Home Insurance Costs Are Rising In 2026: What Smart Buyers Need To Plan For Now

Buying a home is exciting. It’s the keys, the photos, the “this is really happening” moment. But behind all that excitement is a stack of numbers that can make your head spin — and one of the most overlooked is homeowner’s insurance.

Think of home insurance like a seatbelt. You don’t buy it because you expect a crash. You buy it because when something does happen, the damage doesn’t ruin your life. The problem? That seatbelt is getting more expensive every year.

Let’s break down why home insurance costs are rising, what that means for buyers in 2026 and beyond, and how you can plan smartly so it doesn’t derail your homeownership dreams.

What Homeowner’s Insurance Really Covers (And Why You Can’t Skip It)

Before we talk about rising premiums, let’s get clear on what homeowner’s insurance actually does — because it’s more than just a box you check for your lender.

Protection For Repairs And Rebuilding

If your home is damaged by fire, storms, or other covered disasters, your policy helps pay for repairs. In worst-case scenarios, it can even cover a full rebuild. Without insurance, those costs land squarely on you — and rebuilding a home today can cost hundreds of thousands of dollars.

Coverage For Personal Belongings

Your furniture, electronics, clothing, appliances, and even valuables like jewelry are often protected. If they’re stolen or damaged, insurance can help replace them. Imagine losing everything in a fire and having to start from zero — that’s what this coverage prevents.

Liability Coverage For Accidents

If someone slips on your steps or gets hurt on your property, homeowner’s insurance can help cover medical bills or legal expenses. One accident shouldn’t put your financial future at risk.

Peace of mind like that is priceless — but lately, it’s also pricier than ever.

Why Home Insurance Premiums Are Rising So Fast

Home insurance costs aren’t going up randomly. There are some very real, very expensive forces at play.

Extreme Weather Is Becoming The New Normal

Severe storms, wildfires, floods, and hurricanes are happening more often — and they’re more destructive. More disasters mean more insurance claims, and insurers adjust premiums to keep up with payouts.

In simple terms: when insurers pay out more, everyone pays more.

Construction Costs Are Sky-High

Even minor repairs cost more today. Lumber, roofing materials, wiring, plumbing — everything is more expensive. Labor costs are higher too.

So when an insurance company has to repair or rebuild a home, the bill is much bigger than it was just a few years ago. Those costs get passed down to homeowners in the form of higher premiums.

Inflation Doesn’t Spare Insurance

Inflation affects insurance just like groceries and gas. Higher operating costs, higher claim payouts, and higher replacement values all feed into rising premiums.

The result? Insurance costs have climbed steadily year over year.

