What A Fed Rate Cut Really Means For Mortgage Rates In 2025

The Federal Reserve is back in the headlines, and everyone from Wall Street analysts to everyday homebuyers is watching closely. The big question? If the Fed cuts interest rates, does that automatically mean mortgage rates will fall too?

It’s not quite that simple. Sure, Fed rate cuts influence borrowing costs across the economy, but mortgage rates dance to a rhythm of their own. Let’s break it all down in plain English so you know exactly what to expect in the months ahead.

The Fed Doesn’t Directly Control Mortgage Rates

Here’s the first thing to understand: the Federal Reserve does not set mortgage rates. The Fed sets the Federal Funds Rate, which is the short-term rate banks charge each other for overnight lending. Think of it as the baseline cost of money in the financial system.

When the Fed raises or lowers this rate, it ripples through the economy—affecting credit cards, auto loans, business loans, and yes, eventually mortgages. But mortgage rates are more closely tied to long-term bond yields, particularly the 10-year Treasury note, because lenders use those yields to price long-term lending risk.

So while the Fed isn’t sitting in a back room deciding your mortgage rate, its decisions shape the direction the housing market takes.

Why The Market Predicts Fed Moves Before They Happen

Here’s where things get interesting: financial markets don’t just wait around for the Fed’s official announcement. They anticipate it.

Investors constantly make bets on what the Fed will do next, and mortgage rates adjust before the Fed actually pulls the trigger. In fact, you could say the mortgage market is like that friend who blurts out the ending of a movie—you know what’s coming long before the big reveal.

For example, after weaker-than-expected jobs reports earlier this year, investors became convinced the Fed would start cutting rates. What happened? Mortgage rates dipped, even before the Fed met in September.

This means that if the Fed cuts its rate by the expected 25 basis points (0.25%), much of that move may already be “priced in.” Don’t expect a huge overnight drop in mortgage rates—because the market has already factored it in.

