Ever Thought About Using Your Home Equity to Help Your Kids Buy Their First Home?

Let’s face it—being a homeowner today means you’ve likely built up a pretty solid chunk of equity. Maybe without even trying. Just by paying your mortgage and riding the wave of rising property values, your home has turned into a financial powerhouse.

But what if we told you that this equity isn’t just a number on paper? What if it could be the key to helping your kids finally break into the housing market?

Let’s dig into how you can turn your home equity into a meaningful head start for your children—and why more and more parents are doing just that.

What Exactly Is Home Equity?

Before we dive into the hows and whys, let’s get one thing straight: home equity is the difference between what your home is worth and what you still owe on your mortgage.

Say your home is worth $500,000 and you owe $200,000. That means you’ve got $300,000 in equity just sitting there.

Sound like a lot? That’s because it is.

According to recent data from Cotality (previously known as CoreLogic), the average homeowner with a mortgage has around $311,000 in equity. That’s a serious asset—and it can be leveraged in smart, impactful ways.

Why Your Kids Might Need Help Getting Into a Home

Let’s be real: buying a house in today’s market is no walk in the park. With high home prices, interest rate fluctuations, and tight inventory, many first-time buyers are struggling. Even with a good job and a savings plan, homeownership can feel just out of reach.

And that’s where you come in.

You’ve built wealth through homeownership. Now, you have the opportunity to pass on a slice of that stability by using a portion of your equity to help your child buy their first home.

You're Not Alone—Many Parents Are Already Doing It

Here’s the thing: you’re not the first parent to think about this. And you definitely won’t be the last.