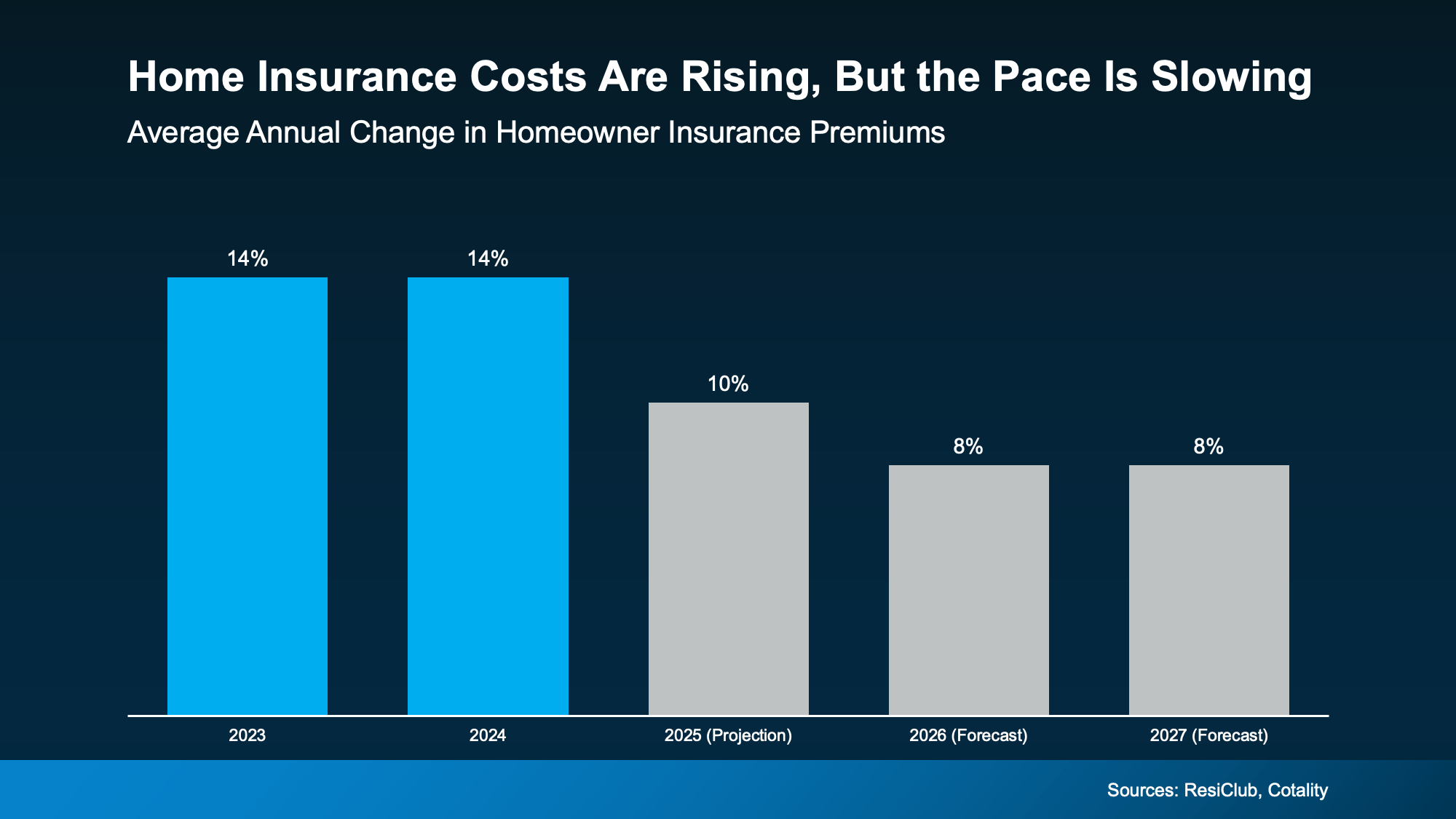

Is There Any Good News? Yes — The Pace Is Slowing

Here’s the silver lining: while insurance premiums are still rising, the speed of those increases is starting to cool.

Recent industry data shows:

-

In 2023 and 2024, premiums jumped around 14% per year

-

In 2025, increases slowed to about 10%

-

In 2026 and 2027, projections point to roughly 8% annual increases

That’s still an increase — but it’s no longer a runaway train. Think of it like inflation easing: prices aren’t dropping, but the pressure isn’t as intense.

Falling Mortgage Rates Can Help Offset Insurance Costs

Here’s where things balance out a bit.

While insurance costs are rising, mortgage rates have been trending downward. And that matters more than many buyers realize.

Even a small drop in your interest rate can significantly reduce your monthly mortgage payment — sometimes enough to offset higher insurance and taxes.

The key isn’t expecting one factor to cancel out another. It’s about layering the right decisions together:

-

Choosing the right loan program

-

Locking in a competitive rate

-

Planning for insurance realistically

When done correctly, homeownership is still very achievable — even in a higher-insurance environment.

