Renting vs. Buying: The Wealth Gap You Can’t Ignore

When it comes to deciding whether to rent or buy a home, it’s easy to get caught up in the monthly numbers – rent payments, mortgage rates, and down payments. But there’s another critical factor you should be considering: your long-term financial future. One of the most compelling reasons to consider buying over renting is the impact it can have on your net worth.

Every few years, the Federal Reserve releases the Survey of Consumer Finances (SCF), a report that provides a snapshot of household wealth across the U.S. The findings reveal a staggering difference between homeowners’ and renters’ net worth, and this gap is growing.

So, if you’re torn between renting or buying, here’s why homeownership could be the key to growing your wealth.

The Huge Wealth Gap Between Homeowners and Renters

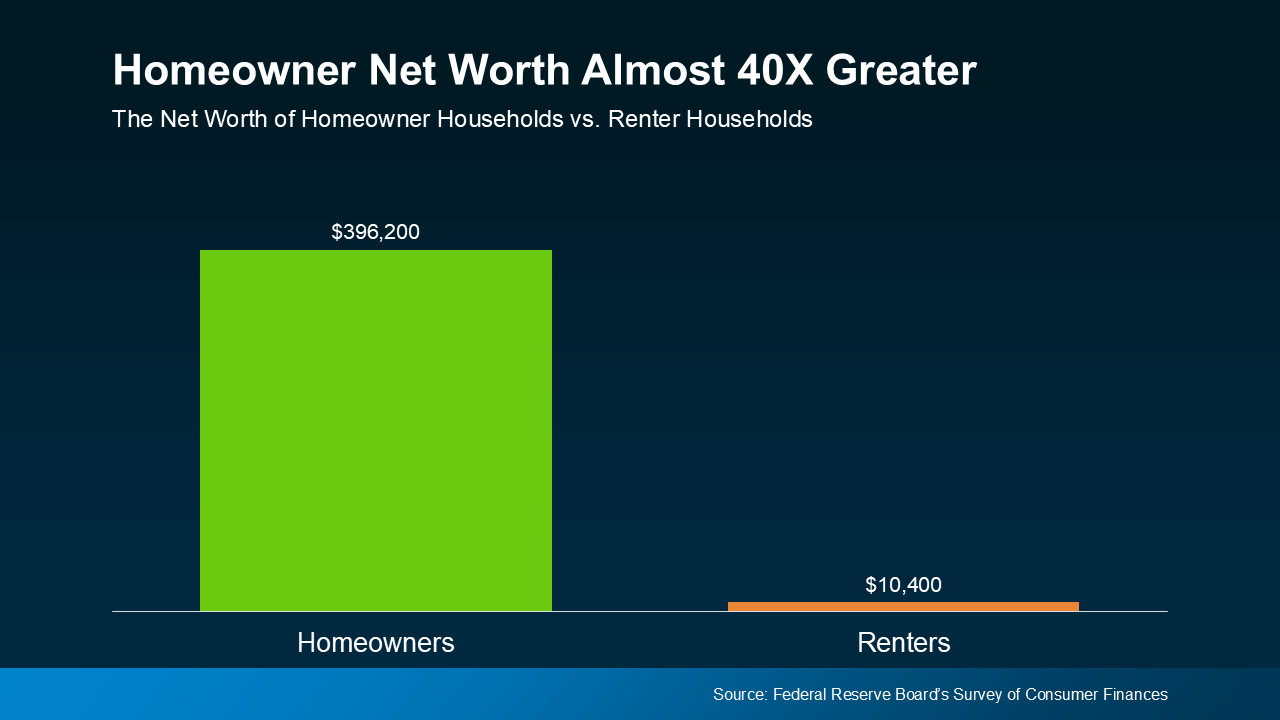

Let’s get right to the numbers. On average, a homeowner’s net worth is nearly 40 times greater than a renter’s. That’s a huge gap, and it’s only getting wider.

For example, in the most recent SCF report, the average homeowner’s net worth was $255,000. In comparison, renters had a net worth of just $6,300. This stark contrast highlights one of the most significant financial benefits of homeownership – the ability to build wealth over time.

