Why Clinging to a 3% Mortgage Might Cost You More Than You Think

So, you’ve got that golden 3% mortgage rate—and yeah, that’s a dream deal in today’s market. It's the kind of rate that feels too good to let go. Why would anyone in their right mind trade that for something higher? Fair question. But let’s dig a little deeper, because sticking with that low rate might be costing you more than you realize.

Here’s the truth: people don’t move because of mortgage rates. They move because life happens. Family grows, needs shift, jobs change, or sometimes, you just need more space (or a lot less). So instead of asking, “Why would I move with a 3% rate?” maybe it’s time to ask, “What happens if I don’t?”

Let’s dive into why holding onto that low rate might actually backfire in the long run—and what the numbers are really saying about your next move.

Life Doesn’t Wait for Mortgage Rates

Picture your life five years from now. Go ahead, close your eyes for a second and really imagine it.

- Will you still be in the same job?

- Will your family be the same size?

- Are your kids moving out—or maybe moving in?

- Are you headed toward retirement?

- Is your current space feeling cramped or too empty?

If the answer to any of those is yes—or even maybe—it’s time to think beyond just your interest rate. Because the reality is, your life and lifestyle are way more important than a single number on a piece of paper.

Sure, 3% is sweet. But if you’re sacrificing comfort, convenience, or a better future for it… is it really worth it?

Waiting Could Mean Paying a Whole Lot More

Let’s say you’re not in a rush. Maybe you’re thinking, “I’ll wait it out. Prices will dip. Rates might come down again. I’ve got time.”

But here’s the thing: time isn’t always your friend when it comes to real estate.