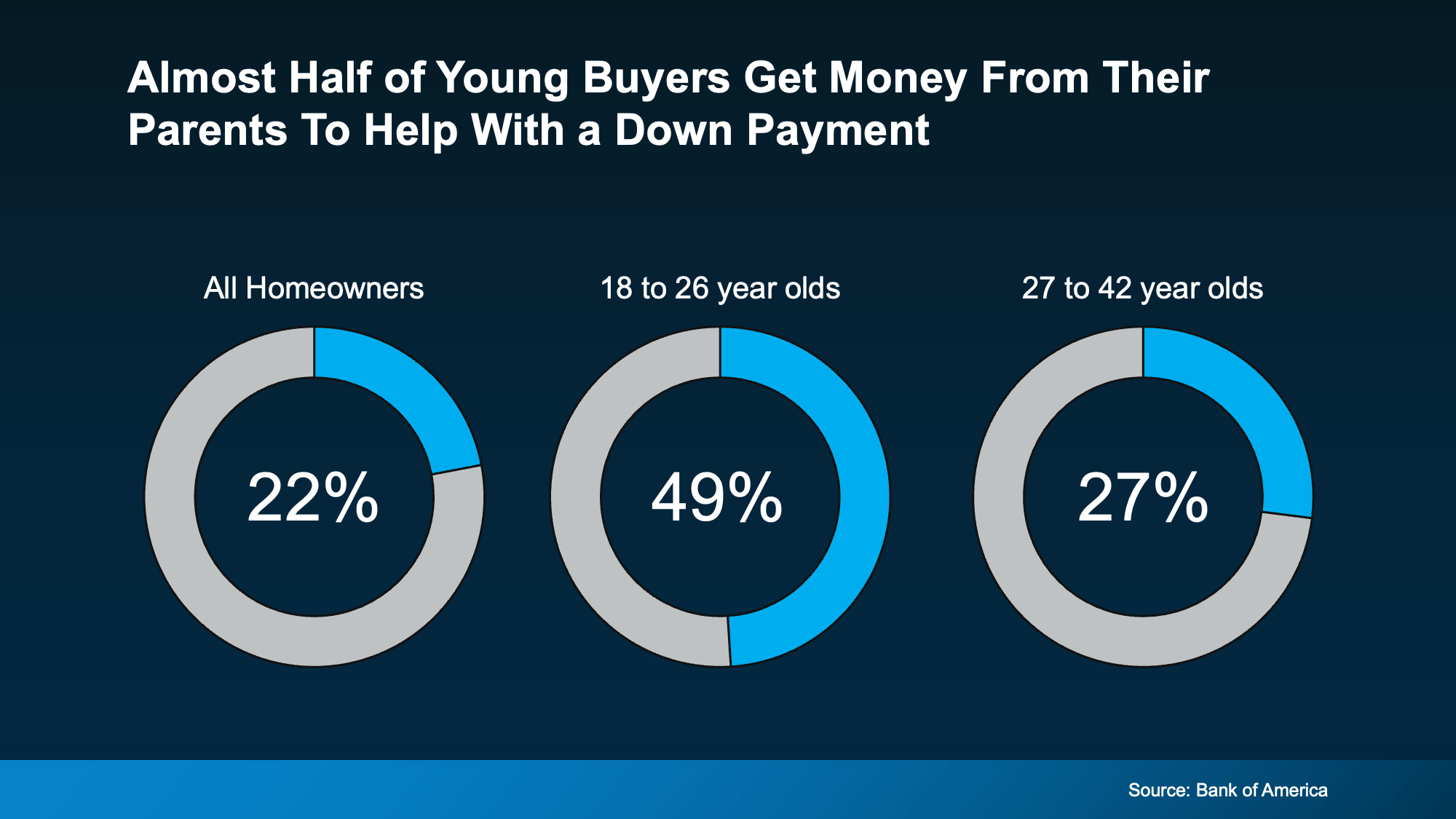

According to Bank of America, 49% of homebuyers aged 18–26 received financial help from their parents to cover part (or all) of their down payment. That’s nearly half of Gen Z buyers leaning on family support to make their homeownership dreams come true.

While the stats don’t say exactly how many used home equity specifically, there’s a good chance many did—especially considering how much wealth today’s homeowners have accumulated.

How Can You Tap Into Your Equity?

Good question! There are a few common ways parents are using their equity to help their kids become homeowners:

1. Cash-Out Refinance

This means replacing your existing mortgage with a new, larger one—and taking the difference in cash. You can use that cash however you want, including helping your child with a down payment.

2. Home Equity Loan

Think of this like a second mortgage. You borrow a lump sum based on your equity, with a fixed interest rate and repayment schedule. It’s a great option if you want to help now but don’t want to touch your main mortgage.

3. Home Equity Line of Credit (HELOC)

This is more flexible. A HELOC works like a credit card tied to your equity, letting you borrow as needed. It’s perfect if you’re unsure how much you’ll need upfront.

Each of these options comes with pros and cons, so it’s smart to talk to a lender or financial advisor before making a move.

Think Long-Term: You’re Not Just Giving Money—You’re Building a Legacy

This isn’t just about writing a check or unlocking some cash. It’s about planting seeds that could grow for generations.

When you help your child buy a home, you’re giving them the chance to build equity, too. You’re setting them up with a stable foundation—something many young adults can’t achieve on their own right now.

And it’s not just financial. For many parents, there’s an emotional reward that can’t be measured. Imagine the look on your kid’s face when they finally say, “We got the house!”—and you know you played a part in making it happen.

That’s a memory that sticks. That’s legacy-building at its finest.

Can They Really Not Do It Without Help?

According to Compare the Market, 45% of Americans who received help from parents or grandparents admitted they wouldn’t have been able to buy a home without it. That’s nearly half of first-time buyers who say their dream home would’ve stayed a dream if not for family support.

So yes, your equity can be the difference between your child renting for another decade or finally owning a place they can call home.

What Are the Risks?

We’d be doing you a disservice if we didn’t mention the flip side.

Using your home equity means increasing your debt—or reducing your cushion of wealth. It could impact your retirement plans, monthly payments, or even your ability to get approved for future loans.

That’s why it’s crucial to:

-

Talk to a financial advisor

-

Review your current mortgage and loan terms

-

Understand the impact on your long-term goals

This isn’t a decision to take lightly. But for many families, the benefits far outweigh the risks—especially when done with careful planning.

Still On the Fence? Ask Yourself This

If you knew you could help your child buy a home today—giving them the stability and pride that comes with homeownership—would you do it?

If it was easier than you thought—just a matter of tapping into the equity you’ve already built—would you at least explore it?

Sometimes, the opportunity to change someone’s life doesn’t come with fireworks or fanfare. Sometimes, it’s sitting quietly in your home value, just waiting to be put to good use.

Final Thoughts: Turn Bricks Into Blessings

Your home is more than just walls and a roof. It’s a wealth-builder, a legacy, and possibly the stepping stone your children need to start their own journey.

So if you’re sitting on six figures in home equity, why not see how it could help your child unlock their own front door?

Reach out to your lender. Talk to a trusted financial advisor. And most importantly—have the conversation with your kids.

You might be surprised just how powerful your support can be.

Recent Posts

GET MORE INFORMATION