How Economic Trends Influence Mortgage Rates: What Homebuyers and Sellers Need to Know

If you’re navigating the real estate market, understanding how economic factors impact mortgage rates is crucial. The relationship between the economy and mortgage rates can seem complex, but grasping these dynamics can help you make more informed decisions. Curious about how the Federal Reserve's actions could affect your mortgage? Let's break it down and explore what’s ahead.

The Federal Funds Rate: The Key to Mortgage Rate Movements

Mortgage rates don’t fluctuate in a vacuum—they’re heavily influenced by broader economic policies, especially those set by the Federal Reserve. The Federal Funds Rate, the interest rate at which banks borrow money from each other, plays a pivotal role here. Although the Fed doesn’t set mortgage rates directly, their control over the Federal Funds Rate significantly impacts borrowing costs across the board.

Why Does This Matter? When the Fed adjusts the Federal Funds Rate, it alters the cost of borrowing for banks. This, in turn, affects mortgage rates. Lowering the Federal Funds Rate generally puts downward pressure on mortgage rates, making it cheaper to borrow money. So, when you hear news about the Fed meeting, it's worth paying attention to.

Three Crucial Metrics the Fed Watches

As the Fed considers whether to adjust the Federal Funds Rate, they closely monitor three key economic indicators:

- Inflation Rate

- Job Creation

- Unemployment Rate

Understanding these metrics can give you insights into potential changes in mortgage rates.

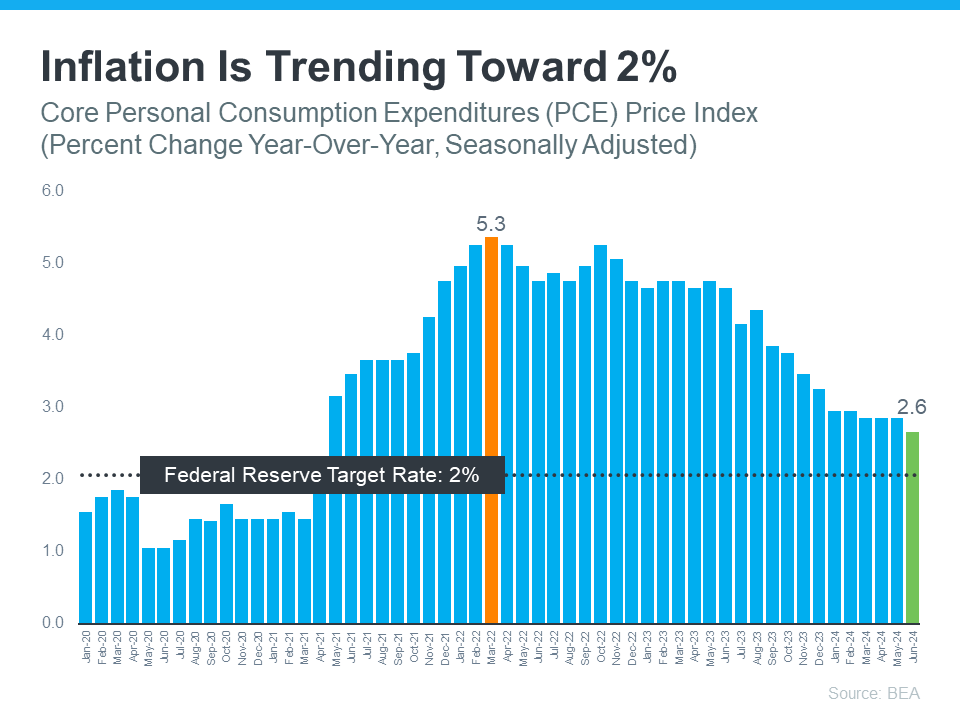

1. Inflation Rate: The Fed’s Primary Concern

Inflation is a hot topic lately, and for good reason. High inflation means prices are rising quickly, which affects everything from groceries to housing. The Fed aims to keep inflation at around 2%. Currently, inflation is above this target but showing signs of improvement.

What’s the Fed Doing? The Fed adjusts monetary policy to control inflation. If inflation is too high, they might raise the Federal Funds Rate to cool off the economy. Conversely, if inflation is decreasing and approaching the target, they might lower the rate to encourage borrowing and spending.

2. Job Creation: A Measure of Economic Health

Job creation is another critical metric. The Fed looks at how many new jobs are being added each month. A slowdown in job creation suggests the economy is cooling off, which can be a sign that it’s time to adjust the Federal Funds Rate.

