Why Today’s Mortgage Debt Isn’t a Sign of a Housing Market Crash

As mortgage debt reaches new heights, many people wonder: is the housing market on the brink of a crash? With memories of the 2008 foreclosure crisis still fresh in many minds, it’s understandable to feel concerned when mortgage debt rises. But before you panic, there’s some important context to consider. While mortgage debt has hit record levels, the current market is in a much healthier state than it was during the housing crash. In fact, today’s homeowners are sitting on more equity and have fewer risks than they did in 2008. So, let’s explore why today’s mortgage debt isn’t a sign of an impending housing market disaster.

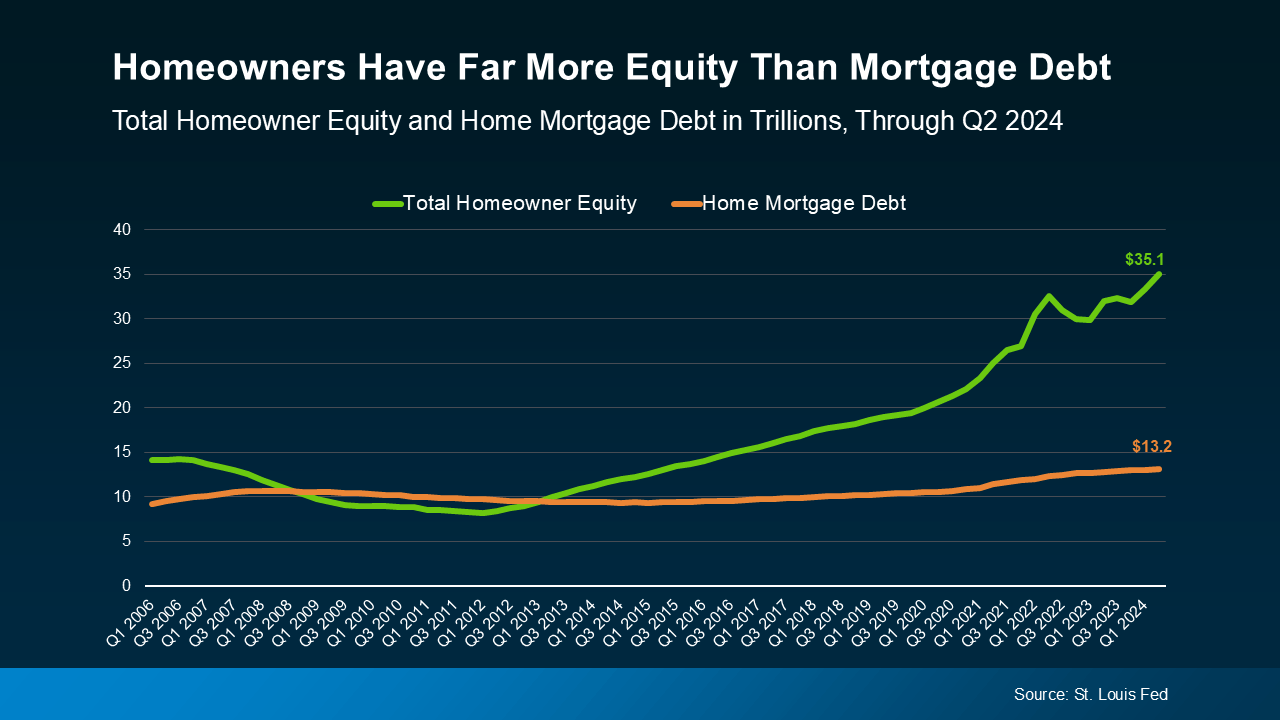

Mortgage Debt Is High, But Homeowners Have More Equity Than Ever

Unlike the housing crisis of 2008, when many homeowners owed more on their mortgages than their homes were worth (a situation known as being “underwater”), today's homeowners are in a much better financial position. Thanks to rising home prices over the past decade, the average homeowner today has significant equity in their property. In fact, total homeowner equity is nearly three times the amount of mortgage debt, according to data from the St. Louis Fed.

Why Equity Makes a Big Difference

Equity is the difference between the value of your home and what you owe on your mortgage. When homeowners have substantial equity, they’re less likely to face foreclosure. Why? Because if they can’t keep up with payments, they have the option to sell their property and potentially pocket some profits. Even if home prices were to drop slightly, most homeowners would still have enough equity to sell without risking foreclosure.

In contrast, during the 2008 housing crisis, many homeowners owed more than their homes were worth, leaving them with no viable options to avoid foreclosure. The situation was much riskier because home values had plummeted, and many people couldn’t sell without taking a loss.