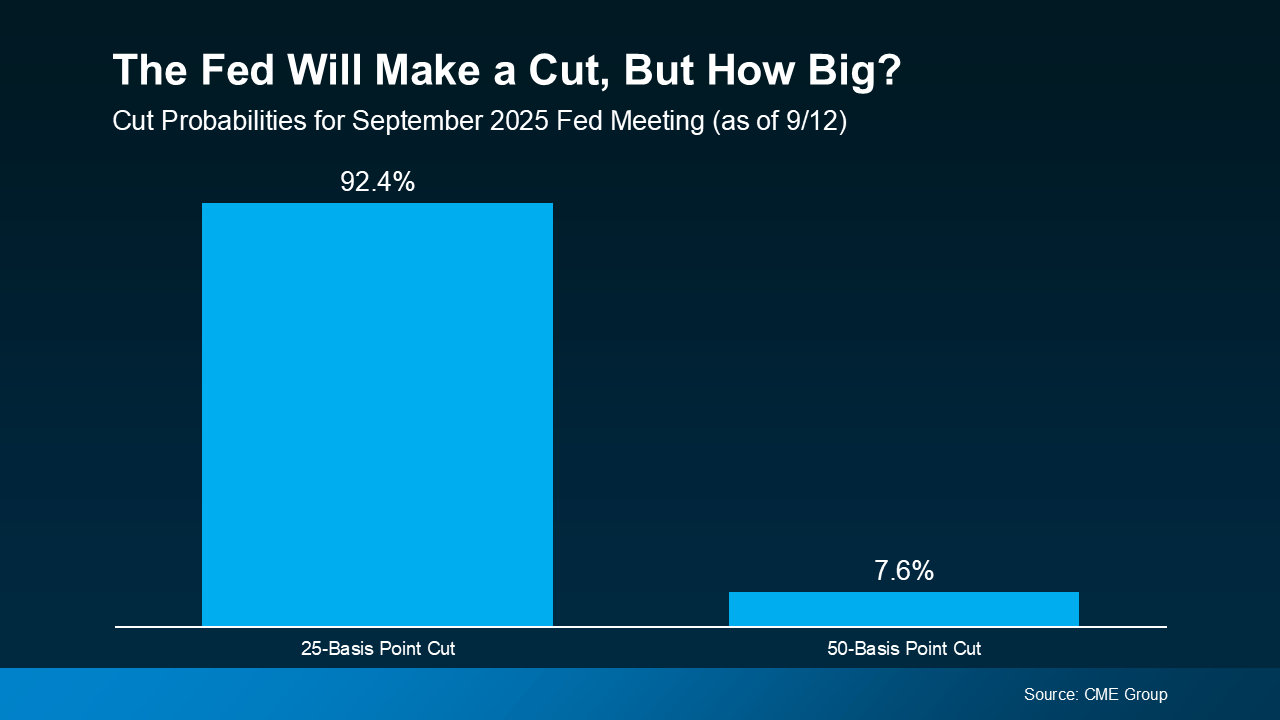

Small Cut vs. Big Cut: What’s The Difference?

So, what if the Fed surprises us?

-

A 25-basis point cut (0.25%) – This is the most likely outcome, and it’s already baked into current mortgage rates. Don’t expect dramatic changes.

-

A 50-basis point cut (0.50%) – This is less likely, but if it happens, you could see mortgage rates come down a bit more noticeably since the market hasn’t fully priced it in.

Think of it like ordering food at a restaurant. If you already know the chef’s specials, you’re not surprised when your plate arrives. But if the chef sends out a dish that’s not on the menu? That’s when things get exciting—and in this case, possibly more affordable for homebuyers.

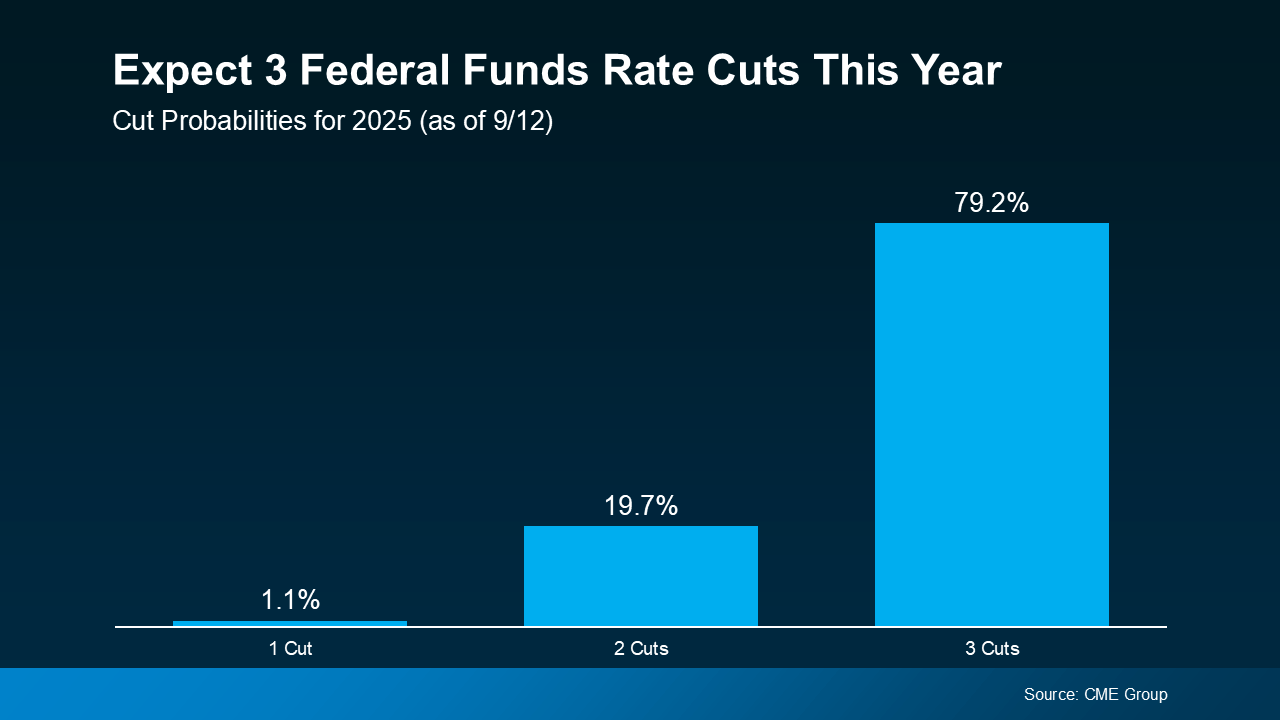

Could Multiple Fed Cuts Push Mortgage Rates Lower?

