Unlocking the Secret VA Home Loan Benefit Most Veterans Miss

Did You Know You Could Buy a Home with Zero Down as a Veteran?

You read that right. If you're a U.S. military Veteran, you could potentially become a homeowner without a single dollar in down payment—and most Vets don't even realize it. That’s like finding a golden ticket under your seat... and never looking.

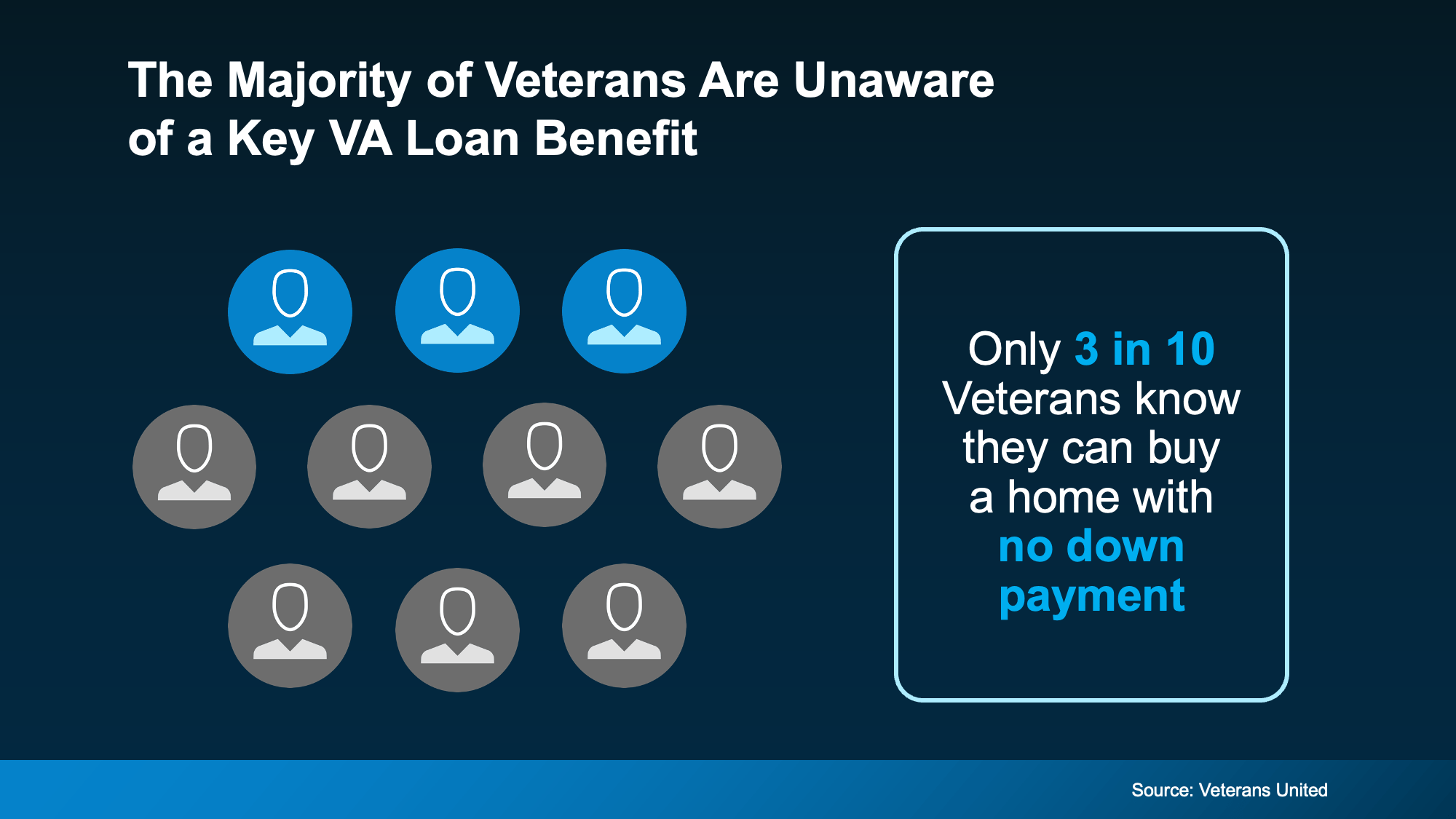

Despite this powerful benefit being around for more than 80 years, nearly 7 out of 10 Veterans have no idea they’re eligible to buy a home with $0 down through the VA loan program. Let’s unpack what that means—and why you shouldn’t leave this opportunity on the table.