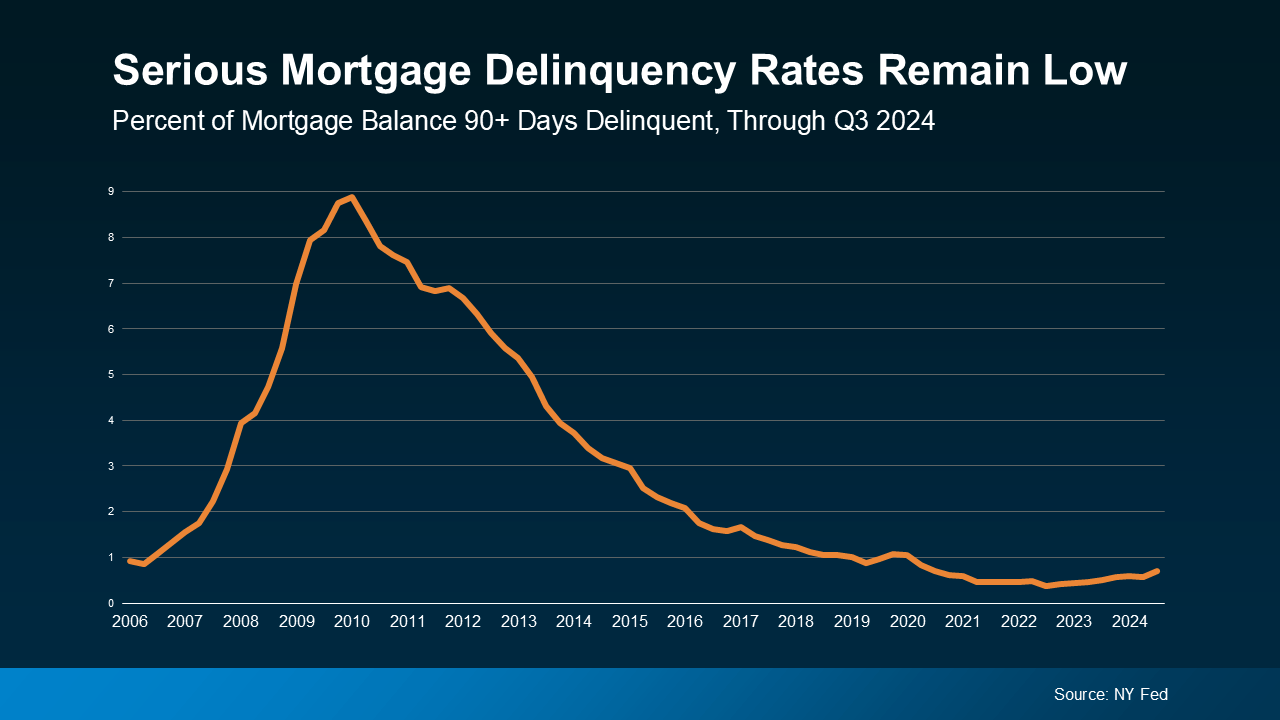

Why Delinquency Rates Are Lower Now

One major reason delinquency rates are so low is the ongoing efforts by mortgage servicers to help homeowners who are at risk of falling behind. After the 2008 crisis, many homeowners faced job loss, medical emergencies, or other financial setbacks without support from lenders. Today, however, servicers are much more proactive in offering solutions to keep homeowners in their homes.

Moreover, the low unemployment rate in the U.S. plays a significant role in reducing delinquency rates. More people have stable jobs, which makes it easier for them to manage their mortgage payments. As Archana Pradhan, Principal Economist at CoreLogic, notes, “Low unemployment numbers have helped reduce the overall delinquency rate.” In 2008, high unemployment contributed to a wave of foreclosures, but today’s job market is much stronger, providing a cushion against financial strain.