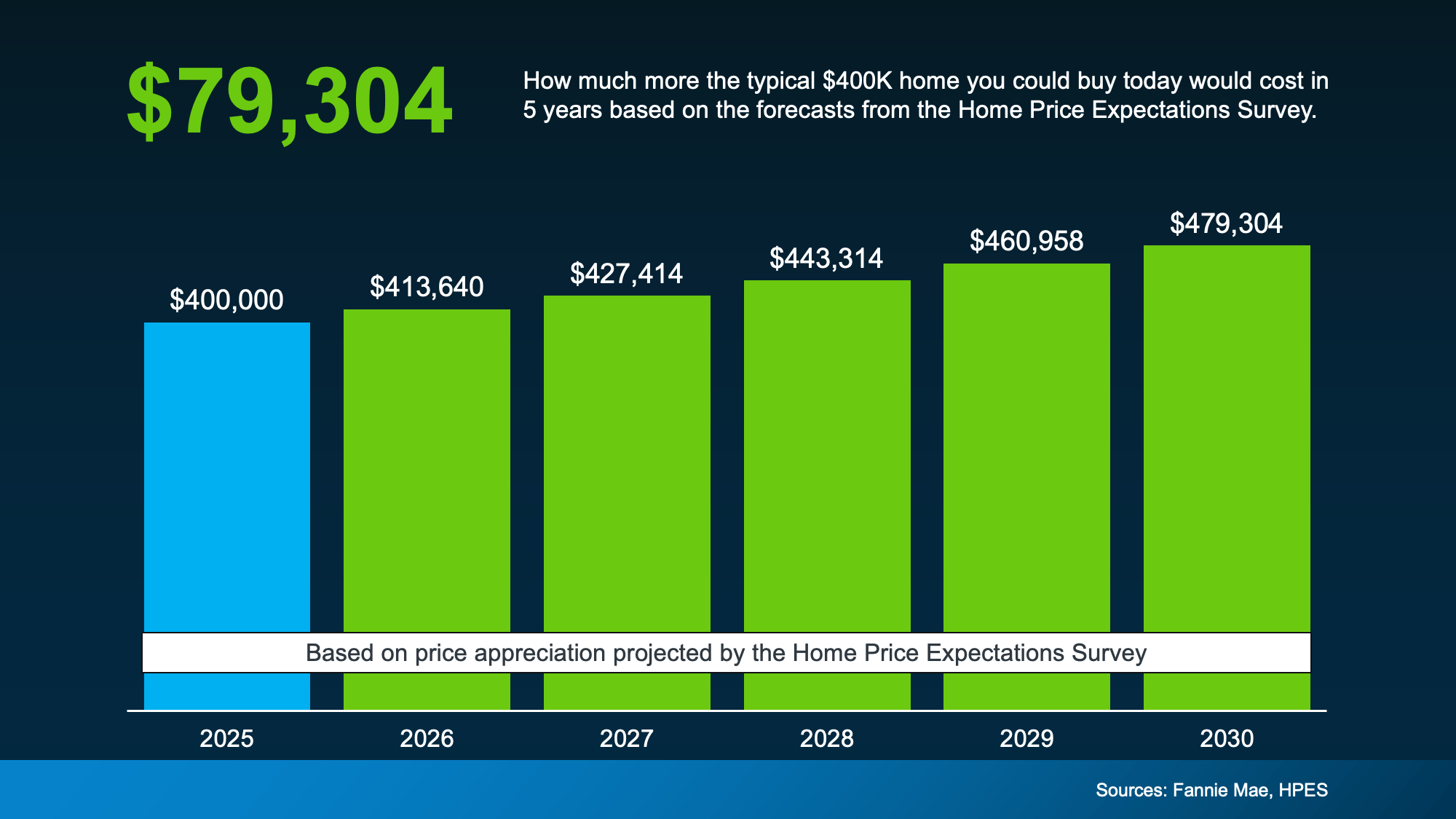

According to quarterly forecasts from Fannie Mae and over 100 housing market pros, home prices are expected to rise steadily through at least 2029. We’re not talking about massive jumps every year—but small increases add up, fast.

Let’s Do the Math:

Imagine your dream home is priced at $400,000 today.

If you wait five years, and prices rise just a modest 4% per year (which is what many experts are forecasting), that same house could cost you around $480,000 by then.

That's an $80,000 difference—for the same home.

And that doesn’t even factor in potential bidding wars, limited inventory, or inflation.

“But Interest Rates Might Drop Again... Right?”

