The Ultimate VA Home Loan Guide: How Veterans Can Buy a Home with $0 Down

Why So Many Veterans Miss Out on This Game-Changing Benefit

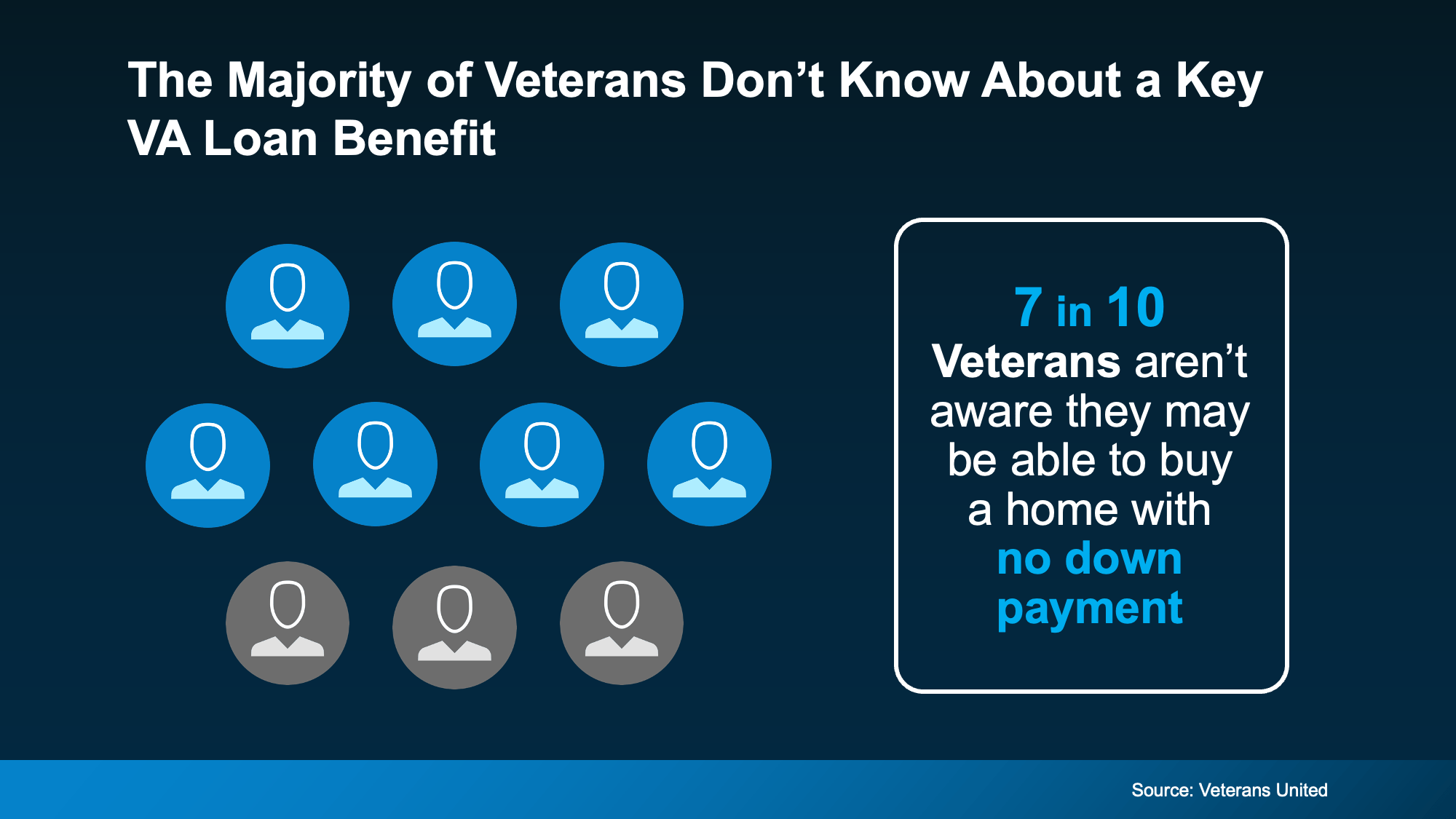

Did you know that nearly 7 out of 10 Veterans don’t realize they can buy a home without a down payment? Shocking, right? The truth is, the VA Home Loan Program—a benefit earned through service—remains one of the best-kept secrets in real estate.

If you’ve worn the uniform or you’re married to someone who has, you have access to one of the most powerful homebuying tools in America. This isn’t just another mortgage program—it’s a life-changing opportunity designed to help Veterans achieve stability, build wealth, and secure their dream home.

Let’s break it all down—how VA home loans work, their top benefits, and why you should take action now to make the most of them.

What Exactly Is a VA Home Loan?

A VA home loan is a special mortgage program backed by the U.S. Department of Veterans Affairs (VA). It’s not issued directly by the government but by private lenders, such as banks and credit unions, with the VA guaranteeing a portion of the loan.

That guarantee makes lenders more confident, which means better terms for you—like no down payment, no private mortgage insurance, and competitive interest rates.