What’s the Latest? Recent data show a slowdown in job growth. The Bureau of Labor Statistics reported that job creation in April and May was less robust than previously estimated, with sluggish hiring in June. This trend indicates that the economy is stabilizing, which aligns with the Fed’s goals.

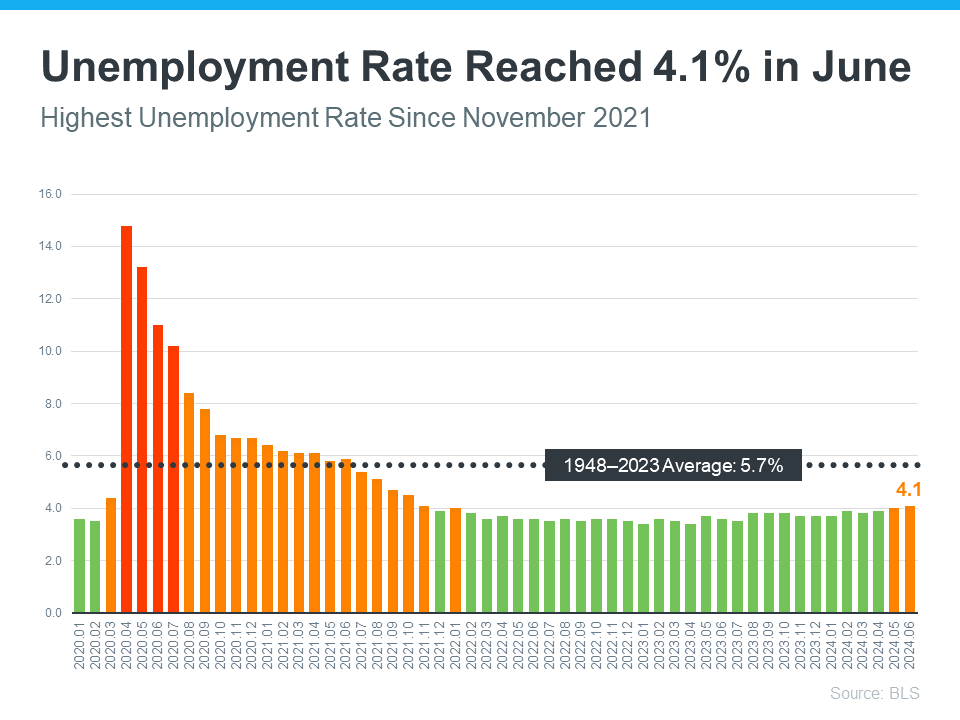

3. Unemployment Rate: A Double-Edged Sword

The unemployment rate is a key indicator of economic health. A low unemployment rate means many people are employed, which typically boosts spending and, consequently, inflation. While low unemployment is generally positive, it can also lead to higher inflation.

Current Trends? The unemployment rate is currently low but has been rising slightly. A gradually increasing unemployment rate might be seen as a sign that the economy is cooling down, which could prompt the Fed to consider lowering the Federal Funds Rate to stimulate economic activity.

What’s Next for Mortgage Rates?

Despite the current economic indicators, it’s unlikely that the Fed will make significant cuts to the Federal Funds Rate in their upcoming meeting. Fed Chair Jerome Powell has indicated that more data is needed to ensure that inflation is moving consistently toward the 2% target before they consider loosening policy.

Looking Ahead: According to the CME FedWatch Tool, there’s a high probability—96.1%—that the Fed might lower the Federal Funds Rate in their September meeting. However, this is contingent on continued positive economic trends. It’s important to remember that economic conditions can change due to new data or global events, so timing the market precisely can be challenging.

Why Timing the Market Can Be Risky

Trying to time the market based on Fed actions or economic forecasts can be risky. The economic landscape is influenced by many factors, and predictions can be uncertain. Instead, focusing on your personal financial situation and long-term goals is often a better strategy.

Bottom Line: Current economic trends suggest that mortgage rates might be on the path to becoming more favorable. However, it’s essential to stay informed and work with an expert who can help you navigate these changes. If you’re thinking about buying or selling a home, keeping up with these trends can help you make more informed decisions.

Need More Information? If you have questions about how these economic factors could impact your mortgage rates or if you’re ready to explore your options, let’s connect. I’m here to provide expert insights and help you stay updated on the latest trends.

Recent Posts

GET MORE INFORMATION