What’s the VA Home Loan Program, Anyway?

In a nutshell, VA home loans are mortgages backed by the U.S. Department of Veterans Affairs. They were created after World War II as a way to help service members transition back to civilian life. Think of them as a "thank you" from the government for your service—only this one could be worth hundreds of thousands of dollars in homeownership potential.

These loans are only available to Veterans, active-duty service members, certain members of the National Guard and Reserves, and eligible surviving spouses. But here's the kicker: even among those who qualify, most have no clue what they're missing out on.

The $0 Down Payment: The VA Loan’s Best-Kept Secret

Imagine walking into your dream home and not needing to hand over a massive chunk of cash upfront. That’s exactly what the VA loan allows you to do.

According to a recent report from Veterans United, only 30% of Veterans know they can purchase a home with no money down. That leaves a whopping 70% who could be throwing away years renting or scraping together a traditional down payment—often unnecessarily.

Why this matters:

On a $300,000 home, a conventional loan might require a $60,000 down payment (20%). That’s a life-changing amount of money. But with a VA loan? That $60K stays in your pocket.

More Than Just $0 Down—VA Loans Pack Serious Perks

The no down payment is just the start. VA loans are loaded with benefits designed to make homeownership easier, cheaper, and more accessible.

Here’s what you get:

✅ No Private Mortgage Insurance (PMI)

Most lenders require PMI when your down payment is under 20%. It’s basically a fee to protect them—not you. With a VA loan, PMI is gone—forever. That could save you hundreds each month, which adds up to thousands over the years.

✅ Competitive Interest Rates

VA loans often offer lower-than-average fixed interest rates, making your monthly payment lower from day one. Over the life of the loan, that’s a massive savings.

✅ Easier Credit Requirements

Worried about your credit score? Don’t be. VA loans come with more forgiving credit guidelines, giving you a better shot at qualifying even if your financial past isn’t perfect.

✅ Limited Closing Costs

Closing on a home can feel like death by a thousand fees. But VA loans limit the types of closing costs you can be charged, helping you avoid those sneaky add-ons and keep more of your money where it belongs—with you.

Why More Veterans Aren’t Using Their VA Loan Benefits

So if these perks are so amazing, why aren't more Veterans using them?

It boils down to awareness and misinformation. Many Vets assume you need perfect credit, a big down payment, or even that they’ve already “used up” their VA benefit (spoiler: you can use it more than once!).

Others may think it’s “too good to be true.” But here’s the truth: this benefit is real, and you earned it.

Don’t Go It Alone—Talk to the Pros

The best way to know what’s possible? Connect with a real estate team that specializes in working with Veterans. That means a VA-savvy lender and an agent who understands the unique ins and outs of the program.

These pros can walk you through:

-

Confirming your eligibility

-

Getting a Certificate of Eligibility (COE)

-

Understanding your loan limits

-

Breaking down costs and benefits

-

Finding the right home (and deal) for you

How to Check If You’re Eligible

Eligibility is often easier to prove than most Veterans think. If you meet just one of the criteria below, you may already qualify:

-

You served 90 consecutive days of active service during wartime

-

You served 181 days during peacetime

-

You have more than 6 years in the National Guard or Reserves

-

You’re the surviving spouse of a service member who died in the line of duty

Still unsure? A VA-approved lender can pull your Certificate of Eligibility (COE) and give you a straight answer in minutes.

The Bottom Line: Don’t Leave Money (or a Home) on the Table

VA home loans aren’t just helpful—they’re life-changing. Whether you're buying your first home, upgrading to fit a growing family, or looking to finally settle down for retirement, the VA loan could be your golden ticket.

You’ve served your country. Now let your country serve you—with a loan program that respects your service and protects your wallet.

Ready to Take the First Step?

Talk to a trusted VA lender today. It doesn’t cost a thing to check your eligibility, but it could cost you thousands if you don’t.

Because here’s the truth:

This isn’t just a loan. It’s a door—to freedom, stability, and the home you deserve.

Pro Tip: Even if you’ve used your VA loan benefit before, you might still be eligible again—yes, really! Ask a VA lender about entitlement restoration.

Recent Posts

GET MORE INFORMATION