The Hidden Power of Home Equity: Why Repeat Buyers Have a Major Advantage in Today’s Housing Market

What if your next home didn’t come with a mortgage payment?

Sounds unrealistic, right? For many homeowners today, though, it’s not just a dream—it’s becoming a real possibility. Thanks to rising home values and years of equity growth, repeat buyers are stepping into the market with a financial advantage many first-time buyers simply don’t have.

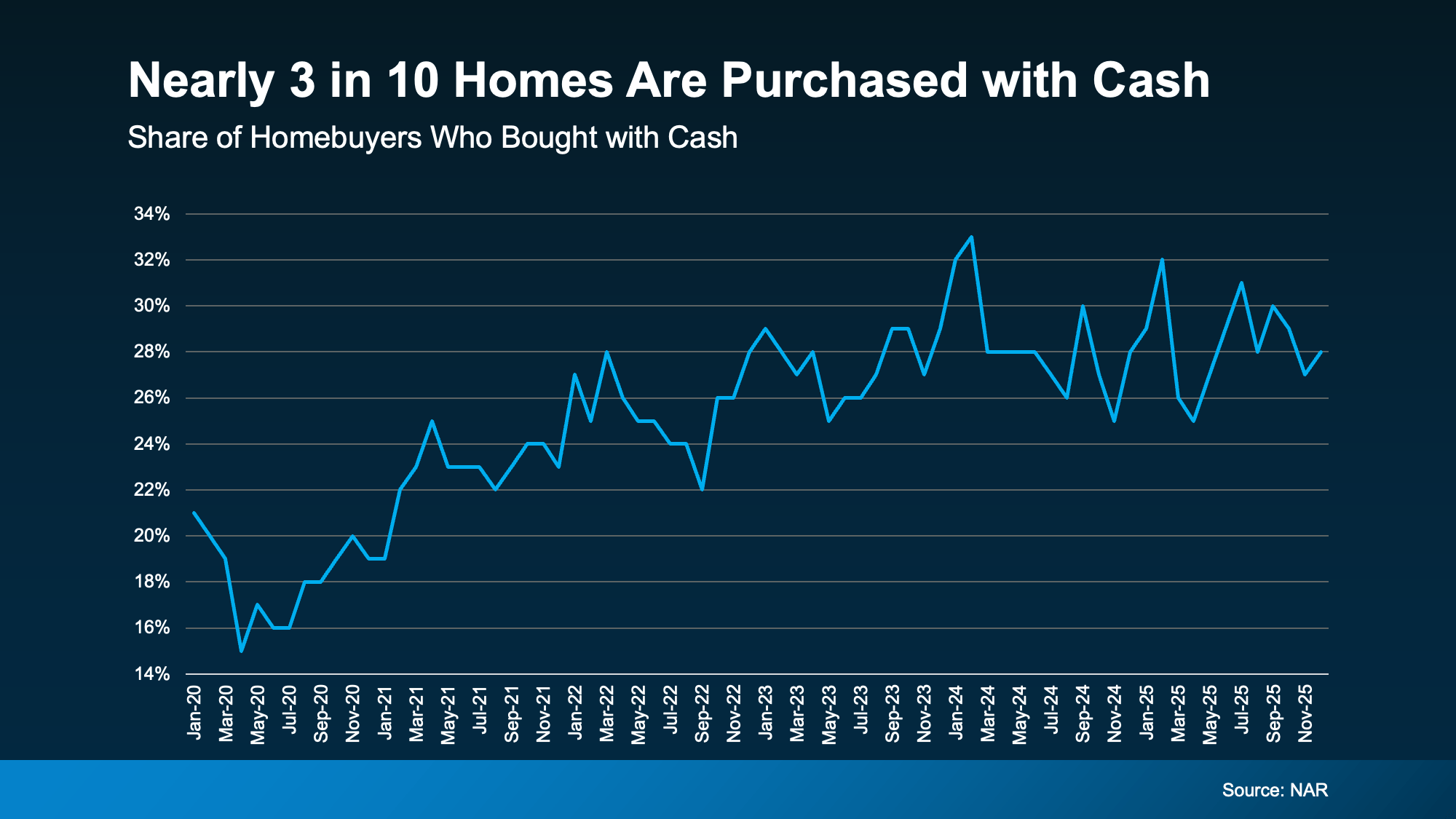

In fact, nearly three out of every ten homes purchased today are bought entirely in cash, according to data from the National Association of Realtors. That number is significantly higher than what we saw before the pandemic.

So what’s driving this shift?

The answer is home equity—and it’s quietly transforming the way many homeowners are buying their next property.

Let’s break down why repeat buyers have such a powerful edge right now and how equity can unlock opportunities that many homeowners don’t even realize they have.

How Rising Home Equity Is Changing the Homebuying Game

To understand why so many buyers are paying cash, we need to rewind a bit.

