WHAT RISING INFLATION Means for Home Buyers and Sellers in Today's Housing Market

Inflation is once again making headlines, and for good reason. Recent economic data suggests that inflation is moving higher instead of lower, creating fresh uncertainty for consumers, investors, and especially those planning to buy or sell a home.

But before you assume the sky is falling, it's important to understand what's actually happening beneath the headlines.

What does rising inflation really mean for the housing market? How could it impact mortgage rates? And should buyers and sellers put their plans on hold?

Let's break it all down.

Understanding Inflation: Why Prices Are Climbing Again

Inflation measures how much the cost of goods and services increases over time. When inflation rises, everyday expenses become more expensive—from groceries and utilities to transportation and housing.

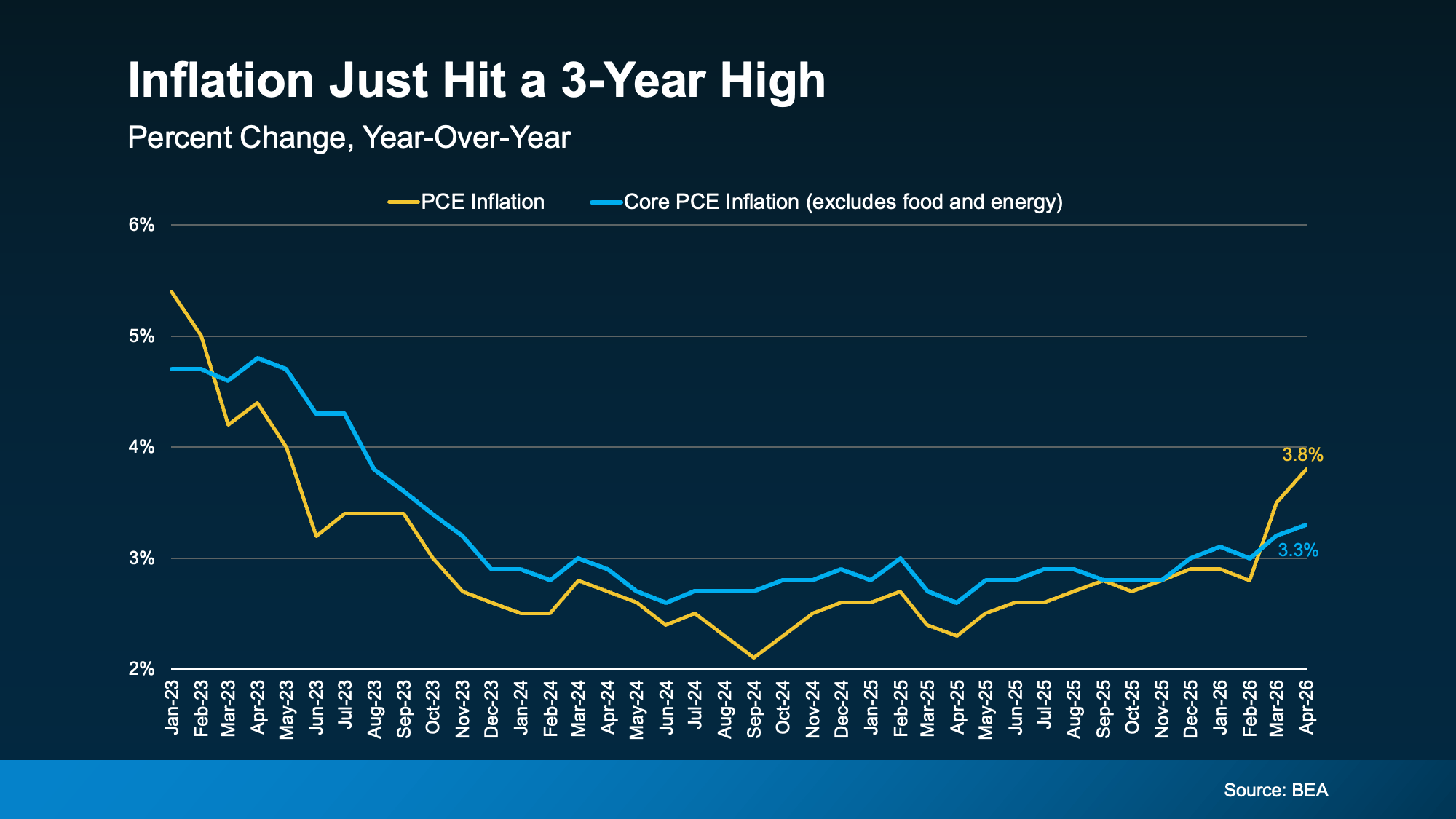

One of the key indicators economists watch is the Personal Consumption Expenditures (PCE) Price Index. This metric tracks consumer spending and measures changes in the prices people pay for products and services throughout the economy.

Recently, the PCE index has shown a noticeable increase, signaling that inflation is moving in the wrong direction.

If you've felt like your paycheck isn't stretching quite as far lately, you're not imagining it. Higher prices are impacting households across the country, and the latest data confirms that trend.

