Unlock The Power Of Your Home Equity: 4 Smart Ways To Turn It Into Real Wealth

You’ve probably heard the buzz: homeowners are sitting on record levels of equity. But what does that actually mean for you?

Is it just a feel-good statistic? Or is it something you can actually use?

Here’s the truth: your home equity isn’t just a number on paper. It’s leverage. It’s opportunity. It’s a financial engine quietly building strength in the background while you live your life.

And if you understand how to use it, it can change your next chapter in a big way.

Let’s break it down.

What Is Home Equity And Why Does It Matter?

At its core, home equity is simple.

It’s the difference between what your home is worth and what you still owe on your mortgage.

As you pay down your loan and as home values rise over time, your ownership stake grows. Think of it like planting a tree. Each mortgage payment is water. Each year of appreciation is sunlight. Over time, that tree becomes strong, valuable, and deeply rooted.

That’s your equity.

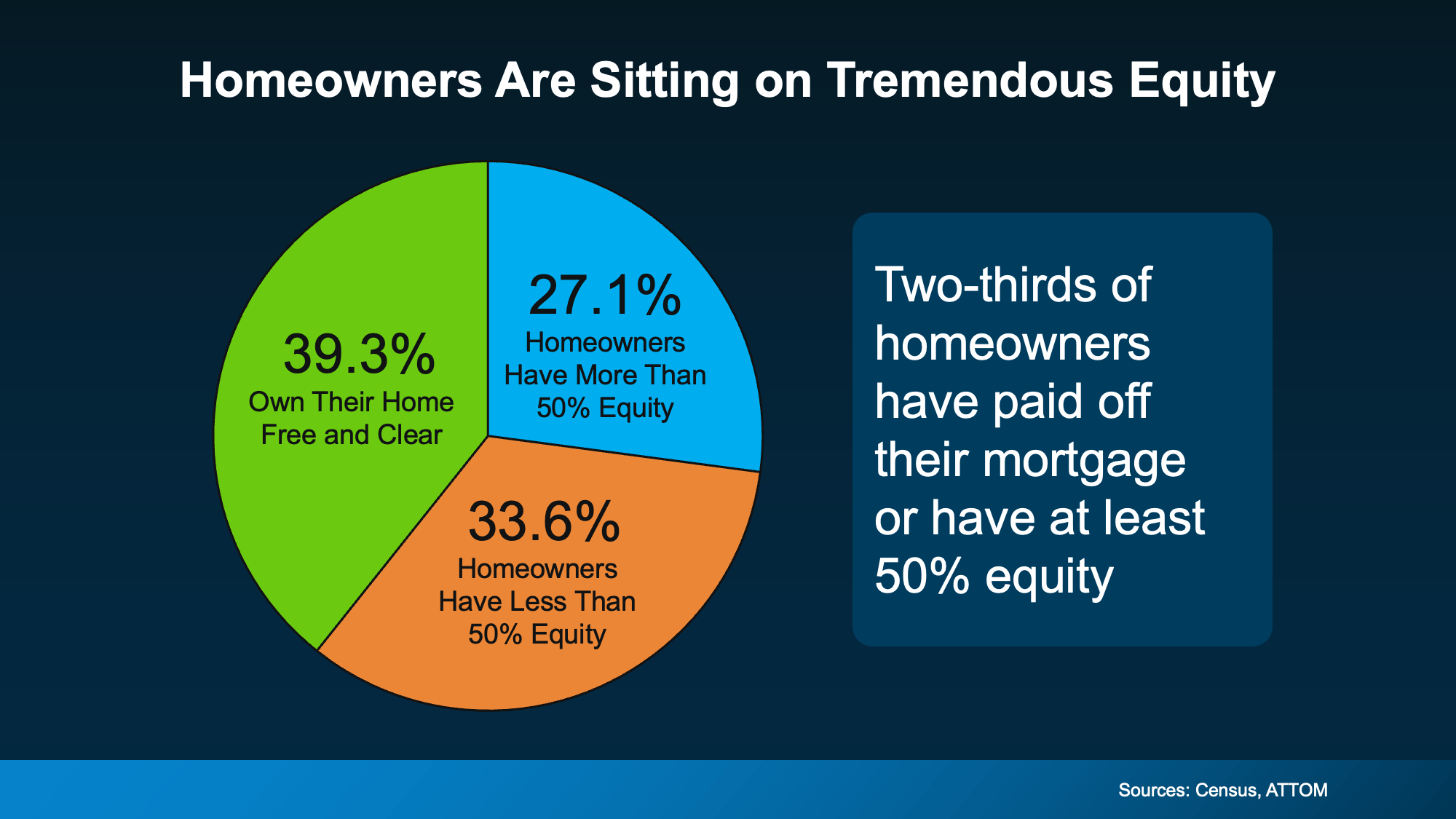

And right now, many homeowners are in an incredibly strong position.

Recent housing data shows that roughly two-thirds of homeowners have built significant equity. Nearly 39% own their homes outright, meaning no mortgage at all. Another 27% have at least 50% equity.

That’s not small change.

In fact, the average homeowner is sitting on close to $300,000 in equity. Six figures. Real wealth.

Now the question becomes: how can you put that to work?

1. Use Your Equity To Move Into The Right Home

Life changes. Your home should keep up.