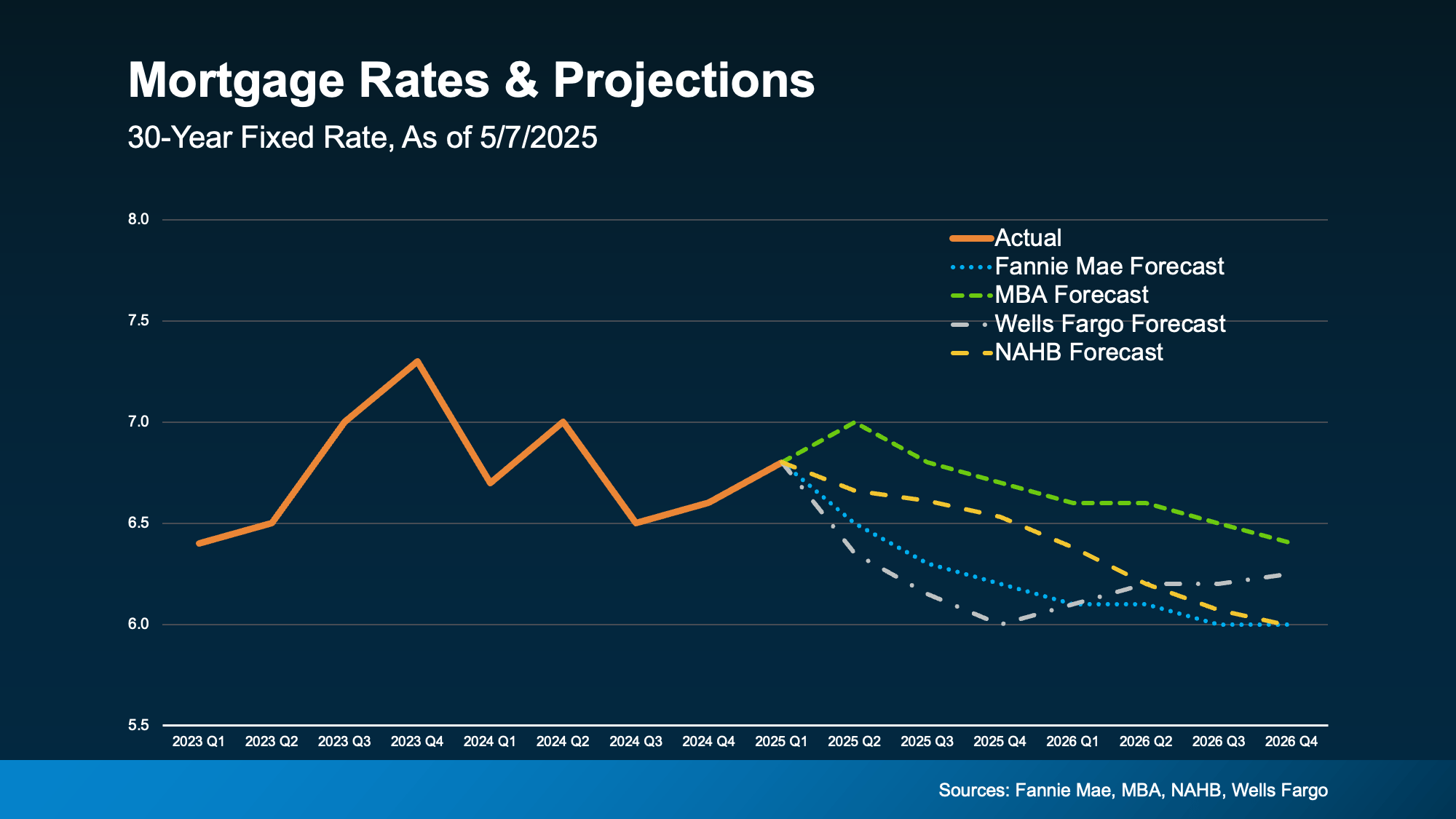

Yes, there’s chatter about interest rates eventually dipping. But here’s what the experts are not saying: that we’ll see those ultra-low 3% rates again anytime soon.

The Federal Reserve has hinted at some softening, but most forecasts suggest that rates will hover in the mid-to-high 5% range for the foreseeable future. So if you’re holding out for another 3% miracle, you might be waiting a long, long time.

And even if rates drop a bit, will it be enough to offset the higher home price you’ll pay later?

Spoiler alert: probably not.

The Real Question Isn’t Why Move?—It’s When?

Instead of asking, “Why would I leave this great mortgage rate?” start asking, “When is the best time for me to move based on my life, my goals, and the market?”

Think of it like this:

-

Low mortgage rate: Great in isolation.

-

Right house, right location, right time: Even better.

Delaying a move might feel like you’re saving money, but in many cases, it’s actually costing you more—both in dollars and in lost opportunities.

Planning Ahead = Peace of Mind

Here’s what you can do right now:

- Review your 5-year plan. Be honest with yourself. What changes are coming? Are you planning for growth, downsizing, or something totally new?

- Talk to a trusted real estate advisor. A great agent can run the numbers, show you market trends, and help you figure out if now—or soon—makes financial sense for you.

- Know your options. Maybe you rent your current place out. Maybe you buy now and refinance later. Maybe you explore new financing solutions. There are options—but they only work if you plan ahead.

Bottom Line: Don’t Let a Low Rate Hold You Back

A 3% mortgage rate is amazing—but it shouldn’t be the ball and chain that keeps you stuck.

If your life is changing (or you know it will), take a hard look at the numbers and your goals. Because waiting might cost you more than giving up that rate ever would.

Want to see the math based on your specific budget or dream home price point? Let’s chat. The best decisions are the ones that are both emotional and logical. You deserve both.

Let’s Talk Strategy – Not Just Rates

Planning a move in the next year or two? Wondering how today’s prices compare to what they’ll be tomorrow? I’ve got the tools to break it all down for you. Let’s crunch the numbers, talk through your goals, and map out a game plan that puts you in control—whether you move now, next year, or later.

After all, your mortgage rate is just a number. Your future? That’s priceless.

Recent Posts

GET MORE INFORMATION