How Your Home Equity Can Unlock Homeownership for the Next Generation

Let’s be honest for a second.

If you’re a parent or grandparent watching your kids struggle to buy their first home, it’s tough. You remember what owning a home did for you. It gave you stability. It gave you control. It quietly built wealth in the background while you were busy living your life.

And now? You’re watching the next generation face rising home prices, higher mortgage rates, and intimidating upfront costs. It can feel like they’re running uphill in a storm.

But here’s something many homeowners don’t realize:

You may already hold the solution — and it’s sitting inside your home.

The Hidden Power of Home Equity

If you’ve owned your home for years — maybe even decades — two powerful forces have likely been working in your favor:

-

Property values have risen.

-

Your mortgage balance has shrunk… or disappeared entirely.

That combination creates equity. And for many homeowners today, that equity isn’t small — it’s substantial.

Home equity is simply the difference between what your home is worth and what you owe on it. But it’s more than a number on paper. It’s leverage. It’s flexibility. It’s opportunity.

Most people think of equity as a retirement cushion. And yes, it absolutely can be that. But it can also serve another meaningful purpose: helping your children or grandchildren overcome the single biggest obstacle standing between them and homeownership.

The Real Reason Young Buyers Are Struggling

You might assume high mortgage rates are the biggest problem. Or skyrocketing home prices.

Surprisingly, they’re not.

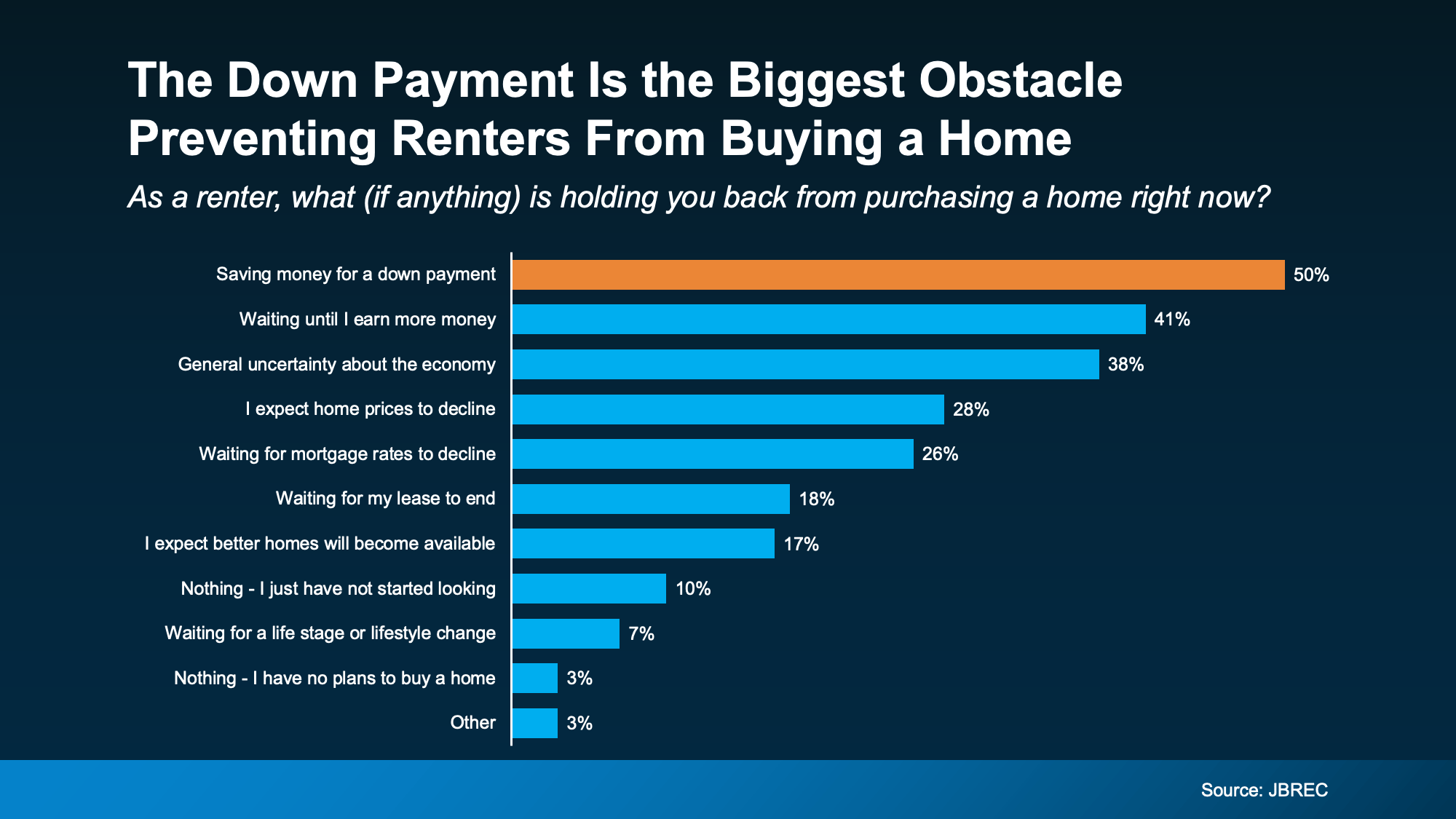

Research from John Burns Research & Consulting shows that the top reason renters aren’t buying homes isn’t rates or prices — it’s the upfront cost.