In short, it’s a home loan designed for those who’ve served.

Why Veterans Love VA Loans: Top Benefits You Can’t Ignore

For nearly eight decades, VA home loans have helped millions of Veterans and active-duty service members turn the dream of homeownership into reality. Here’s what makes them so powerful:

1. $0 Down Payment — Yes, Really!

With traditional loans, you might need to save tens of thousands of dollars for a down payment. But with a VA loan, you can often skip that part completely. That means you can buy a home sooner instead of waiting years to save up.

2. Lower Upfront Costs

The VA actually limits the kinds of closing costs Veterans are required to pay. So, you’ll keep more money in your pocket at closing—something every buyer can appreciate.

3. No Private Mortgage Insurance (PMI)

Most buyers who put down less than 20% are stuck paying PMI each month. VA loan holders? Not you. That’s hundreds of dollars saved every single month.

4. Competitive Interest Rates

Because VA loans are backed by the government, lenders typically offer lower rates. Over the life of your mortgage, that could save you thousands of dollars.

5. Easier Qualification Standards

If your credit isn’t perfect, don’t worry. VA loans are known for being more flexible with credit requirements compared to conventional loans.

All in all, VA loans make it easier, faster, and more affordable for Veterans to achieve the American Dream of homeownership.

Can You Still Get a VA Loan During a Government Shutdown?

Here’s the million-dollar question that’s been worrying a lot of Veterans lately: “Are VA loans still available during a government shutdown?”

Good news — yes, they are.

According to Veterans United, while there might be some minor delays in processing, the VA loan system remains operational. Appraisals can still be ordered, Certificates of Eligibility can still be issued, and funding fees can still be processed.

So, while the news might sound dramatic, the truth is simple: your VA loan benefits are still active and available.

Sure, there may be a little waiting involved, but the opportunity to buy your home or refinance your mortgage is still there—just waiting for you to take it.

Why Having the Right Team Matters More Than You Think

Let’s be honest—navigating the homebuying process can be intimidating, especially if it’s your first time. But when it comes to using your VA loan benefits, having the right people on your side can make all the difference.

According to VA News, working with a military-friendly real estate agent and a VA-experienced lender is key. Here’s why:

-

They understand the VA process inside and out.

-

They can help you avoid unnecessary fees or delays.

-

They’ll make sure your offer is structured to meet VA guidelines.

Think of them as your homebuying team—your personal squad to get you from pre-approval to move-in day. When everyone knows the VA system, everything runs smoother and faster.

Step-by-Step: How to Apply for a VA Home Loan

Getting started might sound complicated, but it’s actually simpler than most people think. Here’s the basic roadmap:

Check Your Eligibility

You may qualify if you’re:

-

A Veteran, active-duty service member, or reservist

-

A surviving spouse of a Veteran who died in service or from a service-related cause

You can verify this by obtaining your Certificate of Eligibility (COE), which confirms your right to the VA home loan benefit.

Find a VA-Approved Lender

Not all lenders are created equal. Work with one that’s VA-approved and experienced in handling VA loans—they’ll guide you through every step.

Get Pre-Approved

Pre-approval helps you understand how much you can afford and shows sellers you’re serious.

Shop for Your Dream Home

Once you’re pre-approved, the fun part begins—house hunting! Your real estate agent (preferably VA-savvy) will help you find a home that meets both your needs and VA property standards.

Close the Deal

Your lender and agent will handle the details, from the appraisal to the final paperwork. Before you know it, you’ll have the keys in your hand and a home you can truly call your own.

How VA Loans Build Long-Term Wealth for Veterans

Buying a home isn’t just about having a roof over your head—it’s about building financial stability.

With a VA loan, you’re not just saving on upfront costs. You’re also building equity every time you make a mortgage payment. Over the years, that equity can turn into a valuable financial resource—something you can tap into for education, emergencies, or even retirement.

And let’s not forget: homeownership gives you freedom and security that renting simply can’t match.

Common Myths About VA Loans (Debunked!)

Let’s clear up a few misconceptions that stop too many Veterans from applying:

Myth 1: “VA loans take forever to close.”

Reality: With the right lender, VA loans close almost as fast as conventional ones.

Myth 2: “You can only use your VA loan benefit once.”

Reality: You can use it multiple times throughout your life—as long as you meet eligibility and entitlement requirements.

Myth 3: “VA loans are only for first-time homebuyers.”

Reality: Nope. Whether it’s your first or fifth home, you can use your VA benefits again.

Bottom Line: Don’t Leave Your VA Benefits on the Table

You’ve earned your VA home loan benefits through service and sacrifice—so don’t let them go unused.

With no down payment, no PMI, and lower monthly costs, the VA home loan is hands down one of the best deals in the housing market today.

So, if you’re a Veteran or an active-duty service member, take the next step. Talk to a VA-approved lender and explore your options.

Your dream home—and the financial stability that comes with it—might be closer than you think.

Ready to take action?

Start today by connecting with a trusted VA lender and see how your service can open the door to homeownership.

Recent Posts

GET MORE INFORMATION