SHOULD YOU WAIT FOR LOWER MORTGAGE RATES? THE REAL COST OF HOLDING OUT FOR THE “MAGIC NUMBER”

Buying a home is one of the biggest financial decisions most people will ever make. Naturally, everyone wants the best possible mortgage rate. Who wouldn’t? A lower interest rate sounds like the golden ticket to a smaller monthly payment and long-term savings.

But here’s the reality: many buyers are sitting on the sidelines waiting for mortgage rates to fall back into the 5% range. They’re watching the market closely, hoping that magical number appears again.

The question is — is waiting actually the smart move?

Let’s break down the numbers, the psychology behind interest rates, and the bigger picture of today’s housing market so you can make a more confident decision.

The “Magic Number” Myth: Why Buyers Fixate on the 5% Range

For many homebuyers, seeing a mortgage rate that starts with a “5” feels like a major victory. It’s almost psychological. The difference between 6.1% and 5.9% seems massive at first glance.

But is it really?

Think about it like shopping for gas. If one station sells gas at $4.10 per gallon and another sells it for $3.99, you might feel like you're getting a huge deal. The number dropped below four dollars — it feels cheaper.

Yet the actual difference per gallon might only be a few cents.

Mortgage rates work in a similar way. The shift from the low 6% range to the high 5% range may feel dramatic, but the financial impact often isn't nearly as large as buyers expect.

And this misunderstanding is causing many potential homeowners to delay their plans.

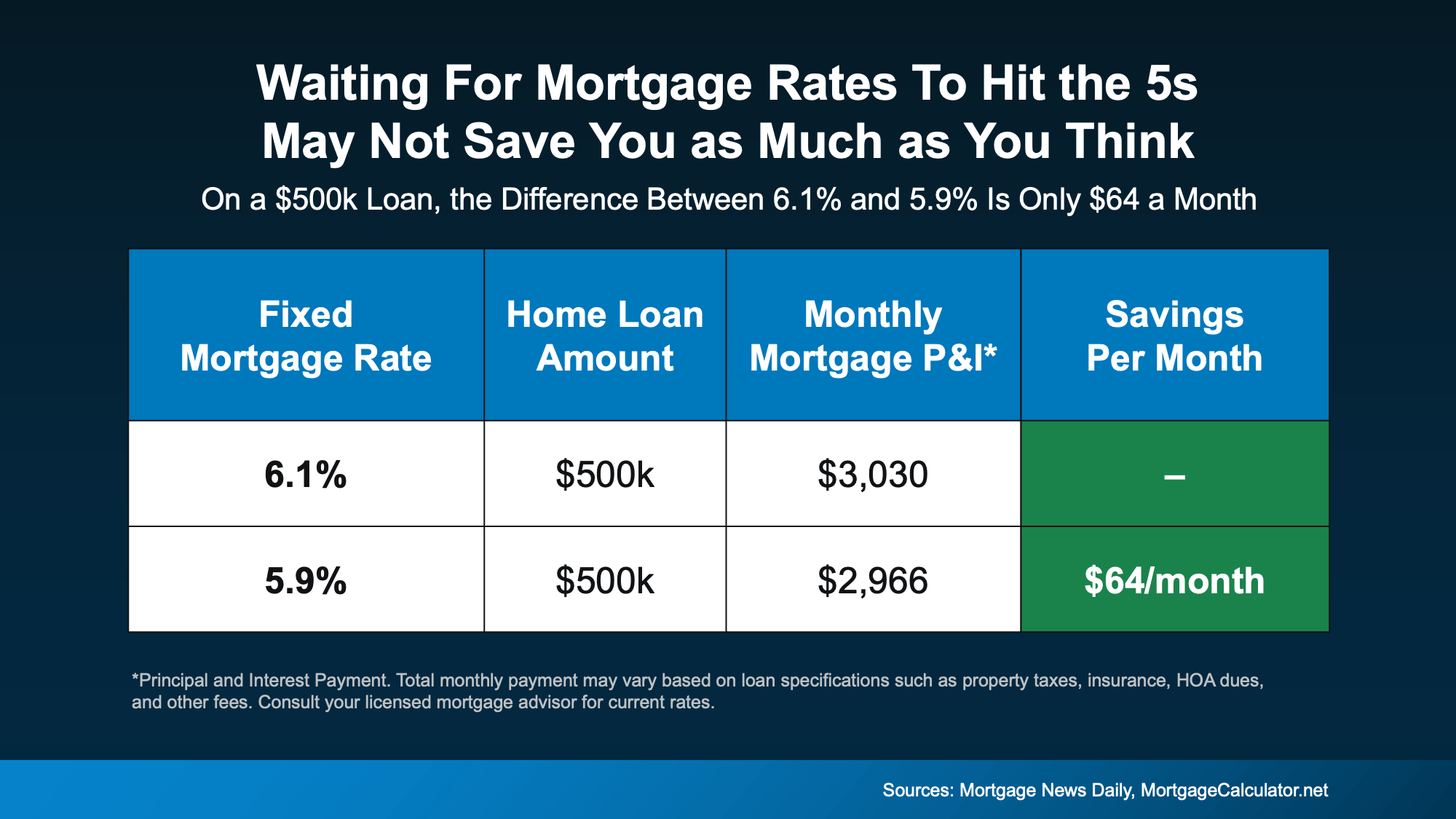

The Real Payment Difference: What the Math Actually Shows

Let’s look at a realistic example.