Here’s the bigger picture: one cut won’t transform the housing market overnight. But a cycle of cuts just might.

Economists believe the Fed could cut rates multiple times before the end of 2025 if the economy continues to cool. That could provide steady downward pressure on mortgage rates, making housing slightly more affordable for buyers who have been sidelined by sky-high borrowing costs.

Sam Williamson, Senior Economist at First American, explains it well:

“For mortgage rates, investor confidence in a forthcoming rate-cutting cycle could help push borrowing costs lower in the back half of 2025, offering some relief to housing affordability and potentially helping to boost buyer demand and overall market activity.”

In other words, it’s not just what the Fed does—it’s what the markets believe the Fed will do. If confidence builds that more cuts are coming, mortgage rates could trend lower even before the Fed takes additional action.

The Wild Card: Inflation

Of course, there’s always a catch. The Fed is laser-focused on inflation. If inflation cools steadily, the Fed will have more freedom to cut rates. But if inflation surprises to the upside—say, gas prices spike or consumer prices stay sticky—then the Fed may pause cuts or even reverse course.

That uncertainty means mortgage rates could remain bumpy in the short term. One unexpected inflation report could push rates higher again, at least temporarily.

What This Means If You’re A Homebuyer

Now, let’s bring this down to earth. What does all this mean if you’re thinking about buying a home or refinancing in the near future?

-

Don’t wait for a miracle drop. Mortgage rates are unlikely to plummet overnight. Even if the Fed cuts rates, expect gradual, not dramatic, declines.

-

Shop around. Lenders don’t all move in lockstep. The same borrower could see noticeably different offers from different lenders.

-

Look beyond the rate. Closing costs, points, and loan terms all affect your bottom line. Don’t fixate on the headline number.

-

Time is on your side (maybe). If you can wait until late 2025 or 2026, you might benefit from further cuts. But if you need a home now, small differences in rates may not outweigh the benefits of buying sooner.

Remember: even a modest dip in mortgage rates can translate into thousands of dollars in savings over the life of a loan. So while you won’t see rates cut in half overnight, the trend matters.

Historical Perspective: Fed Cuts vs. Mortgage Rates

To get some perspective, let’s rewind. Historically, mortgage rates don’t move one-for-one with Fed actions. For example:

-

In 2020, when the Fed slashed rates to near zero during the pandemic, mortgage rates fell too—but not instantly. It took months for the full effect to trickle down.

-

In the early 2000s, the Fed cut aggressively after the dot-com bubble burst, and mortgage rates eased, but again, the moves were gradual.

The lesson? Rate cuts are like turning a cruise ship. It takes time to see the full effect on mortgage rates and housing affordability.

What To Watch Next

If you’re tracking mortgage rates, keep your eye on these indicators:

-

Inflation reports (CPI and PCE). These are the Fed’s key gauges.

-

Jobs data. Weak jobs numbers increase the odds of future cuts.

-

Bond yields. The 10-year Treasury yield is the single best predictor of mortgage rate direction.

-

Fed meetings. Not just the decisions, but also the language in Fed statements, which often reveals future intentions.

The housing market is like a chess game—every move is about anticipating the next one.

Bottom Line

The Federal Reserve is likely to start a rate-cutting cycle in 2025, but that doesn’t mean mortgage rates will drop in perfect sync. Small cuts may already be priced in, while bigger or multiple cuts could gradually bring borrowing costs down.

If you’re in the market to buy or refinance, the key takeaway is this: don’t hold your breath for a sudden crash in rates. Instead, expect slow and steady changes, with opportunities to lock in better affordability if the Fed continues on a cutting path.

Mortgage rates may not fall off a cliff—but they could ease enough to make a meaningful difference in your budget later this year and into 2026.

So, should you wait or act now? That depends on your personal situation, but one thing’s clear: understanding the Fed’s role helps you make smarter decisions in today’s unpredictable housing market.

Recent Posts

GET MORE INFORMATION