Down Payments Are Smaller Than Ever Since 2021: Here's Why Buying a Home May Be More Affordable Than You Think

For many aspiring homeowners, saving for a down payment has always felt like climbing the tallest mountain on the homebuying journey. It's often the biggest hurdle standing between renters and homeownership. With housing affordability remaining a concern across many markets, it's understandable why so many people assume they need years of savings before they can purchase a home.

But what if that assumption isn't entirely true?

The housing market is shifting, and one of the biggest changes may surprise you. Down payments have dropped to their lowest levels since 2021, giving more buyers an opportunity to enter the market without needing as much cash upfront.

If you've been waiting on the sidelines because you thought your savings weren't enough, now may be the perfect time to take another look.

Why Are Down Payments Getting Smaller?

Several market trends are making it possible for today's buyers to purchase homes with less money upfront. While every buyer's situation is unique, these factors are helping reduce the amount many people need to save before buying.

1. A More Balanced Housing Market Means Less Pressure

Not long ago, buyers were competing fiercely for every available home. Multiple offers, bidding wars, and waived contingencies became the norm. In that environment, larger down payments often gave buyers an edge.

Today's market looks very different.

Inventory has improved in many areas, and buyers are no longer facing the same level of competition. With fewer bidding wars, sellers aren't always expecting massive down payments to accept an offer. That creates more flexibility for buyers and reduces the financial pressure many once felt.

Think of it like running a race where everyone was sprinting at full speed just a few years ago. Now, the pace has become much more manageable.

Cooling Home Prices Are Helping Buyers

Another important reason down payments are shrinking is that home prices have started to stabilize.

Since most down payments are calculated as a percentage of the home's purchase price, slower price growth naturally leads to smaller upfront costs.

In many local markets:

- Home prices have leveled off.

- Annual appreciation has slowed.

- Some regions have even experienced modest price reductions.

For buyers, that's welcome news. Even a slight decrease in purchase price can translate into thousands of dollars less needed for a down payment.

More Buyers Are Choosing Low Down Payment Loan Programs

One of the biggest misconceptions about buying a home is believing you need to put 20% down.

In reality, that's far from the truth.

Many buyers are taking advantage of mortgage programs specifically designed to lower the upfront financial burden.

Popular options include:

- FHA loans, which often require as little as 3.5% down for qualified buyers.

- VA loans, available to eligible veterans, active-duty military members, and certain surviving spouses, which can offer zero down payment financing.

- Other specialized mortgage programs that reduce upfront costs for qualified borrowers.

These financing options continue to grow in popularity because they make homeownership more accessible without requiring years of aggressive saving.

