What Everyone Gets Wrong About Rising New Home Inventory (And Why It’s Not 2008 All Over Again)

If you’ve been scrolling through real estate headlines lately, chances are you’ve seen some eye-catching claims: “New home inventory is at its highest since the housing crash!” Sounds alarming, right?

For anyone who remembers 2008, that kind of language triggers flashbacks of plummeting home values, foreclosures, and economic chaos. But here’s the truth: while the headlines might grab your attention, they don’t always give you the full story. And when you dig into the data, you’ll quickly realize today’s situation looks nothing like what we lived through back then.

Let’s break it down—without the hype and fear.

Why Today’s Housing Market Is Different From 2008

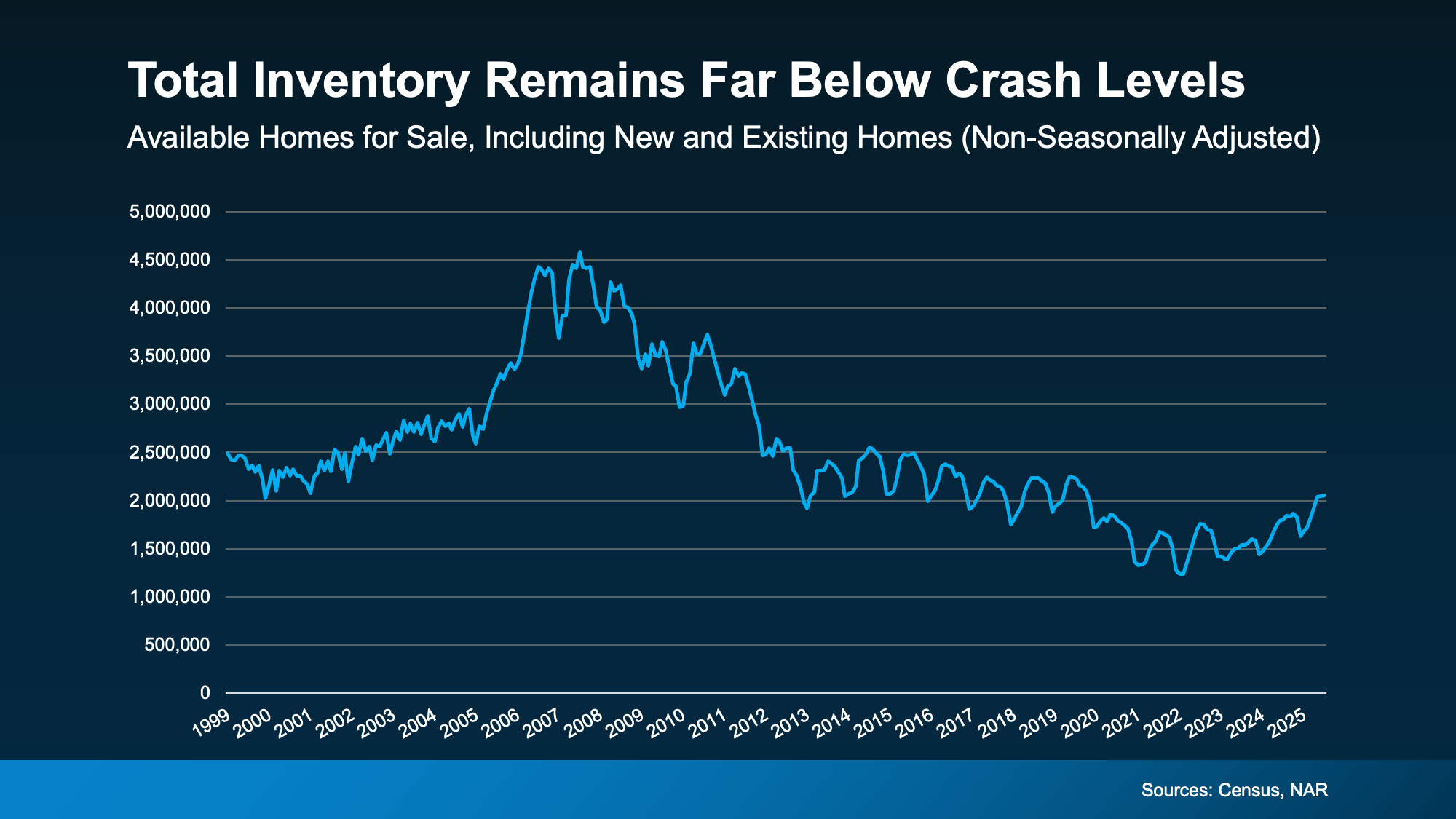

Yes, it’s true. The number of newly built homes available right now is the highest since the crash. But before you panic, let’s zoom out. New builds only represent one piece of the housing supply puzzle.

Back in 2008, the problem wasn’t just about new homes—it was the entire market. Builders had flooded the market with too many properties while lending practices made it way too easy for unqualified buyers to take on risky loans. The result? An enormous surplus of homes that nobody could afford, fueling the crash.

Today? That’s not the case at all.

When you combine new home inventory with existing home inventory (homes that already had previous owners), the bigger picture looks very different. Instead of a surplus, we’re still facing a housing shortage. In fact, the market is tighter than most people realize.

So, comparing “new home numbers today” to “2008’s total housing supply” is like comparing apples to oranges. It just doesn’t work.