Between 2020 and 2021, two major things happened simultaneously:

-

Mortgage rates dropped to historic lows.

-

The number of homes available for sale reached record lows.

That combination created the perfect storm for rising home prices. With more buyers competing for fewer homes, property values climbed rapidly across the country.

If you owned a home during that time, chances are your property increased in value—possibly by a substantial amount. And that increase didn’t just look good on paper. It translated into real, usable equity.

Think of equity like a financial springboard. The longer you own your home and the more its value grows, the more leverage you gain when it's time to make your next move.

For many homeowners, that accumulated equity is now powerful enough to fund the purchase of another home—sometimes even without needing a mortgage.

Why Cash Offers Give Buyers a Powerful Edge

If you’re able to purchase a home with cash, you immediately gain advantages that financed buyers simply can’t match. In competitive housing markets, that difference can be the deciding factor between winning and losing a home.

Let’s look at the biggest benefits.

1. Cash Offers Are More Attractive to Sellers

From a seller’s perspective, certainty is everything.

A traditional home sale involving financing always carries a degree of risk. Mortgage approvals can fall through. Appraisals can come in lower than expected. Loan processing can hit unexpected delays.

Cash buyers eliminate those concerns entirely.

When a seller receives a cash offer, they know the deal is far less likely to collapse at the last minute. There’s no lender approval required, no financing contingency, and no waiting for underwriting.

Because of this, sellers often prioritize cash buyers—even if the offer isn’t the absolute highest price.

It’s a bit like choosing between two job offers: one promises a slightly higher salary but has uncertain terms, while the other guarantees stability and immediate results. Many sellers prefer the dependable option.

2. Faster Closing Times Make Deals More Appealing

Another major advantage of buying with cash is speed.

When a buyer relies on a mortgage, the process can take weeks—or sometimes longer. There are loan applications, credit checks, underwriting reviews, and lender approvals that must all happen before the transaction can close.

Cash purchases remove that entire layer.

Without financing involved, deals can close dramatically faster—sometimes in a matter of days instead of weeks.

That speed can be incredibly appealing to sellers who need to move quickly. Maybe they’ve already signed a contract on their next home. Maybe they’re relocating for work. Or perhaps they simply want a smooth, stress-free sale.

In situations like these, a buyer who can close quickly often becomes the obvious choice.

3. Owning Your Home Without a Mortgage

Let’s talk about one of the biggest benefits of all: financial freedom.

When you buy a home with cash, you own it outright from day one. That means no lender, no interest payments, and no monthly mortgage bill showing up in your mailbox.

Imagine the difference that could make in your monthly budget.

No mortgage payment means more room for the things that matter most—whether that’s saving for retirement, traveling, investing, or renovating your home exactly the way you want.

It also removes one of the biggest financial obligations most households carry. Without a mortgage hanging over your head, homeownership can feel far more flexible and secure.

Think of it like removing a massive weight from your financial backpack. Suddenly, every step forward feels lighter.

4. Cash Buyers Often Pay Less for Homes

Here’s something that surprises many homeowners: cash buyers frequently pay less for the same house.

Why?

Because sellers often value certainty and speed just as much as price.

A cash offer removes financing risks and simplifies the entire transaction. For some sellers, that reliability is worth accepting a slightly lower offer.