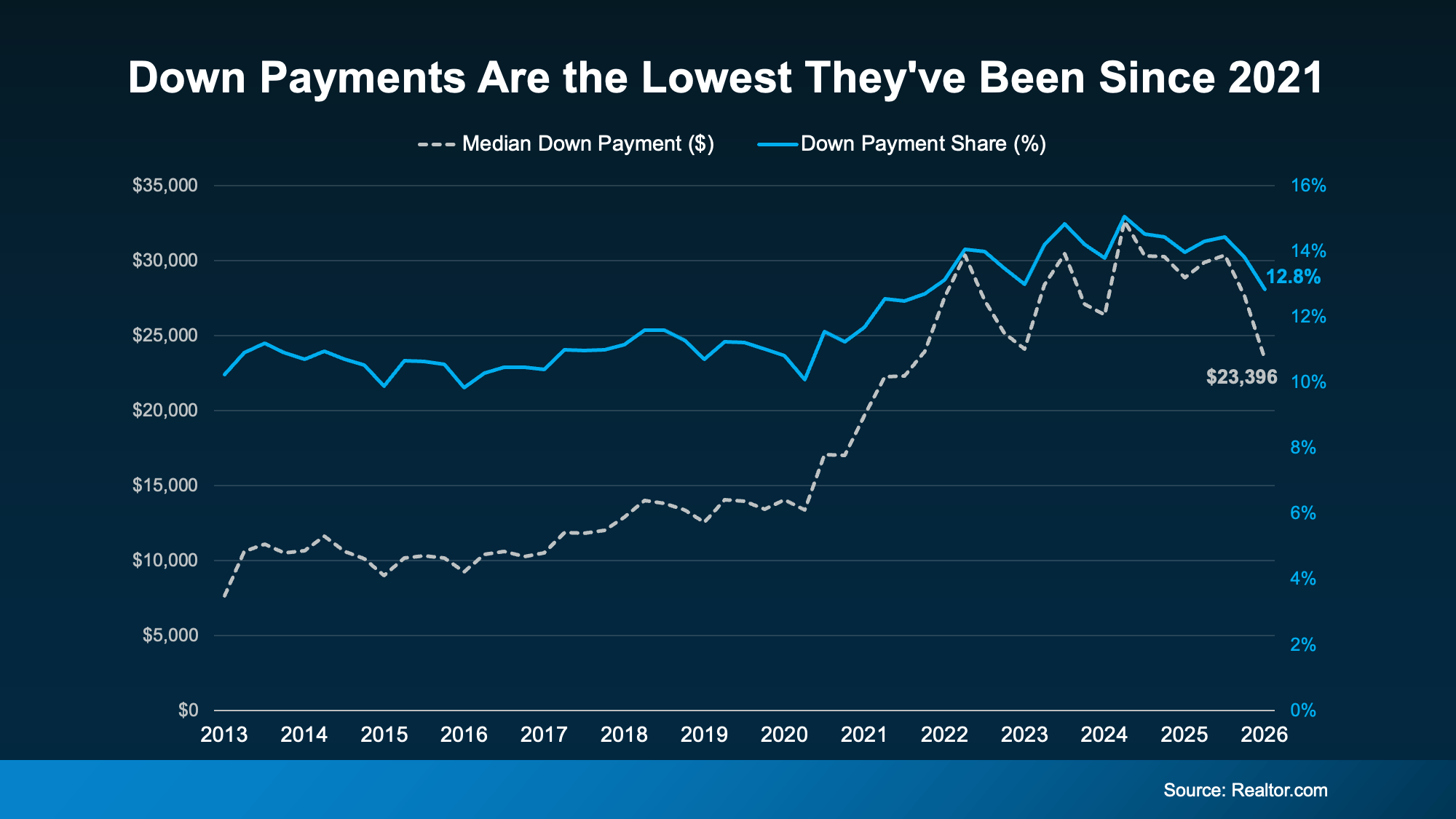

How Much Are Buyers Actually Putting Down?

Recent housing data shows that the typical buyer's down payment has fallen significantly compared to the previous year.

The average down payment in early 2026 dropped to approximately $23,400, representing nearly a 19% decrease from the year before. That's roughly $5,000 less than what buyers were typically putting down just one year earlier.

More importantly, these figures represent the smallest average down payments seen since 2021.

That's a meaningful shift for buyers who previously believed homeownership was financially out of reach.