Maybe your family has grown and your current space feels tight. Maybe your kids have moved out and now you’re maintaining rooms you barely use. Or maybe your commute, neighborhood, or lifestyle needs have shifted.

Equity gives you options.

You can use it as a down payment on your next home. And in some cases, homeowners have enough equity to buy their next property in cash.

Imagine that.

No mortgage. No monthly payment. Just ownership.

Even if you’re not buying outright, a larger down payment can lower your monthly mortgage, reduce your interest rate, and improve your loan terms. It’s like walking into your next home purchase with leverage already in your pocket.

Instead of starting from scratch, you’re building on a solid foundation.

2. Reinvest In Your Current Home Through Strategic Renovations

Not ready to move?

That’s okay. Your equity can still work for you.

Reinvesting in your home through renovations can increase its value and improve your lifestyle at the same time. Think updated kitchens, modern bathrooms, energy-efficient upgrades, or expanded living space.

But here’s the key: be strategic.

Not every renovation delivers the same return on investment. Some projects look great but don’t significantly boost resale value. Others, like kitchen upgrades or curb appeal improvements, can make a big impact.

Before you dive into a remodeling project, talk to a local real estate professional. They understand your market. They know what buyers want. They can guide you toward improvements that make financial sense.

It’s like tuning up a car before selling it. A little investment in the right places can significantly increase the final sale price.

And in the meantime? You get to enjoy the upgrades.

3. Leverage Your Home Equity To Fund Major Life Goals

Here’s where things get interesting.

Home equity isn’t just about real estate. It’s about freedom.

Many homeowners tap into their equity to pursue meaningful financial goals, such as:

-

Starting a business

-

Funding college tuition

-

Supplementing retirement savings

-

Paying off high-interest debt

-

Helping a loved one with a down payment

Think of your equity as stored potential energy. When used wisely, it can power something transformative.

For example, if you’ve always dreamed of launching your own business but lacked startup capital, your equity could provide that funding. If retirement is approaching and you want to strengthen your financial cushion, tapping equity strategically might help.

Some families are even using their built-up wealth to support the next generation. Helping a child purchase their first home isn’t just generous. It’s generational wealth in action.

Of course, this isn’t a decision to take lightly. That’s why working with a financial advisor is critical. You want to understand tax implications, repayment terms, and long-term impact before making a move.

But the opportunity is there.

And for many homeowners, it’s substantial.

4. Use Equity As A Safety Net During Financial Hardship

Let’s talk about something less glamorous but equally important: protection.

Life doesn’t always go according to plan. Job loss. Medical issues. Unexpected expenses. Financial hardship can hit fast.

If you’re struggling to keep up with mortgage payments, equity can act as a lifeline.

Rather than facing foreclosure, many homeowners in tough situations choose to sell. Because of their equity position, they’re often able to pay off their mortgage and walk away with money in hand.

That’s a powerful difference.

During the housing crash of 2008, many homeowners had little to no equity. When values dropped, they were underwater. Today, the landscape is very different. Most homeowners maintain strong equity positions, often well above 20%.

That 20% threshold matters. It provides a financial cushion. It protects you from volatility. It gives you flexibility if circumstances change.

According to recent industry data, mortgage holders collectively have trillions in home equity, with a large portion considered “tappable” while still maintaining that crucial 20% buffer.

In simple terms? Most homeowners have room to maneuver.

How To Safely Tap Into Your Home Equity

If you’re thinking about using your equity, don’t rush.

Here’s a smart, practical approach:

Step 1: Get A Professional Equity Assessment

Start by connecting with a trusted local real estate agent. Ask for a personalized market analysis to determine your home’s current value.

Online estimates can be helpful, but they’re not precise. A professional evaluation gives you a clearer picture of what you’re actually working with.

Step 2: Review Your Loan-To-Value Ratio (LTV)

Your loan-to-value ratio compares your remaining mortgage balance to your home’s current market value.

Financial experts generally recommend maintaining at least 20% equity. That means your LTV should ideally stay at 80% or lower, even after tapping into equity.

Why? Because it preserves flexibility and protects you from market shifts.

Step 3: Meet With A Financial Advisor

Before making any major decision, sit down with a financial professional. Discuss:

-

Interest rates

-

Tax implications

-

Long-term financial goals

-

Risk tolerance

-

Repayment strategies

Your home is likely your largest financial asset. Treat decisions about it with the same care you’d give a major investment.

Because that’s exactly what it is.

Why Today’s Homeowners Are In A Stronger Position

Compared to past housing cycles, today’s homeowners are generally more secure.

Stricter lending standards over the last decade have reduced risky borrowing. Many homeowners refinanced into low interest rates. And consistent appreciation has significantly boosted equity levels.

That means you’re not just sitting on value. You’re sitting on stability.

And stability creates opportunity.

The Bottom Line: Your Equity Is A Tool, Not Just A Statistic

Your home equity is one of the most powerful financial assets you own.

It can help you:

-

Move into a better-fitting home

-

Upgrade your current space

-

Achieve major life goals

-

Protect yourself during tough times

But like any powerful tool, it must be used wisely.

So here’s a question for you:

If you had access to your home equity today, what would you do with it?

Would you upgrade your lifestyle? Build your business? Help your family? Secure your retirement?

The opportunity may already be sitting in your walls.

You just have to decide how to unlock it.

Recent Posts

GET MORE INFORMATION