Unlocking Your Home's Potential: The Benefits of Using Equity for a Bigger Down Payment

Did you know that homeowners have a unique advantage when it comes to making a larger down payment on their next property? By leveraging the equity in their current home, they can significantly boost their financial standing during the buying process. As home equity continues to reach new heights, so too does the median down payment for new homebuyers.

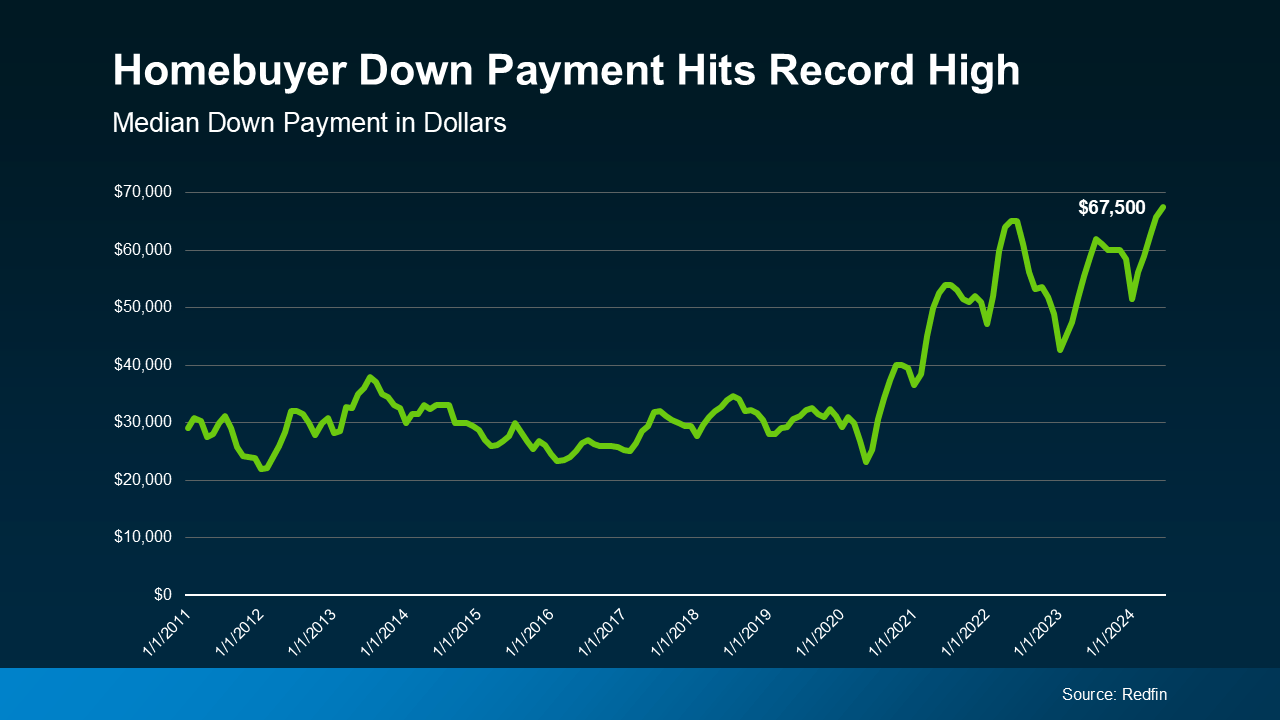

According to recent data from Redfin, the average down payment for U.S. homebuyers is now $67,500—an increase of nearly 15% compared to last year and the highest amount on record. But why is this happening? Let’s break it down.

The Power of Home Equity

Over the past several years, home prices have skyrocketed, leading to a substantial increase in equity for many homeowners. When you sell your current home, the equity you’ve built up can be applied toward a larger down payment on your new home. This presents a significant opportunity, especially if you've been worried about affordability in today’s market.

Understanding Down Payment Options

It's essential to remember that making a large down payment isn’t a requirement. There are loan programs available that allow for down payments as low as 3% or even 0%. However, many homeowners are opting for larger down payments because of the benefits they offer. Let’s explore those advantages in detail.

Why a Bigger Down Payment is a Game Changer

1. Borrow Less and Save More

Using your home equity to increase your down payment means you’ll borrow less for your new home. The less you borrow, the less interest you’ll pay over the life of your loan. This means significant savings for you in the long run, keeping more money in your pocket for other expenses or investments.

2. Secure a Lower Mortgage Rate

When you put down a larger down payment, it signals to lenders that you’re a lower credit risk. A larger upfront payment can bolster your financial credibility, which often results in a more favorable mortgage rate. This can lead to even more savings throughout the duration of your loan.

3. Reduce Monthly Payments

A bigger down payment doesn’t just decrease the total loan amount; it also leads to lower monthly mortgage payments. This can make your new home more affordable and provide you with extra flexibility in your budget, allowing for other financial goals like saving for retirement or vacations.

4. Avoid Private Mortgage Insurance (PMI)

One of the best perks of putting down 20% or more is that you can bypass Private Mortgage Insurance (PMI). This insurance is an extra cost that many buyers face when their down payment is less than 20%. According to Freddie Mac, PMI is “an added insurance policy for homeowners that protects the lender if you are unable to pay your mortgage.” By avoiding PMI, you can eliminate this additional monthly expense, giving you more financial breathing room.

Putting It All Together

When it comes to down payments, homeowners are in a unique position thanks to their equity. If you're considering selling your current home and moving, now is the perfect time to assess how much equity you have and how it can enhance your buying power in the current market.

What to Do Next

If you’re thinking about making a move, let’s connect and explore your options together. Understanding your home equity is the first step in unlocking the potential benefits that come with a larger down payment. Whether it’s buying your dream home or making a savvy investment, using your equity wisely can pave the way for a brighter financial future.

Bottom Line

Down payments are reaching record highs, primarily because homeowners are leveraging their recent equity gains. Don’t let misconceptions hold you back—seize this opportunity to maximize your buying potential. Together, we can navigate the market and find the perfect solution for your next home purchase!

Recent Posts

GET MORE INFORMATION