The Hidden Story Behind the Inflation Numbers

While the headline inflation number has grabbed attention, there's another figure that deserves a closer look: Core PCE.

Core PCE measures inflation just like the standard PCE index, but it excludes food and energy prices. Why? Because those categories tend to experience sharp swings that can distort the bigger picture.

Interestingly, Core PCE is rising at a much slower pace than overall inflation.

That's an important distinction.

A significant portion of the recent inflation increase appears to be tied to higher energy costs, largely influenced by ongoing geopolitical tensions and instability in global oil markets.

Think of it like a temporary storm cloud passing overhead. While it certainly affects current conditions, it may not represent a long-term shift in the broader economy.

If energy markets stabilize and global tensions ease, inflation could gradually cool down as well.

How Inflation Affects Mortgage Rates

For anyone considering a move, this is where things become especially relevant.

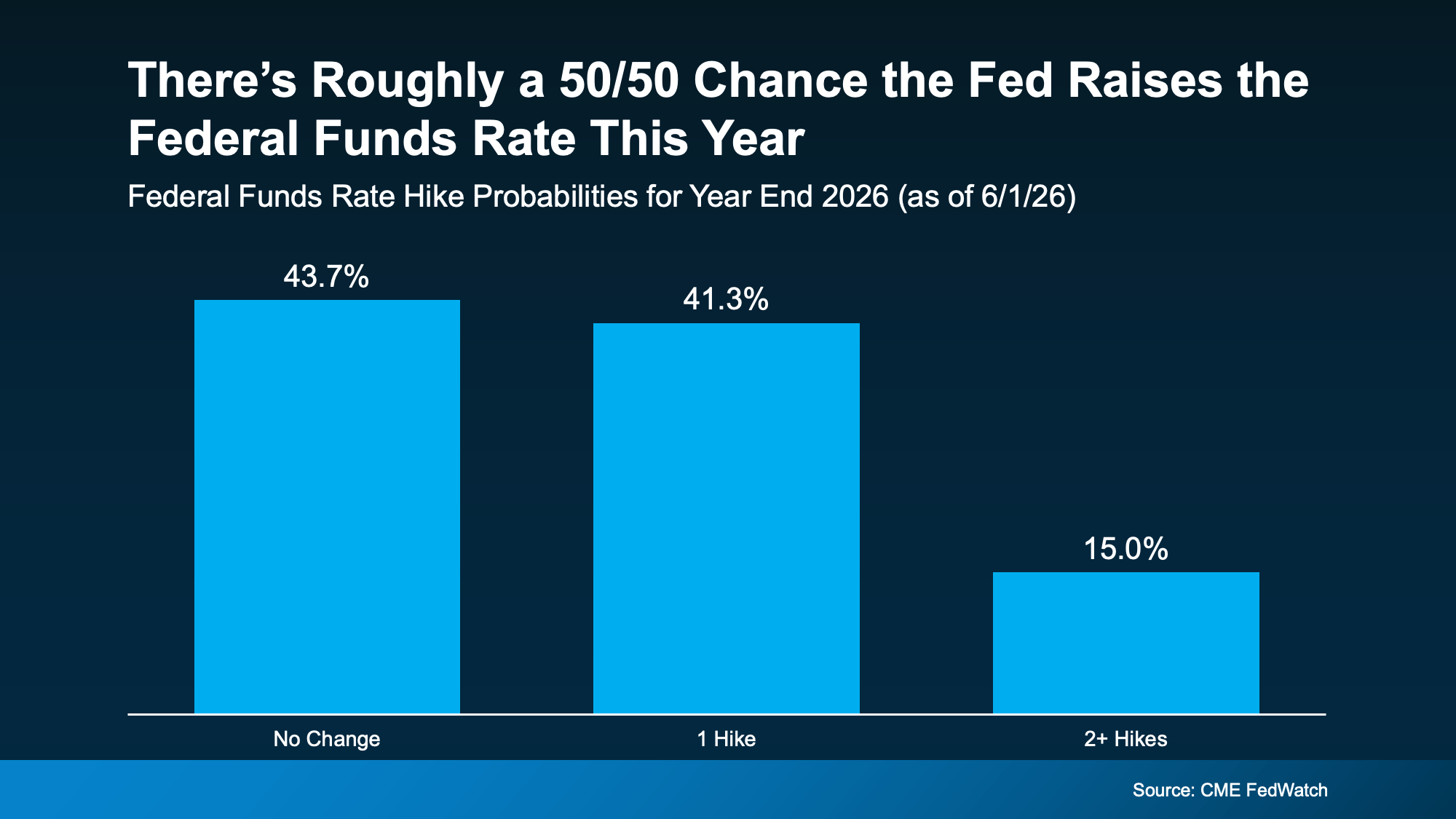

When inflation remains elevated, the Federal Reserve often responds by maintaining higher interest rates or even increasing them further. The goal is simple: slow spending, reduce demand, and bring inflation back under control.

Although mortgage rates don't directly follow the Federal Funds Rate, they are heavily influenced by the same economic forces.