Specifically? The down payment.

Think about it. Even a modest 5% to 10% down payment on today’s home prices can mean tens of thousands of dollars. For young buyers juggling rent, student loans, childcare, and everyday expenses, saving that amount can feel nearly impossible.

They’re not unwilling.

They’re stuck at the starting line.

And that’s where you may be able to step in — without jeopardizing your own financial security.

Why Your Equity Puts You in a Unique Position

Here’s the reality: you can’t control mortgage rates. You can’t control home prices. But you may be able to influence something far more important — the down payment hurdle.

A small portion of your equity could provide:

-

A down payment gift

-

A low-interest family loan

-

Early access to inheritance funds

-

Co-investment support

Even a relatively modest contribution can dramatically change the math for a first-time buyer. Lower down payment stress can mean:

-

Faster entry into the market

-

Smaller monthly mortgage insurance costs

-

Immediate equity growth once they purchase

It’s like helping someone across a river. You’re not carrying them the whole way — you’re just giving them the stepping stone they need.

And here’s the key: helping doesn’t have to mean draining your retirement funds.

Generational Wealth Transfer Is Already Happening

Over the next two decades, experts estimate between $68 trillion and $84 trillion will transfer from older generations to younger ones.

That’s not a typo. Trillions.

Families across the country are rethinking when and how that wealth is passed down. Instead of waiting for inheritance to transfer later in life, some are asking a powerful question:

What if we help when it matters most?

For many young adults, the moment of maximum impact isn’t at age 60. It’s when they’re trying to establish stability in their 20s or 30s.

And increasingly, families are acting on that insight.