Homeownership is not just about having a place to live. It’s a key driver of financial growth. With each mortgage payment, homeowners not only pay down their mortgage but also build equity in their property. This equity grows as home values increase, creating a powerful wealth-building tool.

Why Homeownership Grows Wealth Faster Than Renting

You might be asking, “Why is the difference between homeowners and renters’ net worth so large?” The answer comes down to one major factor: home equity.

Equity is the difference between your home’s market value and the amount you owe on your mortgage. As you pay down your mortgage and as your property appreciates in value, your equity increases. Over time, that equity can translate into a substantial increase in your net worth.

In recent years, home prices have surged. One of the primary reasons for this surge is the imbalance between supply and demand in the housing market. There simply haven’t been enough homes available to meet the needs of all the potential buyers, driving up prices and accelerating equity gains for homeowners.

If you’ve been watching the housing market lately, you’ve probably noticed that home prices are continuing to rise in many areas. Even though the rate of price growth is expected to moderate in the coming year, home prices are still expected to increase – meaning homeowners can expect to see continued equity growth.

The Power of Home Equity in Building Net Worth

Let’s take a closer look at how home equity works. If you purchased a home five years ago for $250,000, and today that same home is worth $300,000, you’ve gained $50,000 in equity – not including the money you’ve paid off on the mortgage. The equity you’ve gained is money that stays with you and contributes directly to your net worth. And over time, as home values continue to rise, your equity can grow significantly.