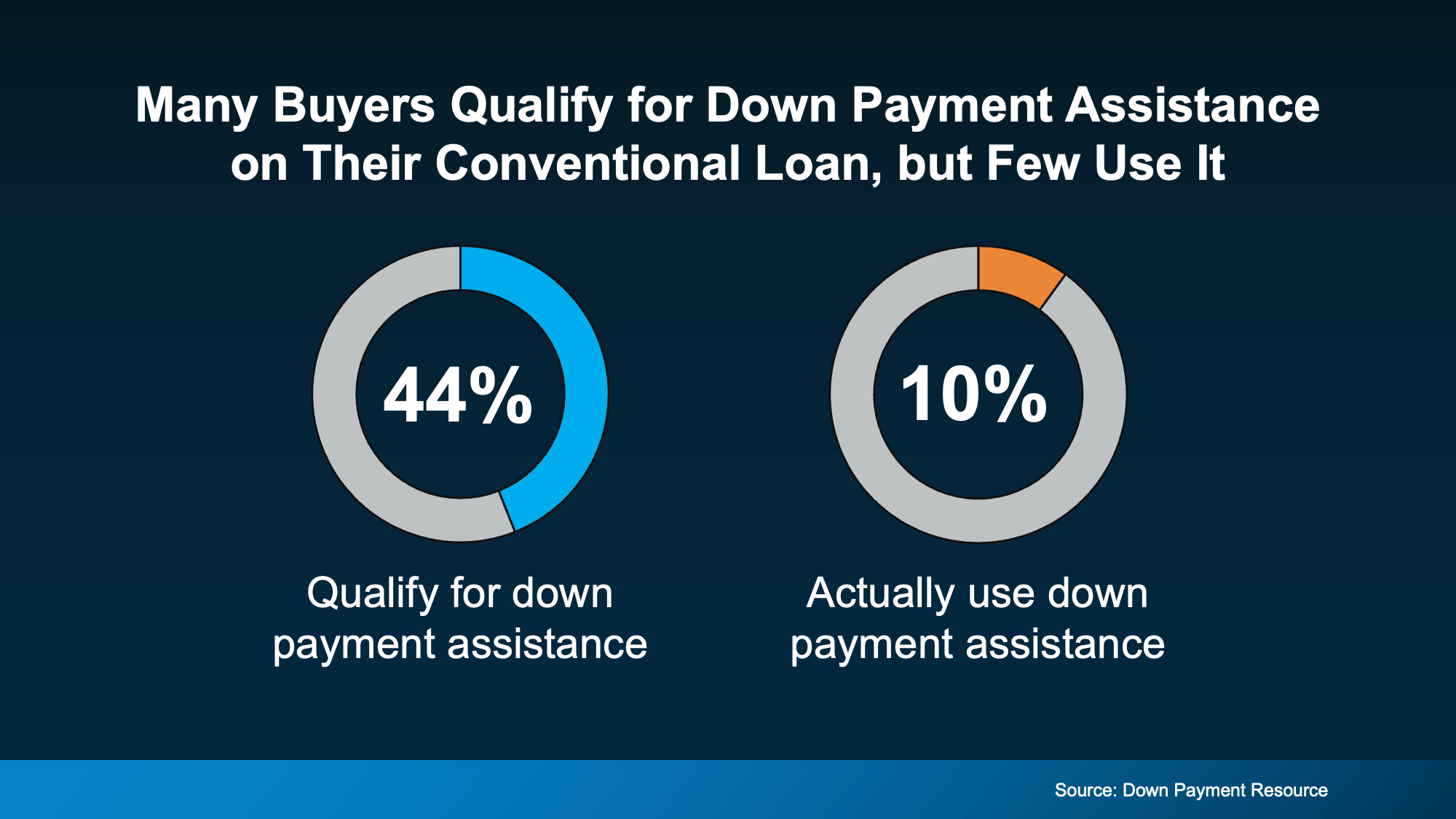

Down Payment Assistance Programs Could Save You Thousands

Even with smaller down payments, saving several thousand dollars isn't always easy.

The good news?

Many buyers qualify for financial assistance without even realizing it.

Down payment assistance programs remain one of the most underused resources in today's housing market. In fact, studies have shown that a significant percentage of buyers who were eligible for assistance completed their home purchase without ever applying for available programs.

That's like leaving free money sitting on the table.

Who Qualifies for Down Payment Assistance?

Many people mistakenly assume these programs are only available for first-time homebuyers with low incomes.

The reality is much broader.

Across the United States, there are more than 2,600 down payment assistance programs designed to help buyers overcome one of the biggest barriers to homeownership.

Many of these programs offer:

- Grants that never need to be repaid

- Forgivable loans

- Low-interest second mortgages

- Closing cost assistance

- Reduced upfront cash requirements

Even better, eligibility requirements may surprise you.

Many programs:

- Welcome first-time homebuyers.

- Also allow repeat buyers to qualify.

- Accept households earning six-figure incomes.

- Offer assistance based on location, profession, military service, or household size.

Because every program has different guidelines, speaking with a knowledgeable mortgage professional can uncover opportunities you didn't know existed.

Family Support Is Helping More Buyers Become Homeowners

Not every down payment comes entirely from personal savings.

Increasingly, parents and family members are helping loved ones purchase their first home.

Whether it's through a financial gift, assistance with closing costs, or helping strengthen a mortgage application, family support has become an important part of today's housing market.

For many families, helping the next generation buy a home isn't simply a generous gesture—it's a practical response to rising housing costs and affordability challenges.

If your family is willing and financially able to help, even a modest contribution can shorten your timeline to homeownership by months—or even years.

You Probably Don't Need 20% Down

One of the oldest myths in real estate continues to discourage countless potential buyers.

The belief that every home purchase requires a 20% down payment simply isn't true.

While putting down 20% can help borrowers avoid private mortgage insurance (PMI) on certain conventional loans, it's not a universal requirement.

Depending on your loan type and financial situation, you may qualify with a significantly smaller down payment.

That means waiting years to save a large lump sum may not always be the smartest strategy—especially if homeownership aligns with your long-term financial goals.

Should You Buy Now or Keep Waiting?

Every buyer's circumstances are different, and there's no one-size-fits-all answer.

However, today's market presents several advantages that weren't available just a few years ago:

- Smaller average down payments.

- Less buyer competition.

- Stabilizing home prices.

- Expanded access to affordable loan programs.

- Thousands of available down payment assistance opportunities.

- Greater flexibility for qualified borrowers.

If you've been delaying your home search because you assumed you didn't have enough saved, now may be the right time to revisit your options.

You might be closer to buying a home than you ever imagined.

Final Thoughts: Homeownership May Be More Within Reach Than You Think

Buying a home doesn't always require perfect timing, perfect finances, or a massive savings account.

With down payments reaching their lowest levels in years, buyers have more opportunities than they've had since 2021. Combined with government-backed mortgage programs, down payment assistance, and even family support, there are now more pathways to homeownership than many people realize.

Before assuming you need to keep saving for several more years, consider speaking with a trusted mortgage lender or real estate professional. They can help you explore financing options, determine whether you qualify for assistance programs, and create a plan tailored to your financial situation.

The dream of homeownership may be much closer than you think—and taking the first step could be easier than ever.

Recent Posts

GET MORE INFORMATION