When Will Mortgage Rates Drop? What You Need to Know About the Future of Rates

The question that’s on everyone's mind right now: when will mortgage rates come down? After years of rising rates, followed by some wild fluctuations in 2024, we’re all anxiously waiting for relief. The good news is that there is some hope on the horizon. While we can't predict exactly when or by how much mortgage rates will decrease, there are signs that things may ease up in the near future. So, what can we expect moving forward? Let’s break down the latest forecasts and the key factors that will influence the direction of mortgage rates in the coming year.

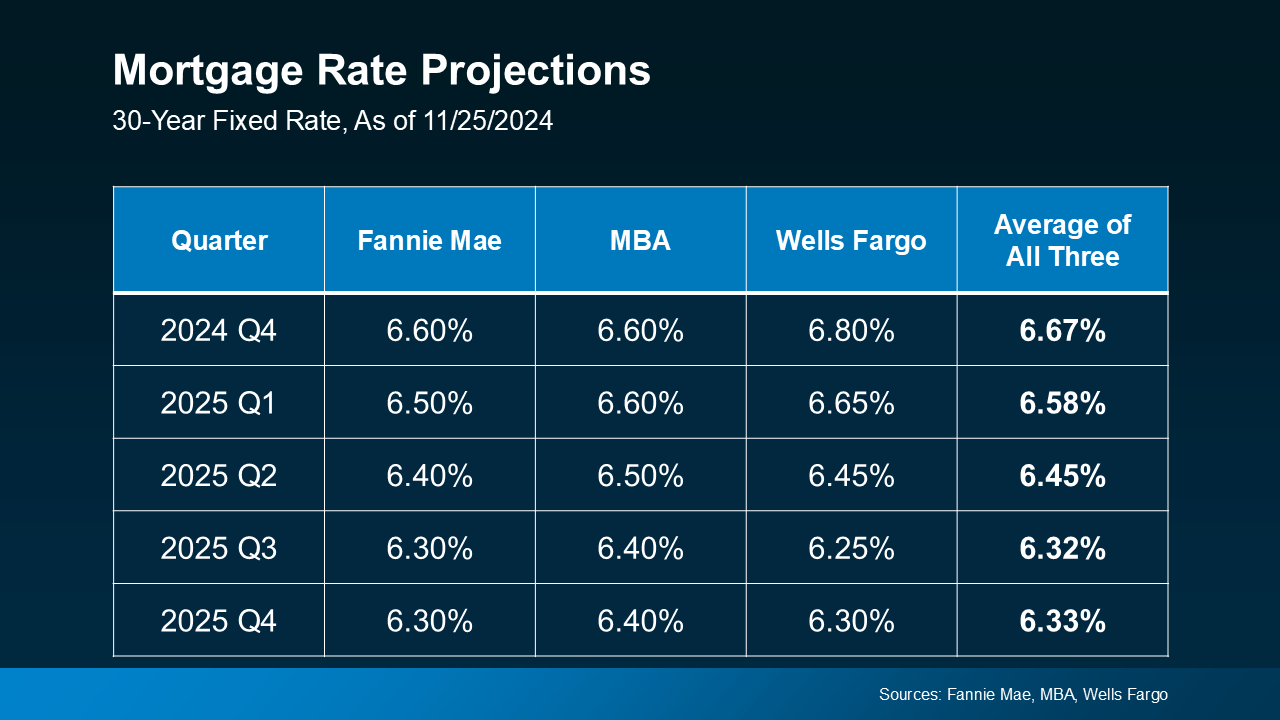

Will Mortgage Rates Drop in 2025?

The good news? Mortgage rates are expected to ease and stabilize over the next year, especially going into 2025. After several years of volatility, experts are cautiously optimistic that rates will come down slightly from their current levels. According to Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), while mortgage rates remain elevated for now, they are predicted to stabilize.

This means that we’re likely to see less unpredictability and a smoother transition into more favorable mortgage conditions, which could provide much-needed relief for potential homebuyers. While experts can’t pinpoint the exact timing of when rates will decrease, the forecast suggests that we might be entering a period of more steady, manageable rates.

What Drives Mortgage Rates?

When it comes to predicting mortgage rates, it’s not as simple as just looking at one factor. These rates are heavily influenced by a mix of economic conditions, government policies, and market forces. If you’re wondering why we can’t say exactly when rates will drop, it’s because there are several moving parts that need to line up perfectly. Let’s explore the most significant factors that will shape the future of mortgage rates.