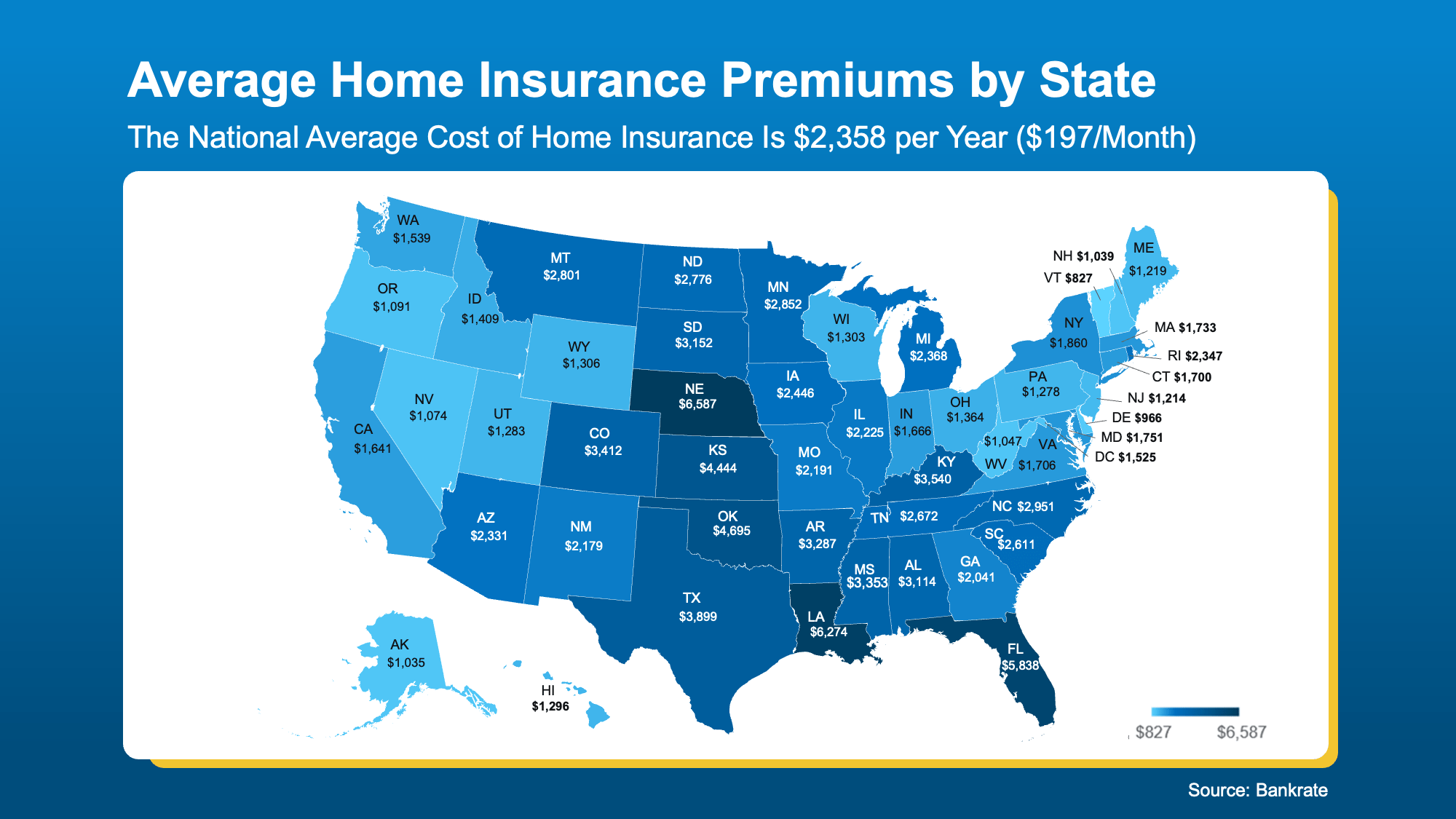

Home Insurance Costs Vary Widely By Location

Not all homes — or states — are created equal when it comes to insurance.

Why Location Matters So Much

Insurance premiums are heavily influenced by:

-

Local weather risks (hurricanes, floods, wildfires)

-

Crime rates

-

Building codes

-

Average home values

-

Claim history in the area

A home in a low-risk inland state may cost far less to insure than a coastal or disaster-prone area — even if the homes are similarly priced.

That’s why two buyers with the same budget can have very different monthly costs depending on where they buy.

When Do You Pay For Home Insurance?

For buyers, timing matters.

At Closing

Your first year of homeowner’s insurance is typically included in your closing costs. You’ll usually pay the premium upfront so coverage begins immediately.

After Closing

After that first year, insurance becomes a recurring expense — often paid monthly through your escrow account along with property taxes.

This is why it’s so important to factor insurance into your long-term budget, not just your upfront costs.

How Buyers Can Save On Home Insurance In 2026

You may not be able to control the market, but you can control how smartly you shop. Here are proven ways to lower your premium.

Shop Around (Seriously)

Insurance rates vary wildly between providers. Comparing quotes isn’t optional — it’s essential. One hour of shopping could save you hundreds per year.

Bundle Your Policies

Many insurers offer discounts if you bundle home and auto insurance. It’s one of the easiest ways to lower your rate without changing coverage.

Ask About Discounts

New homeowners often qualify for discounts they don’t know about — things like security systems, smoke detectors, or being claims-free. Ask directly.

Highlight Home Upgrades

A newer roof, storm-resistant windows, updated electrical systems — these can all reduce risk in the insurer’s eyes and lower your premium.

Improve Your Credit Score

In many states, your credit score impacts your insurance rate. Better credit often equals lower premiums. It’s not instant, but it’s powerful.

Why Cutting Coverage Is Usually A Bad Idea

When premiums rise, some buyers consider lowering coverage to save money. This can backfire fast.

Underinsuring your home means:

-

You may not get full replacement value after a loss

-

You could pay out-of-pocket for major repairs

-

One disaster could undo years of financial progress

Home insurance isn’t the place to gamble. It’s meant to protect your biggest investment — not barely cover it.

What This Means For First-Time And Repeat Buyers

If you’re buying your first home, rising insurance costs can feel intimidating. If you’re a repeat buyer, they may feel frustrating. Either way, the solution is the same: plan early.

Get insurance quotes while you’re still house-hunting. Ask lenders to estimate escrow payments accurately. Build insurance into your monthly comfort zone, not just your maximum approval amount.

Knowledge is leverage — and in this market, leverage matters.

Bottom Line: Plan Ahead, Stay Protected

Home insurance costs are rising, and they’re likely here to stay. But higher premiums don’t mean homeownership is out of reach.

When you:

-

Understand why costs are increasing

-

Budget realistically

-

Shop smartly for coverage

-

Take advantage of falling mortgage rates

You put yourself in control.

Homeowner’s insurance isn’t just another bill. It’s the shield protecting what’s likely the biggest investment of your life. And that’s one thing worth planning for — not skimping on.

Recent Posts

GET MORE INFORMATION