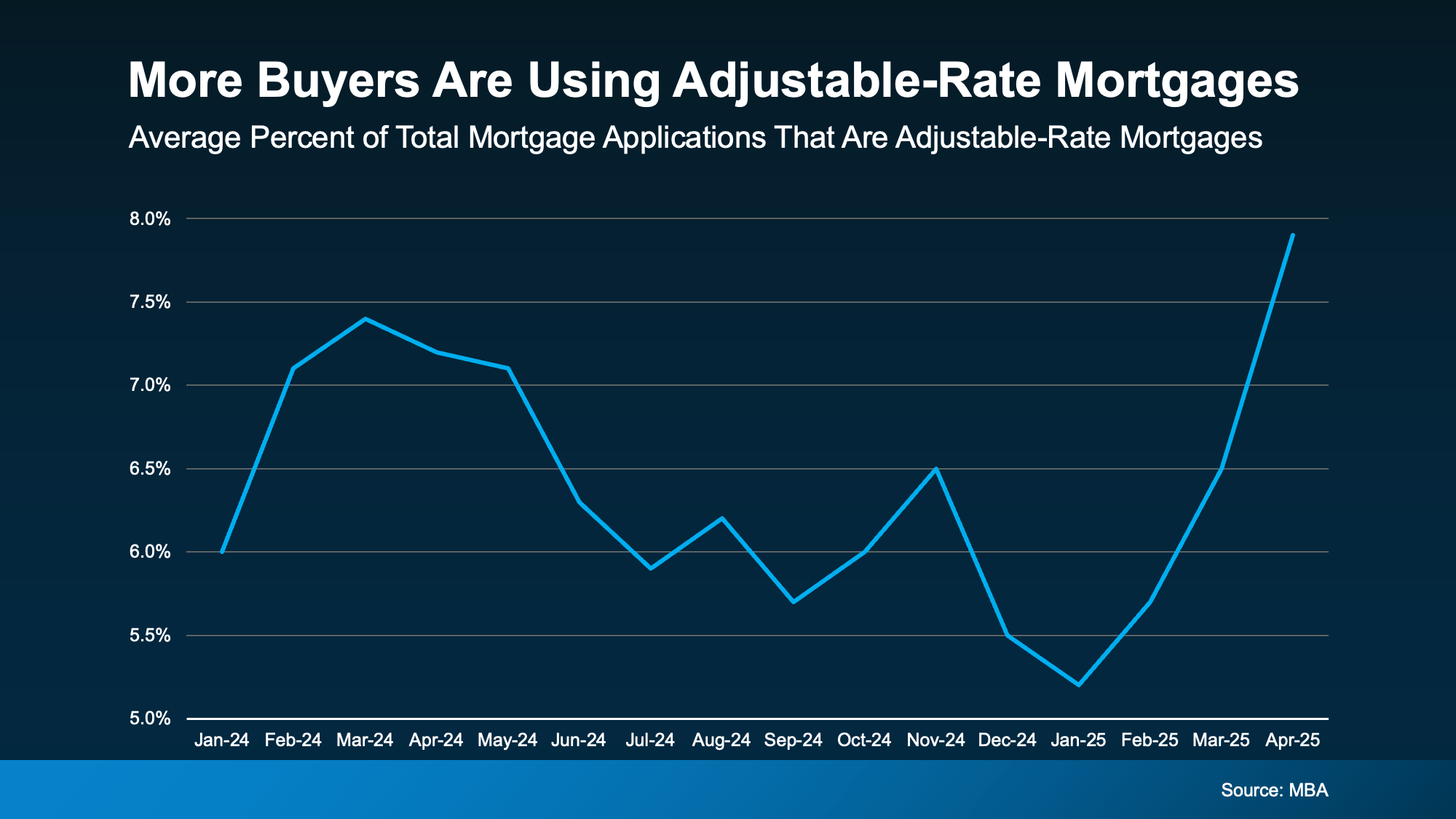

Mortgage rates are currently flirting with historic highs—and for many buyers, traditional fixed loans are pricing them out of the market. ARMs are becoming the “life hack” of home financing because they usually start with a significantly lower interest rate than a fixed-rate loan.

According to recent data from the Mortgage Bankers Association (MBA), ARM applications are rising as affordability tightens.

But is this just a short-term fix or a long-term trap?

Pros of Adjustable-Rate Mortgages: Why They’re Worth Considering

Let’s talk perks. Here’s why ARMs might actually make sense:

✅ Lower Initial Payments

The biggest draw? That juicy low starting rate. For the first few years, you’ll likely pay less each month than you would with a fixed-rate mortgage.