Family Support Is Fueling First-Time Homeownership

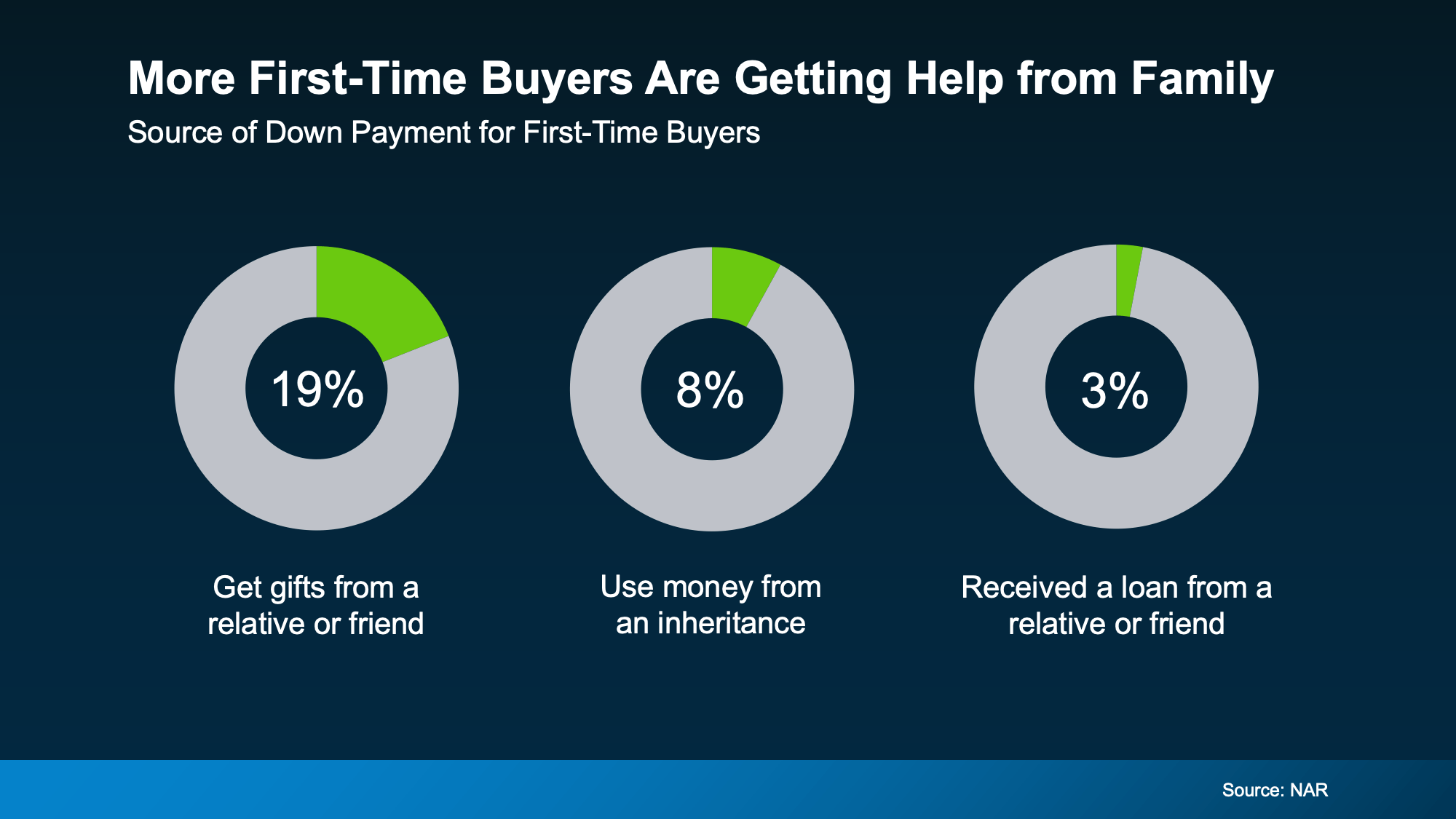

According to the National Association of Realtors, nearly 1 in 5 first-time homebuyers use a cash gift from a family member or loved one to help with their down payment.

That’s significant.

It means family-assisted homeownership is no longer rare — it’s common.

Some buyers receive outright gifts. Others receive loans. Some use inheritance funds early. The methods vary, but the outcome is the same: access.

And access to homeownership often leads to:

-

Long-term wealth building

-

Forced savings through mortgage payments

-

Protection against rising rent

-

Emotional stability and community roots

In other words, it’s not just about buying a house.

It’s about building a foundation.

This Isn’t Obligation — It’s Opportunity

Let’s be clear.

This is not about pressure. It’s not about guilt. And it’s definitely not about sacrificing your own financial well-being.

Every family’s situation is different.

But if you’ve built significant equity, you may have more flexibility than you think. And sometimes, even a small move can create a ripple effect that lasts generations.

Helping a loved one buy a home isn’t just writing a check. It’s offering:

-

Stability in uncertain times

-

A foothold in a competitive market

-

A launching pad for future wealth

It’s planting a tree whose shade they’ll sit under for decades.

Strategic Ways to Use Equity Without Putting Yourself at Risk

If you’re considering this path, strategy matters.

Here are a few thoughtful options homeowners explore:

1. Cash-Out Refinance

You refinance your mortgage for more than you owe and take the difference in cash. This can provide funds while potentially adjusting your loan terms.

2. Home Equity Line of Credit (HELOC)

A HELOC allows you to borrow against your equity as needed, often with flexible repayment structures.

3. Downsizing

Selling your current home and purchasing a smaller one may free up significant equity to share.

4. Structured Family Loan

Instead of a gift, you provide a formal loan with agreed-upon repayment terms, keeping it businesslike and clear.

Of course, any of these moves should be discussed with financial and tax professionals. The goal is to empower — not overextend.

The Emotional Return on Investment

Let’s step away from spreadsheets for a moment.

Remember how it felt when you got the keys to your first home?

The pride.

The relief.

The sense of arrival.

Now imagine watching your child or grandchild experience that — knowing you helped make it possible.

That’s not just a financial return. That’s emotional ROI.

And unlike market swings or interest rate fluctuations, that kind of return compounds in a different way — through security, gratitude, and generational progress.

Why Timing Can Matter

Markets shift. Conditions improve. Affordability fluctuates.

But the longer someone waits to enter the housing market, the longer they delay building equity of their own.

Homeownership works like a slow-cooking meal. The magic happens over time. Appreciation, loan amortization, tax advantages — they accumulate gradually.

Helping sooner can mean decades of additional wealth-building potential.

And sometimes, the difference between “someday” and “now” is simply the down payment.

Is This the Right Move for Your Family?

That depends.

Ask yourself:

-

Is my retirement fully protected?

-

Do I have a financial cushion?

-

Would helping now reduce future financial strain for them?

-

Is this aligned with our family’s values?

If the answers feel encouraging, it may be worth exploring further.

Because sometimes the most powerful investment isn’t in stocks, bonds, or savings accounts.

It’s in people.

The Bigger Picture: Legacy Over Assets

At the end of the day, equity is more than a financial metric.

It represents years of discipline. Years of payments. Years of believing in long-term growth.

Using a portion of that equity to help the next generation isn’t about losing something.

It’s about multiplying impact.

Your home may have built your net worth quietly over time.

Now it could help build theirs.

Bottom Line: Start with a Conversation

You don’t need to make a decision today.

You don’t need to restructure your finances overnight.

But if you’re curious about what your home equity could make possible — for you or for someone you love — start with a conversation.

Talk to a trusted real estate professional. Speak with a financial advisor. Explore the numbers calmly and strategically.

Because sometimes the most meaningful investment you can make isn’t in the market.

It’s in the future of your family.

And that kind of return?

That lasts far beyond any mortgage term.

Recent Posts

GET MORE INFORMATION