As inflation persists, lenders typically demand higher returns to offset the loss of purchasing power caused by rising prices. The result? Mortgage rates tend to remain elevated.

For buyers hoping to see a dramatic drop in borrowing costs anytime soon, recent inflation data suggests patience may still be required.

The reality is that the "higher-for-longer" interest rate environment remains a very real possibility.

Why Mortgage Rates May Stay Higher Than Expected

Many prospective buyers entered the year expecting mortgage rates to gradually decline.

However, inflation has complicated that outlook.

As long as inflation remains above the Federal Reserve's target range, policymakers are likely to maintain a cautious stance. Any hopes for aggressive rate cuts may be delayed if economic data continues to show persistent price pressures.

This means mortgage rates could remain relatively high throughout the near future.

For homebuyers, that creates a challenging environment. Monthly payments remain elevated, affordability remains tight, and competition for well-priced homes can still be intense in many markets.

But waiting indefinitely for the perfect rate can also come with risks.

Home prices continue to appreciate in many areas, and delaying a purchase could mean paying more for the same property later.

The key is understanding your financial situation and making decisions based on your goals—not market speculation.

Rising Inflation Doesn't Mean a Housing Crash Is Coming

Whenever economic uncertainty increases, many people immediately think back to the housing collapse of 2008.

But today's market conditions are fundamentally different.

In fact, comparing the current housing market to 2008 is like comparing a rainstorm to a hurricane. Both involve bad weather, but the scale and causes are completely different.

Here's why.

Housing Inventory Remains Limited

One of the biggest factors supporting home values today is the ongoing shortage of available homes.

Unlike the years leading up to the 2008 crash, there isn't an overwhelming supply of properties flooding the market.

Low inventory continues to create competition among buyers, helping support home prices even during periods of economic uncertainty.

Homeowners Have Built Significant Equity

Today's homeowners are sitting on historically strong levels of equity.

Many purchased or refinanced during periods of exceptionally low interest rates and have seen substantial home value appreciation over the past several years.

This financial cushion reduces the likelihood of widespread distressed sales.

Lending Standards Are Much Stronger

Prior to the housing crisis, mortgage qualification standards were considerably looser.

Today, lenders require more documentation, stricter income verification, and stronger credit profiles.

As a result, homeowners are generally better positioned to manage their mortgage obligations.

Affordability Is the Challenge—Not Foreclosures

The biggest obstacle facing today's market isn't a wave of foreclosures or underwater mortgages.

It's affordability.

Higher home prices combined with elevated mortgage rates have made homeownership more difficult for many buyers.

That creates challenges, but it's not the same set of circumstances that led to the housing crash nearly two decades ago.

Smart Strategies for Buyers in a High-Rate Environment

Even when mortgage rates are elevated, opportunities still exist for motivated buyers.

The most successful homebuyers focus on strategy rather than trying to perfectly time the market.

Here are several approaches worth considering.

Explore Alternative Loan Options

Not every mortgage has to be a traditional fixed-rate loan.

Adjustable-rate mortgages (ARMs), temporary rate buydowns, and other financing programs may help reduce initial monthly payments depending on your situation.

A knowledgeable lender can explain which options align with your goals and risk tolerance.

Take Advantage of Buyer Assistance Programs

Many first-time buyers are surprised to learn how many assistance programs are available.

Down payment assistance grants, closing cost support, and local housing incentives can significantly reduce upfront expenses.

Researching available programs could save thousands of dollars.

Negotiate Seller Concessions

In some markets, sellers are willing to contribute toward closing costs or rate buydowns to help facilitate a transaction.

These concessions can improve affordability and reduce out-of-pocket expenses.

Stay Ready for Market Changes

Mortgage rates can move quickly.

When opportunities arise, buyers who are financially prepared often have an advantage.

Maintaining communication with your lender and real estate professional can help you act confidently when conditions improve.

What Sellers Should Know Right Now

Sellers shouldn't assume higher rates have eliminated buyer demand.

Life events still drive housing decisions.

People relocate for jobs, grow their families, downsize after retirement, and move for countless personal reasons regardless of interest rate trends.

However, today's buyers are more price-sensitive than they were during the ultra-low-rate era.

That means accurate pricing, effective marketing, and professional guidance are more important than ever.

Homes that are priced appropriately and presented well continue to attract serious buyers.

The Bottom Line: Strategy Matters More Than Timing

Inflation remains above the Federal Reserve's preferred level, and that means mortgage rates may stay elevated longer than many people expected.

However, that doesn't mean buyers and sellers should put their lives on hold.

Real estate has always been about more than interest rates. It's about personal goals, financial readiness, and making informed decisions based on your unique circumstances.

Trying to perfectly predict the market is nearly impossible. Developing a smart strategy, on the other hand, is completely within your control.

Whether you're thinking about buying your first home, upgrading to a larger property, or selling your current house, understanding the economic landscape can help you make confident decisions.

The market may be challenging, but challenges create opportunities for those who are prepared. The key is having the right plan—and the right professionals—guiding you every step of the way.

Recent Posts

GET MORE INFORMATION