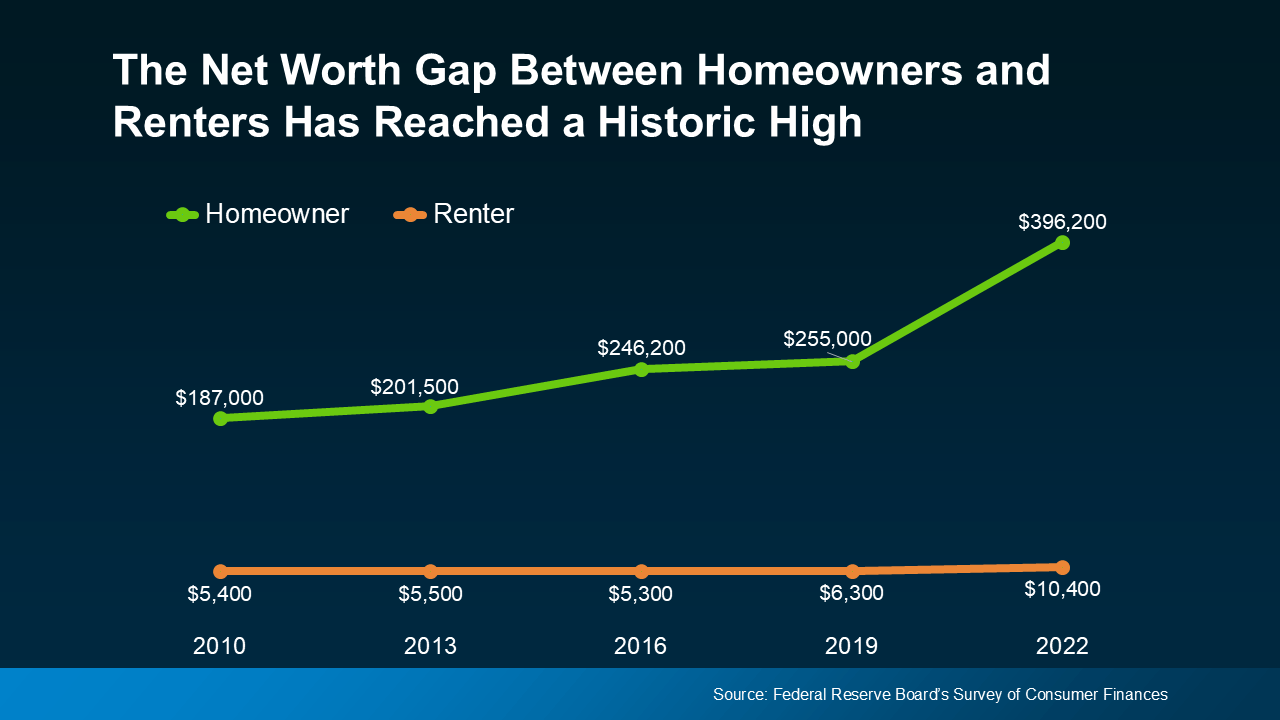

The recent growth in homeowner wealth is no accident. According to the SCF report, “The 2019-2022 growth in median net worth was the largest three-year increase in history, more than double the next-largest one on record.” This is largely due to the rapid increase in home prices over that period, as well as homeowners paying down their mortgages.

This increase in homeowner wealth is a clear indicator of how much potential homeownership has for building long-term financial security. So, if you’re wondering whether buying a home is worth it, the answer is often a resounding “yes” — especially if you plan to stay for a few years and watch your equity grow.

Is Homeownership Right for You? What to Consider

While homeownership can be an incredible way to build wealth, it’s not always the right decision for everyone. Factors like your financial stability, job security, and lifestyle goals should play a significant role in your decision.

For example, if you're planning to move frequently or don’t have the financial flexibility to handle a down payment and monthly mortgage payments, renting may be a better choice for you in the short term. However, if you're ready to settle down and start building long-term wealth, buying a home could be one of the best financial decisions you make.

One thing to keep in mind is that home prices and availability can vary widely depending on where you’re looking to buy. While inventory has grown this year, many areas still face housing shortages, which means prices will likely continue to rise. Experts predict that national home prices will increase again next year, albeit at a more moderate pace compared to the pandemic years.

The Local Market Impact: Why You Need Expert Advice

If you’re still undecided about whether to rent or buy, it’s important to get the right advice. Local real estate agents are invaluable resources when it comes to understanding your market’s specific trends and conditions. They can give you insights into what’s happening with home prices, inventory, and other financial factors that could impact your decision.

As Ksenia Potapov, an economist at First American, points out, “Despite the risk of volatility in the housing market, homeownership remains an important driver of wealth accumulation and the largest source of total wealth among most households.” In other words, even with fluctuations in the housing market, owning a home is still one of the best ways to build wealth over time.

A skilled real estate agent can also help you explore down payment assistance programs and other financial tools that can make buying a home more affordable. If homeownership feels out of reach, don’t be discouraged – there may be programs available that can help you get your foot in the door.

Weighing Renting vs. Buying: What You Need to Know

When it comes to deciding between renting or buying, there are several factors you should consider:

-

Financial Situation: Can you afford the upfront costs of homeownership, such as the down payment, closing costs, and monthly mortgage payments? If you’re financially stable, buying could be a wise choice.

-

Long-Term Financial Goals: If your goal is to build wealth and achieve long-term financial stability, homeownership can be an important tool in achieving those goals.

-

Flexibility: If you value the flexibility of moving around frequently or prefer not to deal with the responsibilities of home maintenance, renting may be the better option.

-

Local Market Conditions: Understanding your local housing market is crucial. A local agent can provide insights into whether buying now is a smart decision or if waiting might benefit you.

The Bottom Line: Owning a Home Can Build Lasting Wealth

If you’re unsure about whether to rent or buy, remember that homeownership is a powerful tool for building wealth. While renting may offer short-term flexibility, buying a home can be one of the best long-term financial decisions you can make. Over time, homeownership builds equity, grows your net worth, and provides stability that renting simply cannot offer.

Before making your decision, take the time to consider your financial situation, long-term goals, and the conditions of your local market. And if you're feeling unsure, reach out to a trusted real estate agent who can help guide you through the process and provide expert advice tailored to your needs.

At the end of the day, if you’re ready to make the leap into homeownership, there are plenty of resources available to help you make that dream a reality – and begin building your wealth for the future.

Recent Posts

GET MORE INFORMATION