Is $80 Really Worth Delaying Your Homeownership? The Truth Buyers Need to Hear in 2025

Buying a home has always felt like one of those big life moments—exciting, terrifying, and overwhelming all at once. But in today’s market? It feels even trickier. A lot of buyers are stuck in what I call “rate paralysis.” They’re watching mortgage rates hover in the low 6% range and thinking, “I’ll jump in once rates hit the 5s.”

Sounds logical, right? Who wouldn’t want a lower rate?

But here’s the twist: that magical 5.99% number might not save you nearly as much as you think. In fact, the real savings you’re waiting for… could be smaller than one dinner out.

Let’s break it down, without the jargon, without the fear tactics, and without the fluff.

Understanding Today’s Mortgage Rates: The Hidden Savings Buyers Don’t See

Let’s rewind a bit. Earlier this year—around May—mortgage rates peaked above 7%. That freaked a lot of buyers out. And understandably so.

But here’s what most people haven’t noticed:

Rates have already come down… and the savings are bigger than you think.

Rates today are sitting in the low 6% range. And while that shift might seem subtle, the impact on your monthly payment isn’t subtle at all.

How Much Has the Average Buyer Already Saved?

Let’s put real numbers behind the headlines.

According to Redfin data, the typical monthly payment on a $400,000 home is already down nearly $400 per month compared to the peak in May.

That’s $400 back in your pocket every single month—without waiting for rates to drop a single decimal more.

If you paused your home search earlier this year, you’ve already gained a serious affordability advantage compared to the market you stepped away from.

Yet a lot of people are still waiting… hoping… praying… for something “better.”

But is the “better” you’re waiting for actually meaningful?

Where Are Mortgage Rates Heading? (Spoiler: Not as Low as You Think)

Here’s the part most buyers don’t want to hear—but absolutely need to know:

Most industry experts believe rates will stay close to where they are now through 2026.

That means the chances of rates dropping dramatically are slim. Extremely slim.

Only one major forecaster is predicting that rates might dip into the upper 5% range next year. And even if that happens…

The savings would barely move the needle.

Let’s talk about the math, because numbers don’t lie.

