Why a Foreclosure Wave Isn't on the Horizon: Here's What You Need to Know

In recent times, it’s not uncommon to hear concerns about a potential surge in foreclosures. With inflation cooling but daily expenses still hitting hard, many are worried that financial strain might lead to a spike in mortgage defaults. But is this concern justified? Let's dive into why experts and data suggest a foreclosure crisis is not looming on the horizon.

The Current Mortgage Landscape: A Quick Overview

It's easy to feel uneasy about the economy, especially when everyday costs seem to rise unchecked. However, it’s important to understand that current economic indicators and lending practices are quite different from those during the last housing crisis. Here’s why the current climate is far from signaling a foreclosure wave:

Tighter Lending Standards Preventing Defaults

One of the major culprits of the foreclosure crisis back in 2008 was the lax lending standards. Lenders were extending mortgages to individuals who were not financially prepared to handle the payments, with little regard for their creditworthiness or ability to repay.

Today’s Lending Practices: Fortunately, we’re not in the same situation. Post-crisis, lending standards have become much stricter. Lenders now scrutinize credit scores, income levels, employment status, and debt-to-income ratios more carefully. This thorough vetting process ensures that borrowers are more capable of managing their mortgage commitments.

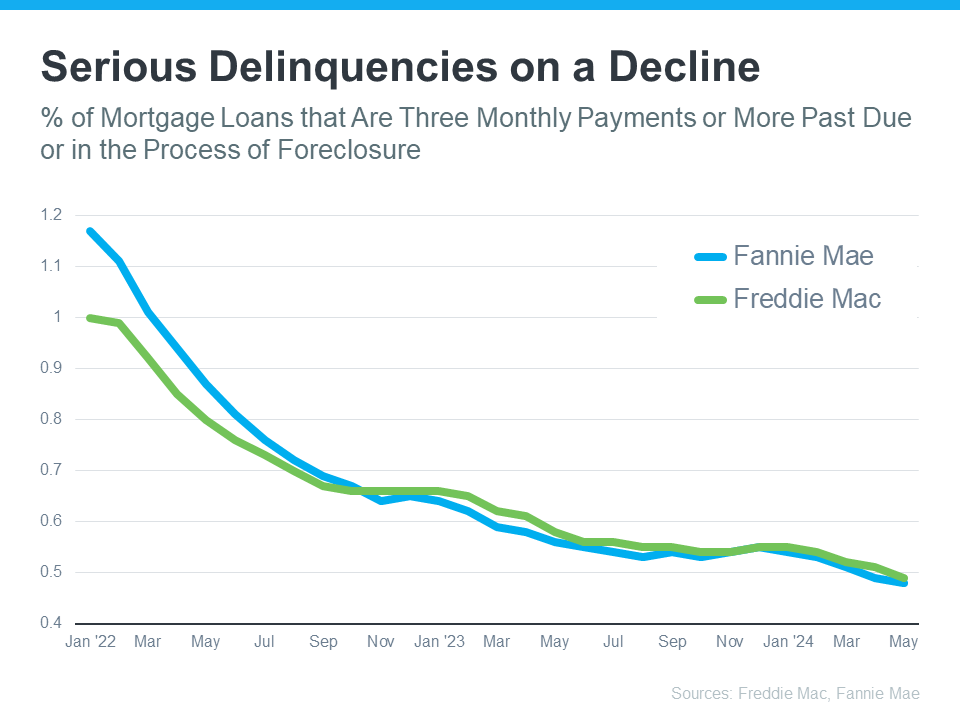

Declining Mortgage Delinquencies: A Positive Sign

According to data from Freddie Mac and Fannie Mae, the number of homeowners seriously behind on their mortgage payments has been on a steady decline. This decline is a direct result of:

- Stricter Lending Standards: More qualified buyers mean fewer defaults.

- Increased Home Equity: Many homeowners have built up significant equity in their homes, which they can leverage to avoid foreclosure if necessary.

The Equity Cushion: A Buffer Against Foreclosures

One of the key differences between now and the last housing crash is the substantial amount of home equity that many homeowners possess. Home equity acts as a safety net. If homeowners encounter financial difficulties, they can potentially sell their property or use the equity to negotiate their way out of trouble, thus avoiding foreclosure.

Expert Opinions: A Foreclosure Surge is Unlikely

Bill McBride, a well-respected analyst from Calculated Risk who accurately predicted the last foreclosure crisis, shares a reassuring perspective. According to McBride:

“We will NOT see a surge in foreclosures that would significantly impact house prices (as happened following the housing bubble) for two key reasons: 1) mortgage lending has been solid, and 2) most homeowners have substantial equity in their homes.”

Current Market Conditions: Why a Crisis Isn’t on the Horizon

To anticipate a significant rise in foreclosures, we would need to see a drastic increase in the number of homeowners unable to make their mortgage payments. Given the current economic data:

- Qualified Borrowers: Today’s mortgage borrowers are more financially stable.

- Equity and Repayment Options: Homeowners have more equity and options to manage their financial challenges.

Looking Ahead: A Stable Mortgage Market

While it's natural to be concerned about financial stability, the data and expert insights point to a stable mortgage market. The rigorous lending practices of today, combined with the substantial equity homeowners hold, make a foreclosure wave highly improbable.

Bottom Line

If you’re anxious about the possibility of a foreclosure crisis, rest assured that the current indicators don’t support such fears. The housing market is in a much healthier state compared to the pre-crisis years. With more qualified buyers and significant homeowner equity, the risk of a widespread foreclosure surge remains low.

Recent Posts

GET MORE INFORMATION