✅ Buy More House

Lower rates = more buying power. You could potentially afford a bigger or better-located home—without inflating your budget.

✅ Great for Short-Term Homeowners

Planning to move, sell, or refinance before the rate adjusts? Then why lock into a higher fixed rate? An ARM could save you thousands if you’re not planning to stay long-term.

✅ Rates Could Drop

If interest rates fall in the future, your payments might actually decrease after your initial fixed term—unlike a fixed mortgage, which stays the same no matter what.

Cons of ARMs: What Could Go Wrong?

Now for the flip side—because this isn’t all sunshine and low interest.

❌ Unpredictable Future Payments

Once your initial term ends, your monthly payment becomes a wild card. If rates shoot up, so does your mortgage bill—and that can be a budget-buster.

❌ Long-Term Risk

Still living in your home after the fixed period? You could be facing much higher costs down the road. If you can’t refinance or sell in time, you’re stuck.

❌ Complexity and Confusion

Caps, indexes, margins... ARMs aren’t as simple as fixed-rate loans. If you don’t understand the mechanics, you could be blindsided by rate hikes.

ARM Lingo You Need to Know (Without the Headache)

Here’s a cheat sheet so you sound smart in front of your lender:

-

Index: The benchmark rate your ARM is based on.

-

Margin: The number your lender adds to the index to set your new rate.

-

Caps: Limits on how much your interest rate can increase at each adjustment and over the life of the loan (super important).

-

Fully Indexed Rate: The index + margin = your actual adjustable rate.

Pro tip: Always ask your lender about rate caps. These are your safety nets.

Who Should Consider an ARM?

ARMs aren’t one-size-fits-all. Here’s who they work best for:

🏃♂️ Short-Term Buyers

If you know you'll sell or refinance before the adjustment period hits, why not take advantage of the lower rate now?

📈 Professionals With Rising Income

Expecting big raises or income growth in a few years? An ARM’s future higher payments might be easier to handle later.

🔄 Refinance Strategists

If you’re comfortable watching rates and jumping on a refinance when the time is right, an ARM could be your financial playground.

Who Should Steer Clear?

If any of these sound like you, think twice before choosing an ARM:

-

You’re planning to stay in the home long-term.

-

You live on a tight or fixed income.

-

You hate financial uncertainty.

-

You’re not comfortable tracking market trends or refinancing.

What the Experts Say

Business Insider puts it simply:

“Adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. That means if average rates have gone up, your mortgage payment will increase. If they've gone down, your payment will decrease.”

Barron’s adds:

“That’s a plus for borrowers if rates come down in the future, or if a borrower sells before the fixed period ends, but can lead to higher costs if they hold on to their home and rates go up.”

Translation? Don’t gamble unless you know the odds.

Key Questions to Ask Before Choosing an ARM

Thinking about going the ARM route? Here’s what you need to ask your lender:

-

What’s the starting interest rate and for how long?

-

How often does the rate adjust?

-

What index is it tied to?

-

What are the rate caps (initial, periodic, and lifetime)?

-

What’s the worst-case payment scenario?

-

Can I afford the payments if the rate maxes out?

Final Thoughts: Is an ARM Right for You?

Adjustable-rate mortgages have a bit of a reputation—but like many things in life, they’re not inherently bad. They just need to be used wisely.

For buyers with short-term plans or a strong grip on their finances, ARMs can be a strategic way to save money and boost affordability right now. But for others, the long-term risk may not be worth the reward.

Bottom line? Talk to your lender. Talk to your financial advisor. Crunch the numbers. And make sure you understand exactly what you’re signing up for. The more you know, the better prepared you’ll be to make a confident, informed decision.

Because when it comes to your mortgage, guessing is not a strategy—it’s a gamble. Choose wisely.

TL;DR – Quick Recap

| Pros | Cons |

|---|---|

| Lower initial payments | Future payment uncertainty |

| Increased buying power | Higher long-term cost risk |

| Ideal for short-term homeowners | Complex terms and conditions |

| Potential for lower future rates | Could be risky if staying long-term |

Need help comparing ARM vs fixed-rate loans for your unique situation? Don't wing it—talk to a mortgage expert and make a move that aligns with your long-term goals.

Because your mortgage shouldn’t just get you into a home—it should keep you there comfortably.

Recent Posts

GET MORE INFORMATION