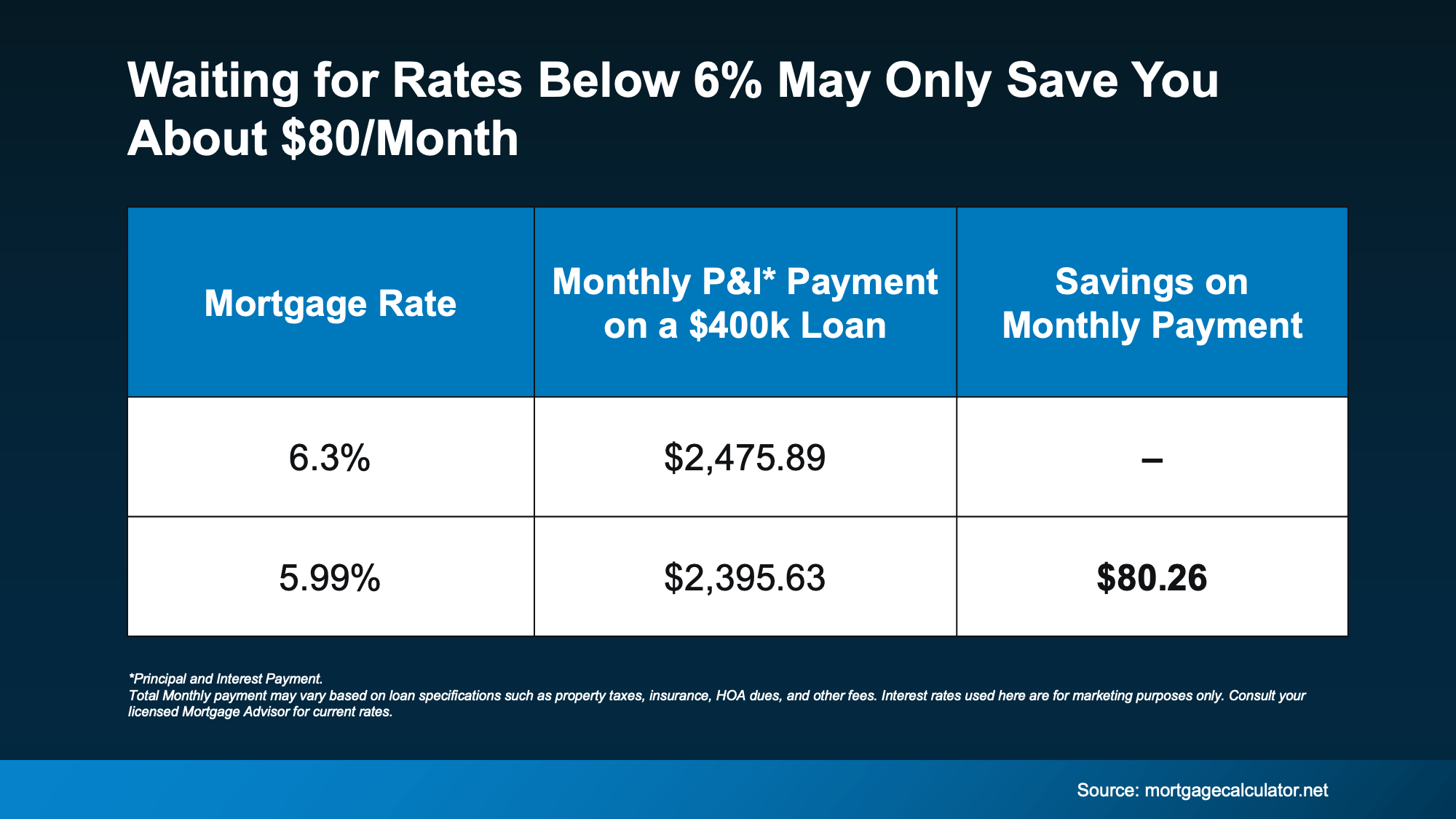

The Real Savings Behind a 5.99% Rate: Is It Worth Waiting For?

If rates dropped from today’s levels down to 5.99%, here’s what the difference looks like:

About $80 a month on an average-priced home.

That’s it.

Eighty dollars.

For most families, that’s the price of:

-

One dinner out

-

A few food delivery orders

-

A tank of gas

-

Two subscription services

So the big question becomes:

Are you really willing to delay your entire homeownership journey over $80 a month?

Especially when you’re already saving five times that amount compared to the peak earlier this year?

It’s like refusing a $400 monthly discount because you want an extra $80 on top of it later.

Sounds backward, doesn’t it?

But here’s the bigger risk—and it’s a big one.

Why Waiting for Lower Rates Could Cost You Way More Later

Even if rates drop below 6%, that tiny little $80 discount comes with a very big price tag:

Competition. LOTS of it.

Right now, buyers have a unique window. There are:

-

More homes on the market

-

Sellers willing to negotiate

-

Fewer buyers jumping in

-

Price reductions actually happening

But once rates hit the magical “5s,” you can kiss that quiet market goodbye.

What happens when rates drop? Buyers come rushing back.

The National Association of Realtors reports that if rates hit 6%, about 5.5 million more households suddenly become able to afford a median-priced home.

Even if just 10% of them decide to buy?

You’re looking at hundreds of thousands of new buyers entering the market again.

More buyers = more competition.

More competition = higher home prices.

Higher home prices = you lose the savings you waited for.

That extra $80 can disappear fast if prices jump even slightly.

Suddenly, waiting doesn’t feel so smart anymore, does it?

Timing the Market vs. Taking the Opportunity

Let’s be honest for a second.

Trying to time the real estate market perfectly is like trying to time the stock market or waiting for the “perfect moment” to start a workout routine. There’s always something that’ll make you hesitate.

But here’s the truth savvy buyers already understand:

You don’t win in real estate by waiting for perfection. You win by acting when opportunity is in your favor.

And right now?

-

Rates are lower than they’ve been in months

-

Competition is still manageable

-

Inventory is healthier

-

Sellers are open to concessions

-

Payments are already $400 cheaper than in the spring

This is what opportunity looks like.

But it won’t stay like this once rates fall even slightly lower.

So… Should You Wait for Rates Under 6%? Let’s Be Real.

Think about this for a moment:

If you found the perfect home today—one you loved, one that fit your budget—would you let $80 stand between you and homeownership?

Because that’s what waiting really means.

You’re gambling the bigger benefits of today’s market for a tiny possible savings that may never come… and even if it does, might cost you more in the long run.

The Bottom Line: The Best Time to Buy Isn’t When Rates Hit the 5s—It’s When the Numbers Work for YOU

You don’t have to wait for some magical mortgage rate to appear. You don’t need perfect timing. You need a strategy—and the willingness to take advantage of what the market is already giving you.

Rates are already better.

Payments are already lower.

Opportunities are already here.

The question now is simple:

Will you let $80 delay your entire path to owning a home?

If you’re serious about buying, the smartest move is to run your numbers now—not later. Because when the market shifts, it shifts fast.

Let’s take a look at your budget, your timeline, and your goals so you can see exactly what you’re working with in today’s market—before the window closes.

Just tell me when you're ready, and we’ll break it all down together.

Recent Posts

GET MORE INFORMATION