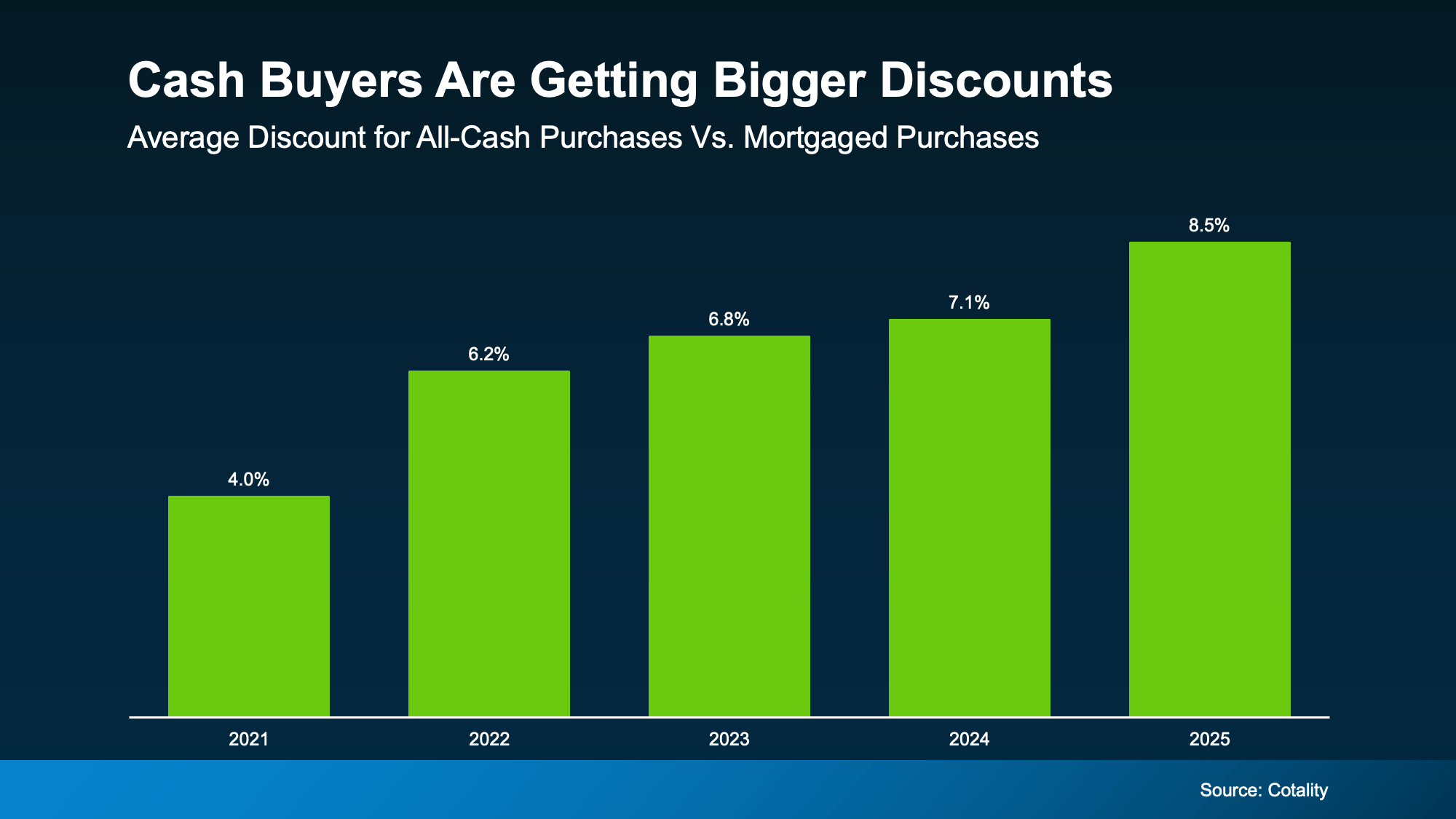

Studies have found that homes purchased with cash can sell for roughly 9% less than properties bought with traditional financing.

From a seller’s perspective, it’s a trade-off. Accepting a slightly lower offer may feel like the safer bet if it guarantees the deal will close without complications.

It’s similar to selling a car. You might receive two offers—one slightly higher but dependent on a bank loan, and another slightly lower but with immediate payment. Many sellers choose the immediate certainty.

Is Buying Your Next Home in Cash Realistic?

Of course, not every homeowner will be able to buy their next property entirely in cash—and that’s perfectly okay.

The bigger takeaway isn’t that everyone should aim for a cash purchase. It’s that the equity in your current home may give you more flexibility than you realize.

That equity can open several possible paths, including:

-

Downsizing to a smaller home and eliminating a mortgage entirely

-

Relocating while making a stronger, more competitive offer

-

Using equity as a substantial down payment to lower monthly payments

-

Leveraging equity to invest in additional real estate

In other words, the home you already own could be the key to unlocking your next move.

And many homeowners underestimate just how much buying power they’ve built over time.

The Strategic Advantage Repeat Buyers Have Over First-Time Buyers

First-time buyers often face the toughest obstacles in today’s housing market: saving for a down payment, qualifying for a mortgage, and competing with experienced buyers.

Repeat buyers, on the other hand, typically enter the market with built-in advantages.

They already have equity. They’ve benefited from appreciation. And they often have the option to use that wealth strategically.

It’s a bit like climbing a ladder. The first step is the hardest—but once you’re higher up, reaching the next rung becomes much easier.

Home equity effectively becomes the ladder that helps homeowners keep moving forward.

Why Understanding Your Home Equity Matters

Before assuming you’ll need another traditional mortgage, it’s worth asking a simple but powerful question:

How much equity do you actually have in your current home?

The answer could dramatically reshape what your next move looks like.

Many homeowners are surprised to discover they have far more financial flexibility than they expected. In some cases, the appreciation alone may provide enough leverage to make a major lifestyle change possible.

Understanding your equity isn’t just about numbers—it’s about understanding your options.

Bottom Line: Your Current Home Could Be the Key to Your Next One

Today’s housing market may feel challenging at times, but homeowners who’ve built significant equity are sitting on a hidden advantage.

That equity can transform how you buy your next home—making your offer stronger, your closing faster, and your financial future more flexible.

And for some buyers, it even opens the door to something many people dream about but rarely expect:

Owning their next home completely mortgage-free.

So before automatically assuming your next purchase requires another loan, take a moment to evaluate the equity you’ve built.

You might be sitting on more buying power than you ever imagined.

Recent Posts

GET MORE INFORMATION