Mortgage Rates Plummet to Their Lowest in 18 Months: What It Means for You

Exciting news in the world of home buying: mortgage rates have just dropped to their lowest level in over a year and a half! If you’ve been biding your time on the sidelines, waiting for the perfect opportunity to jump into the housing market, this could be it.

Why This Rate Drop Matters

Even a minor dip in mortgage rates can significantly alter your monthly payments. But the recent decrease? It’s not minor at all. As Sam Khater, Chief Economist at Freddie Mac, puts it:

“Mortgage rates have fallen more than half a percent... and are at their lowest level since February 2023.”

So, how does this translate into real savings for you? Let’s break down the numbers and see how your monthly mortgage payment could benefit from this shift.

The Numbers Behind the Drop

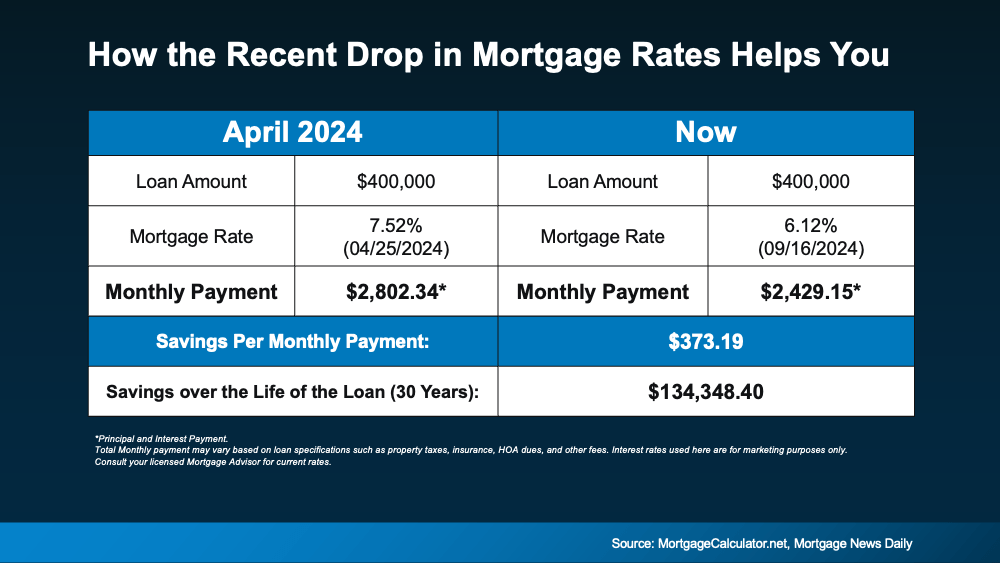

To illustrate the impact of this mortgage rate drop, let’s consider a $400,000 home loan. Back in April, when mortgage rates were peaking, the average rate hovered around 7.5%. Fast forward to today, and we’re looking at rates in the low 6s. What does this mean for your wallet?

Monthly Payment Comparison

Imagine purchasing that $400K home just a few months ago at a 7.5% interest rate. Your monthly payment for principal and interest would be significantly higher compared to the rates available now. In fact, that anticipated monthly payment has plummeted by over $370 in just a few months!

That’s a staggering amount. Think about what you could do with those savings: maybe treat yourself to a nice dinner, put it towards home improvements, or save for future investments.

Your Purchasing Power Has Increased

With mortgage rates now more favorable, your purchasing power is better than it’s been in nearly two years. This is a golden opportunity if you've been hesitant to dive into the real estate market.

What Can You Afford Now?

Let’s take a moment to consider how this rate drop affects the types of homes you can buy. Lower rates mean you might be able to afford a bigger home, a better location, or even features you didn’t think were possible within your budget.

For instance, if you were looking at homes that cost around $400K, you might now be able to stretch your budget and explore options in the $425K to $450K range without significantly impacting your monthly expenses.

What Should You Do Next?

Evaluate Your Financial Situation

Before making any decisions, take a hard look at your financial situation. Assess your budget, your credit score, and how much you can comfortably afford to spend each month on housing.

Get Pre-Approved

Once you’ve evaluated your finances, consider getting pre-approved for a mortgage. This not only gives you a better idea of how much you can borrow but also shows sellers you’re a serious buyer.

Explore Your Options

With these new rates, now is the time to explore different lenders and mortgage options. Don’t just settle for the first offer. Compare rates, terms, and closing costs to ensure you’re getting the best deal possible.

The Bottom Line

The recent dip in mortgage rates opens up a world of possibilities for homebuyers. With the potential for significant savings on your monthly payments, now is an excellent time to take action. Whether you're a first-time homebuyer or looking to upgrade your living situation, let’s discuss your options and make the most of this moment you’ve been waiting for.

Remember: The housing market is always changing, and it’s essential to stay informed. With the right information and a proactive approach, you can seize this opportunity and turn it into your dream home. So, are you ready to take that leap?

Recent Posts

GET MORE INFORMATION