Imagine you’re considering a $500,000 mortgage loan.

At a 6.1% interest rate, your estimated principal and interest payment would be roughly:

$3,030 per month

Now, let’s drop that rate slightly to 5.9%.

Your monthly payment becomes approximately:

$2,966 per month

That’s a difference of:

$64 per month.

Not $300.

Not $500.

Just sixty-four dollars.

Take a moment to think about that.

Many buyers delay purchasing for months — sometimes years — waiting for that rate to start with a “5.” Yet the real monthly savings might be smaller than a typical dinner out or a streaming subscription.

Yes, over the life of the loan, that difference adds up. But for many households, it isn’t the life-changing shift they imagined.

Why Mortgage Rates Feel More Important Than They Sometimes Are

Human psychology plays a bigger role in financial decisions than we often realize.

We tend to anchor ourselves to specific numbers. In real estate, those numbers might include:

-

Home price thresholds

-

Down payment percentages

-

Mortgage rates

Once a number becomes a mental benchmark, it’s hard to let go of it.

For years, mortgage rates were historically low — hovering around 3% during the pandemic era. That environment shaped expectations. So when rates climbed into the 6% and 7% range, buyers felt like the market suddenly became unaffordable.

But markets evolve. Conditions change.

And today’s mortgage rates are already significantly lower than they were just a year ago.