1. Inflation: The Key to Rate Fluctuations

Inflation has been a major topic of discussion in recent years, and for good reason. It plays a pivotal role in interest rates, including mortgage rates. The Federal Reserve (the Fed) uses inflation as one of the primary drivers when making decisions about interest rates. If inflation starts to cool down and show signs of stabilization, we could see mortgage rates drop slightly.

However, if inflation remains high or starts creeping up again, rates may stay elevated for a longer period. Simply put, the Fed wants to keep inflation in check, and if inflation is stubborn, they may choose to maintain higher rates to cool the economy down.

2. The Unemployment Rate: A Barometer of Economic Health

Another crucial factor in determining mortgage rates is the unemployment rate. While the Fed doesn’t directly control mortgage rates, it does play a significant role in shaping overall economic conditions. If unemployment remains low, the economy is likely to be strong, and the Fed may choose to adjust its policies accordingly, potentially affecting interest rates.

If job growth slows or unemployment rises, the Fed may choose to lower rates in order to stimulate the economy. Changes in the unemployment rate can have a ripple effect on mortgage rates, making this an important factor to keep an eye on.

3. Government Policies and Political Factors

With a new administration taking office soon, government policies—especially fiscal and monetary policies—will play a role in shaping economic conditions and, by extension, mortgage rates. The government’s approach to managing inflation, employment, and overall economic stability could influence the Fed’s actions, which in turn could affect interest rates.

It’s important to note that while government policies and politics are unpredictable, they’re critical to understanding the broader economic landscape. If new policies focus on boosting the economy or controlling inflation, we could see mortgage rates respond accordingly.

The Roller Coaster of Economic Drivers

Predicting mortgage rates is no easy feat. After all, the market is constantly evolving, with new data emerging all the time. Even though experts offer their best guesses, there’s no way to guarantee exactly how rates will move in the future. Mortgage rates are inherently volatile and susceptible to changes in economic conditions.

As we’ve seen in recent years, small shifts in factors like inflation or unemployment can lead to noticeable changes in rates. So, while we can anticipate some easing in the near future, there’s still a level of uncertainty.

Instead of trying to time the market perfectly, it’s important to focus on what you can control today. With the right strategies, you can position yourself for success no matter what the market does.

How to Prepare for Changing Mortgage Rates

While no one can predict exactly when mortgage rates will drop, there are several steps you can take right now to prepare for the future and make the most of the current market conditions. Here’s how you can set yourself up for success, regardless of what happens with rates.

1. Work on Improving Your Credit Score

Your credit score plays a significant role in the mortgage rate you’ll qualify for. The higher your credit score, the more favorable your interest rate will likely be. So, if you’re planning to buy a home soon, it’s a good idea to focus on improving your credit score by:

- Paying off any outstanding debts

- Reducing your credit card balances

- Ensuring your credit report is accurate and free from errors

By boosting your credit score now, you can ensure that you’re ready for more favorable rates when they do arrive.

2. Save for a Larger Down Payment

Another key factor that can help you secure a better mortgage rate is the size of your down payment. A larger down payment not only reduces the amount you need to borrow but also shows lenders that you’re financially responsible. If you’re able to put down 20% or more, you may be able to avoid private mortgage insurance (PMI) and secure a more attractive interest rate.

If you’re not in a position to save a large sum just yet, don’t worry! You can still start saving today, even if it’s just a small amount each month. Over time, these contributions will add up and position you for success.

3. Automate Your Savings

If saving feels like an uphill battle, one of the best ways to stay on track is by automating your savings. Set up a separate savings account for your down payment fund and schedule automatic transfers each month. By making savings a consistent habit, you’ll be better prepared to take advantage of lower rates when they arrive.

4. Consult with a Trusted Mortgage Professional

Finally, it’s always a good idea to connect with a trusted lender or mortgage professional. They can provide you with the latest updates on the market and give you an expert opinion on what mortgage rates might do in the near future. Having a knowledgeable partner by your side ensures you stay informed and ready to make your move when the time is right.

The Bottom Line: Don’t Wait for the Perfect Timing

The reality is that no one can predict exactly when mortgage rates will drop, but we can expect some stability and potential easing in the near future. Instead of waiting for rates to hit a specific target, focus on what you can control—improve your credit score, save for a larger down payment, and stay informed.

If you’re ready to take the next step, don’t hesitate to reach out to a mortgage professional who can help you navigate the process and keep you up to date on the latest market trends. The right time to buy is the one that aligns with your financial goals and lifestyle, so get ready to make your move when the time feels right!

Are you ready to buy a home? Let’s connect and discuss how we can make the most of the current mortgage market conditions.

Recent Posts

GET MORE INFORMATION