Builders Have Been Playing Catch-Up for Over a Decade

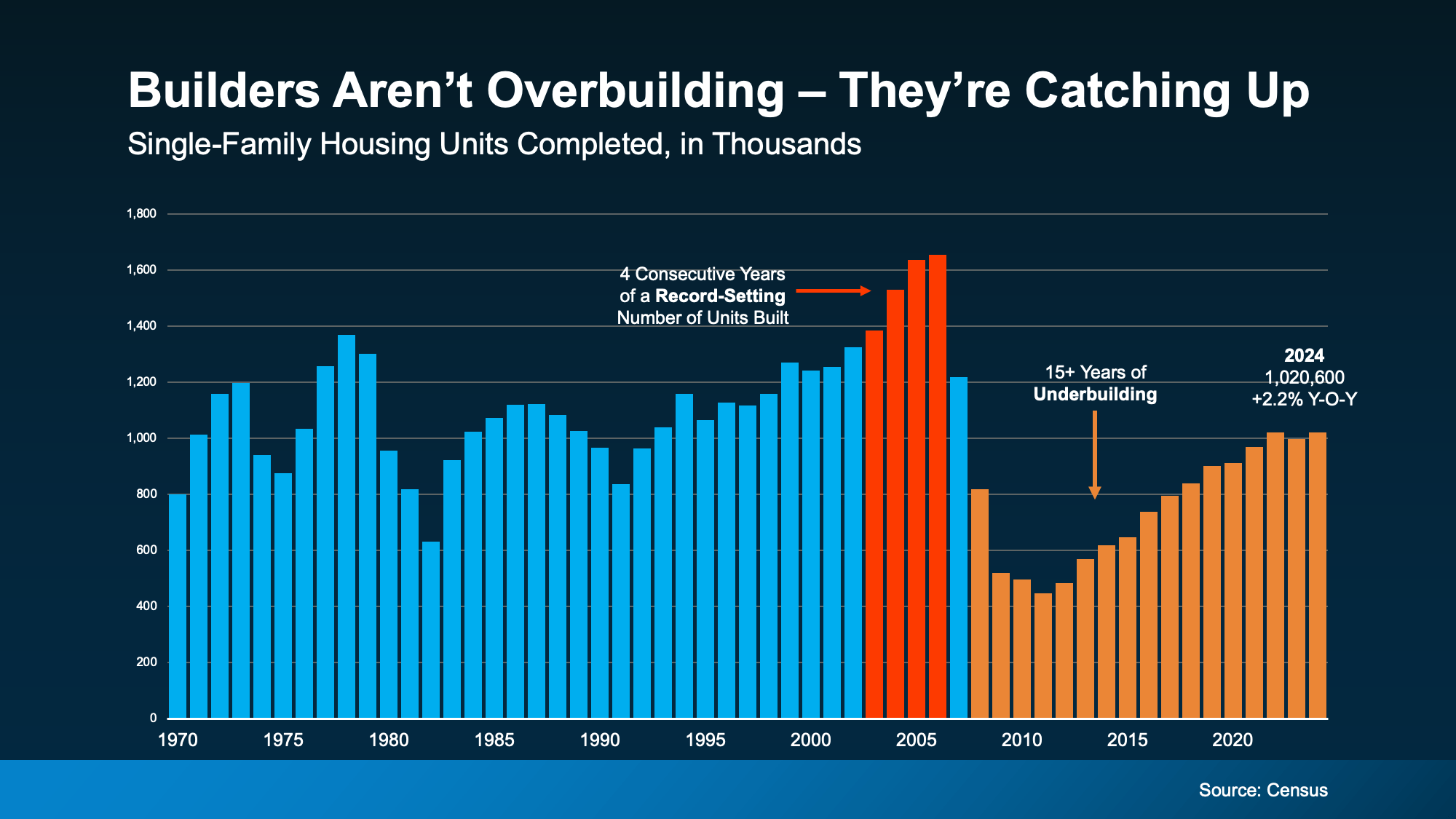

Here’s the part that most clickbait headlines leave out: builders have actually been underbuilding for nearly 15 years.

After the crash, homebuilders slammed on the brakes. They weren’t going to risk another oversupply situation, so construction slowed to a crawl. For more than a decade, fewer homes were built than needed to keep up with the demand from new households.

Think about that. Millions of families formed, younger generations entered the market, and population growth continued—yet new home construction lagged far behind. That underbuilding dug a deep hole we’re still trying to climb out of.

According to Realtor.com, it could take nearly 7.5 more years of steady building just to close the gap. Even with the recent uptick in construction, we’re nowhere near an oversupply. If anything, we’re still short.

What Rising Inventory Really Means for Buyers and Sellers

So, what does this increase in new home inventory actually mean for you? A few things:

-

Buyers have more options. If you’ve been struggling to find a home, you might finally see more choices hitting the market. That’s good news for anyone tired of bidding wars.

-

Sellers need to price wisely. More competition from new builds means existing homeowners can’t just slap a high price on a property and expect offers to roll in. Pricing strategy is key.

-

The market is balancing—not crashing. More homes available means less pressure, fewer wild price jumps, and a healthier market overall. That’s very different from the freefall of 2008.