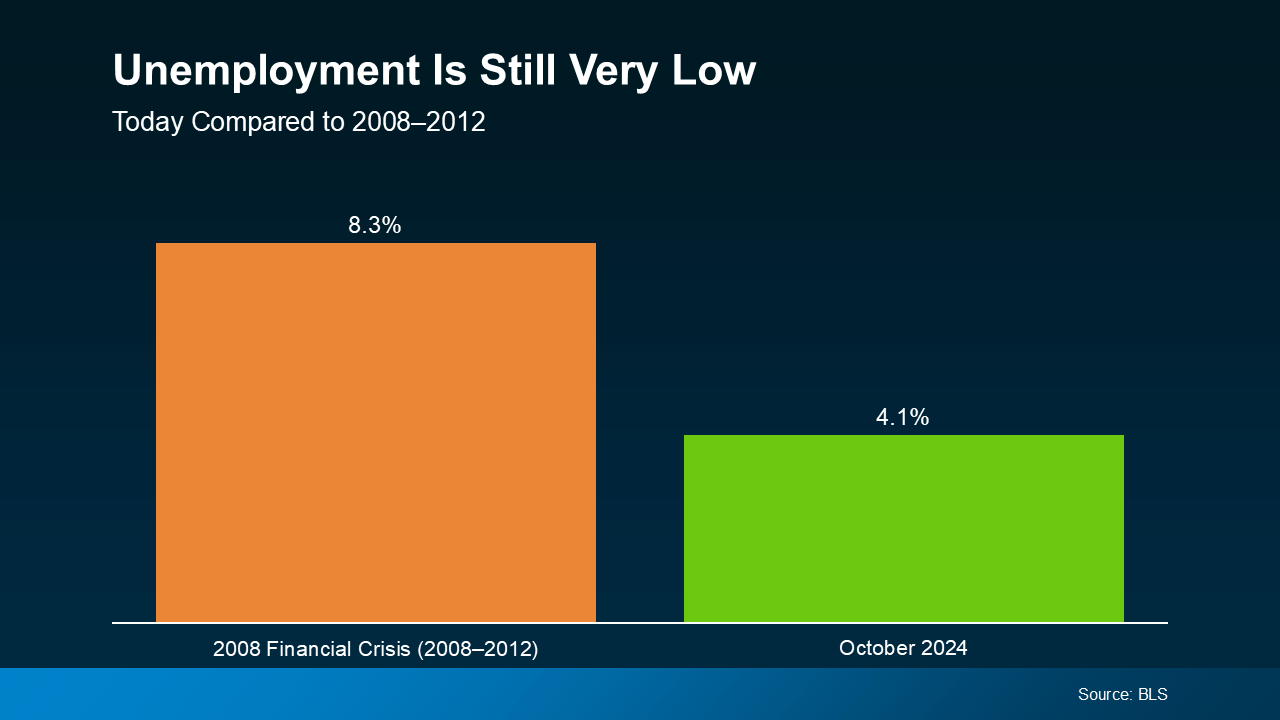

How Unemployment Rates Contribute to Market Stability

It’s not just about the economy’s current state; it’s also about how much things have changed since the last housing crisis. In 2008, the country was in the midst of a severe recession, and the unemployment rate was much higher. This put millions of people in a difficult position where they could no longer afford their mortgage payments, leading to a surge in foreclosures and distressed sales.

Today, however, the unemployment rate is low, with the economy growing steadily. According to the U.S. Bureau of Labor Statistics, unemployment is at its lowest levels in decades. This provides more job security for homeowners, which reduces the risk of mortgage delinquencies and foreclosures. Homeowners today are much more likely to be able to make their payments, even during difficult times.

Will There Be a Wave of Distressed Sales Like in 2008?

Many people are understandably worried about the possibility of another foreclosure crisis, but the key takeaway here is that today’s situation is vastly different. Bill McBride, a housing analyst at Calculated Risk, reassures us that “there will not be a huge wave of distressed sales as happened following the housing bubble.”

Thanks to strong homeowner equity, low unemployment, and more effective support systems, today’s housing market is far more resilient than it was in 2008. While mortgage debt is indeed at an all-time high, the risks are mitigated by these key factors that simply didn’t exist during the last housing bubble.

Why the Current Market Is in a Stronger Position Than 2008

The 2008 housing crisis was driven by several factors: inflated home prices, subprime lending, and an overall lack of financial stability. But today’s market is different. Today’s mortgage borrowers are generally more creditworthy, and lending standards are stricter. As a result, homeowners are in a much stronger position.

Moreover, unlike in 2008, many homeowners today are sitting on low-interest-rate mortgages, which means their monthly payments are more manageable. Even with mortgage debt rising, the financial burden isn’t as heavy as it was in the past. Plus, homeowners are less likely to default, given that most have built up substantial equity in their homes.

The Bottom Line: Mortgage Debt Isn't a Sign of a Housing Crash

While mortgage debt is at an all-time high, it’s not a sign of impending doom for the housing market. The market today is in a much stronger position than it was before the 2008 crash. Homeowners have more equity, delinquency rates are low, and the unemployment rate is stable—all of which help reduce the risk of widespread foreclosures and distressed sales.

So, if you’ve been worried about the state of the housing market, rest assured: today’s mortgage debt isn’t a red flag. In fact, it’s a sign that most homeowners are in a much better position to weather any economic storms.

If you have concerns or questions about today’s housing market, don’t hesitate to reach out to a real estate professional or mortgage expert. With the right information and guidance, you can make smart decisions about your homeownership journey.

Recent Posts

GET MORE INFORMATION