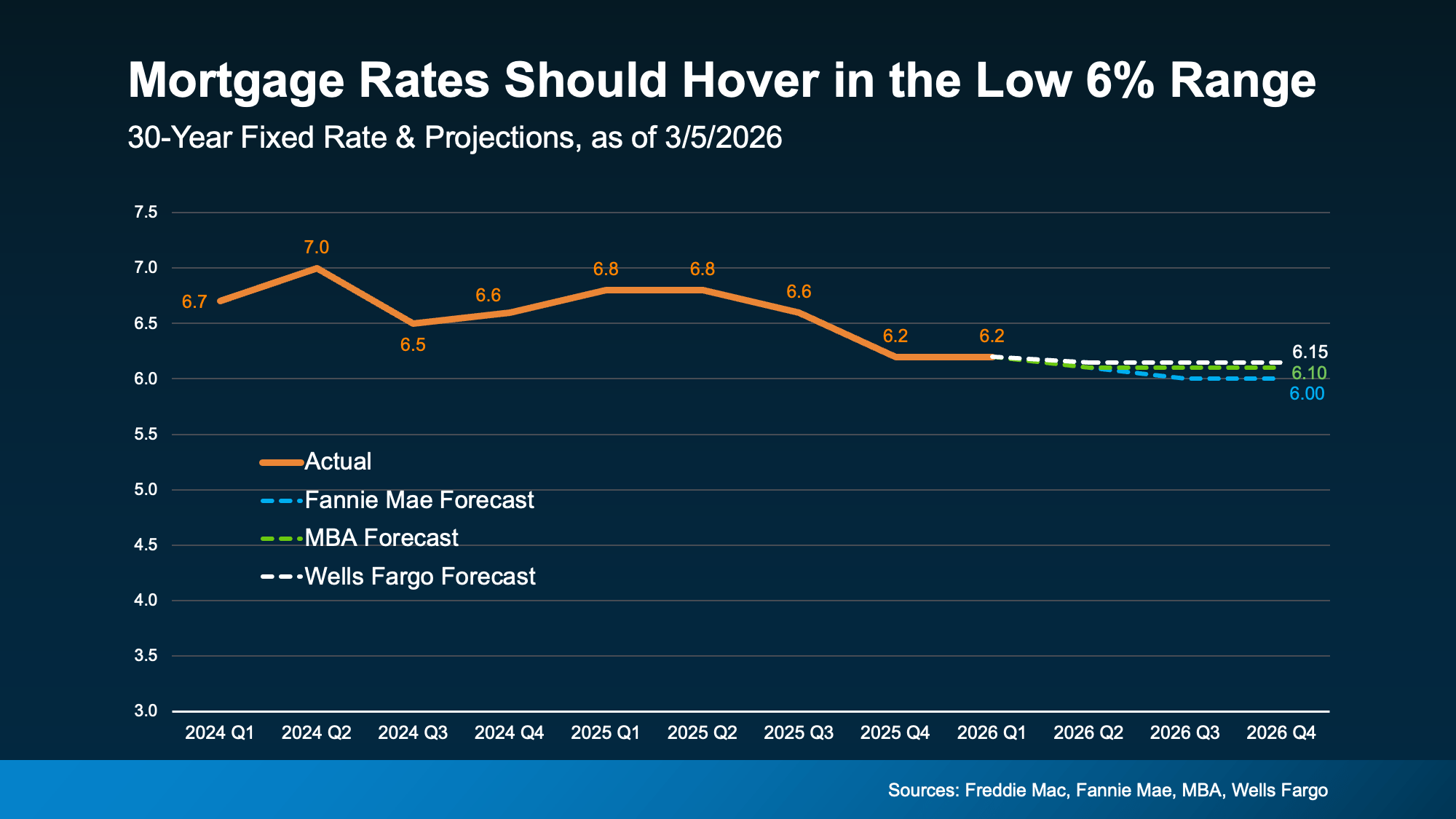

Mortgage Rate Trends: What Experts Are Actually Predicting

Many buyers are waiting for a major drop in mortgage rates, expecting them to settle comfortably back in the 5% range.

However, most housing economists aren’t forecasting that kind of dramatic shift anytime soon.

Current expectations suggest that mortgage rates will likely:

-

Fluctuate between the high 5% range and low 6% range

-

Experience short-term dips and increases

-

Remain relatively stable compared to the spikes seen in previous years

In other words, rates may occasionally dip into the high 5s — but they may not stay there consistently.

That means waiting indefinitely for a deep drop could leave buyers stuck on the sidelines longer than expected.

The More Important Question: Can You Afford the Payment Today?

Instead of asking:

“Did I miss the lowest rate?”

A better question might be:

“Does the monthly payment work for my budget right now?”

That’s the question that actually determines whether buying a home is the right move.

If your monthly payment fits comfortably within your financial plan, and you’ve found a home that meets your needs, then a small difference in mortgage rates may not be the deciding factor.

Think of buying a home like catching a flight.

Waiting for the absolute cheapest ticket might sound like a good idea — but if you wait too long, the flight may fill up or prices may rise again.

Sometimes the better move is securing a seat when the opportunity makes sense for you.

Don’t Forget the Power of Refinancing

Here’s another important factor many buyers overlook.

Mortgage rates are not permanent.

If interest rates drop significantly in the future, homeowners have the option to refinance their loan. Refinancing allows you to replace your current mortgage with a new one at a lower rate.

That means you can benefit from lower rates later.

But there’s one thing you can’t refinance:

A home you never purchased.

Waiting for the perfect rate might delay homeownership — and in the meantime, home prices or competition could change the equation.

The Housing Market Has Already Improved From Last Year

It’s easy to forget how much conditions have shifted.

Not long ago, mortgage rates were sitting in the 7% range. Compared to that environment, today’s low-6% rates already represent a meaningful improvement.

That difference alone can significantly impact affordability.

For many buyers who paused their home search when rates were higher, now may be the perfect time to revisit the numbers.

The payment scenario today could look far more manageable than it did just a year ago.

Waiting Feels Safe — But It Isn’t Always Strategic

Delaying a major purchase can feel like the cautious approach. After all, everyone wants to make the smartest financial decision possible.

But sometimes waiting creates its own risks.

For example:

-

Home prices could increase while you wait

-

Competition from other buyers could return

-

Inventory could shrink in desirable areas

-

Mortgage rates could remain stable instead of falling

In other words, the market doesn’t stand still while buyers wait for the perfect moment.

Real estate decisions are rarely about perfect timing. More often, they’re about finding a moment when the numbers make sense for your personal situation.

Re-Running the Numbers Might Surprise You

If you paused your home search when mortgage rates were higher, now may be the right time to revisit your financial calculations.

Run the numbers again.

Look at:

-

Your potential monthly payment

-

Current mortgage rates

-

Available homes in your target price range

You might discover something surprising.

What once felt out of reach could now be comfortably within your budget.

Sometimes the opportunity we think we missed never actually disappeared — it just looks different than we expected.

The Bottom Line: Waiting for the “Perfect” Mortgage Rate May Not Pay Off

Waiting for mortgage rates to fall into the perfect range might sound like a smart strategy. But in many cases, the financial difference between rates like 6.1% and 5.9% is smaller than buyers imagine.

The real question isn’t whether you caught the lowest rate in the market.

The real question is whether today’s payment works for your financial goals.

If the numbers make sense, the home meets your needs, and the payment fits comfortably in your budget, it may be worth taking a closer look at your options now rather than waiting for a hypothetical future rate.

Because in real estate, the best opportunities aren’t always the ones that look perfect on paper — they’re the ones that fit your life when the timing is right.

Thinking about buying but unsure if the numbers work?

Take another look at the math for your price range. You might find that homeownership is already closer than you think.

Recent Posts

GET MORE INFORMATION