Think of it like this: if the housing market were a crowded restaurant, 2008 was when they put out way too many tables, but nobody showed up to eat. Today, the restaurant has a waiting list of hungry customers—and builders are finally starting to add more tables to meet demand.

The Local Picture Still Matters

It’s important to remember that real estate is hyper-local. National trends give us the big picture, but your city or neighborhood could be very different.

Some markets are seeing more homes pop up, giving buyers relief. Others are still red-hot with limited inventory. So, while nationally we’re not in 2008 territory, your local market dynamics might feel tighter or looser depending on where you are.

That’s why it’s always smart to connect with a real estate professional who understands the local scene and can break down what the numbers mean for your situation.

Bottom Line: Rising New Home Inventory Is Not a Sign of a Crash

Don’t let the scary headlines fool you. More new homes on the market doesn’t equal another 2008. The difference is crystal clear: back then we had a massive surplus fueled by reckless building and lending. Today, we’re still playing catch-up from years of underbuilding.

The rise in inventory is actually a step toward a healthier, more balanced housing market. It means more opportunities for buyers, more competition for sellers, and a chance for the industry to inch closer to meeting demand.

So next time you see a headline comparing today to 2008, remember: the data tells a very different story.

And if you’re curious about what this all means for your local market, it might be time to have a conversation with someone who knows your area inside and out.

Recent Posts

GET MORE INFORMATION