THE VA HOME LOAN SECRET MOST VETERANS STILL DON’T KNOW

For many Veterans, the dream of owning a home feels farther away than ever. Rising home prices, higher interest rates, and the pressure of saving for a huge down payment can make buying a home seem impossible. In fact, nearly half of Veterans believe homeownership is currently out of reach. But here’s the surprising truth: many Veterans are far closer to buying a home than they realize.

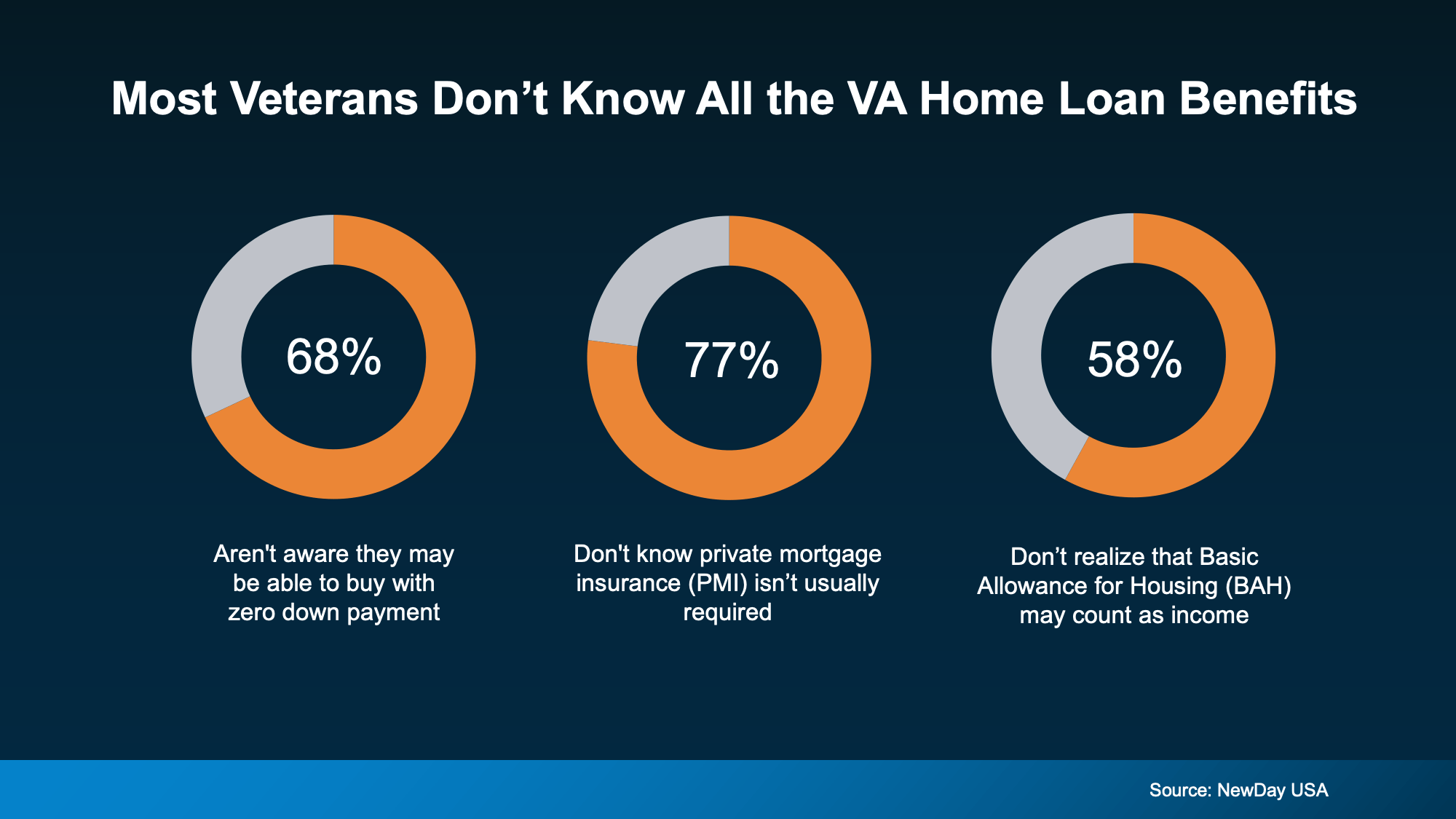

The reason? A large number of service members and Veterans still don’t fully understand how their VA home loan benefit actually works.

That’s a big deal because the VA loan program is one of the most powerful homebuying benefits available in the United States today. Yet misconceptions continue to stop qualified buyers from taking advantage of it. Some believe they need a massive down payment. Others assume the process is too difficult or expensive. And many don’t realize just how much money they could save over time.

If you’ve served in the military, are currently on active duty, or are part of a qualifying reserve unit, this benefit could open doors you thought were still years away. Let’s break down the biggest myths surrounding VA home loans and uncover what most Veterans still don’t know.

Why VA Home Loans Matter More Than Ever

Think of a VA loan like a bridge. While traditional loans may ask buyers to climb a steep financial mountain alone, the VA loan program helps carry part of the weight. Backed by the U.S. Department of Veterans Affairs, these loans are specifically designed to make homeownership more accessible for those who have served the country.

The program has existed for more than 80 years, helping millions of Veterans purchase homes with better terms and fewer financial barriers. Yet despite its long history, confusion about the benefit remains surprisingly common.

And honestly, that confusion can be expensive.

Recent Posts

GET MORE INFORMATION