Why Today’s Foreclosure Numbers Won’t Trigger a Housing Market Crash

The rising costs of living are enough to make anyone uneasy these days, and the worry that it could lead to a housing market crash is on many minds. With gas prices soaring, grocery bills climbing, and inflation hitting hard, it’s understandable to wonder if more homeowners might struggle to make their mortgage payments, potentially triggering a wave of foreclosures.

However, before you jump to conclusions and start envisioning another 2008-style housing market crash, take a deep breath. The latest data tells a different story—one that’s far more stable and reassuring than you might think. Let's dive into why today’s foreclosure numbers aren’t a cause for alarm.

The Key Differences Between Today’s Housing Market and 2008

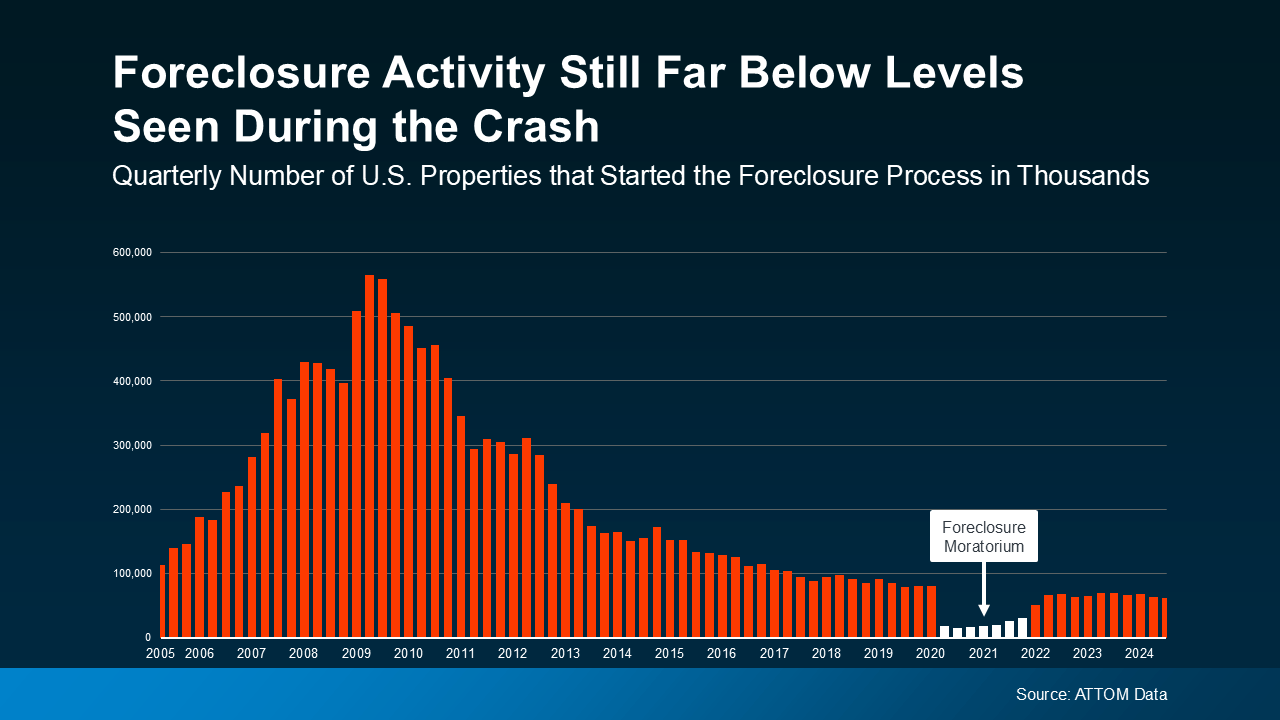

To understand why today’s market is so different from the 2008 housing crash, we need to take a step back and look at the bigger picture. The foreclosure numbers we’re seeing today are a far cry from the catastrophic spikes we experienced during the Great Recession. In fact, the current figures are significantly lower, and the latest reports even show a decrease.

The Foreclosure Surge of 2008: A Dark Chapter

Back in 2008, we saw a huge wave of foreclosures as a result of the housing bubble bursting. Lenders were handing out subprime mortgages like candy, and many homeowners found themselves in homes they couldn’t afford. As the economy crashed and home values plummeted, many homeowners owed more than their homes were worth. This led to a massive surge in foreclosures and a housing market that spiraled out of control.

Today’s Market: A More Resilient Landscape

Flash forward to today, and things are quite different. While it’s true that foreclosure filings have increased slightly since 2020, that’s primarily because of the moratorium put in place during the COVID-19 pandemic. The moratorium temporarily prevented foreclosures to give homeowners financial relief during a particularly difficult time. When that moratorium ended, foreclosure filings understandably ticked up—but they’re still nowhere near the levels seen during the height of the 2008 crisis.

According to research from ATTOM, a property data provider, the number of foreclosure filings has dropped significantly in recent years compared to the years following the housing crash. So, despite higher living costs, there’s no reason to panic about a foreclosure wave.

Homeowners Have More Equity, and That’s a Game Changer

So, why are foreclosures lower today despite the rising cost of living? The key factor is equity. Today’s homeowners are in a much stronger financial position than those who were caught in the 2008 crisis, largely because many of them have built up substantial equity in their homes.

The Power of Equity: A Safety Net for Homeowners

After the 2008 crash, millions of homeowners were underwater, meaning they owed more on their mortgages than their homes were worth. This led to a cascade of foreclosures, as people who couldn’t afford their mortgage payments had no way to sell their homes to recoup their losses. Home prices plummeted, and the foreclosure crisis deepened.

Fast forward to today, and the story is very different. Many homeowners have significant equity built up in their properties. In fact, a report from Bankrate points out that, unlike during the last housing crisis, most homeowners today have a “comfortable equity cushion.” This means that even if homeowners are facing financial hardship, they have more options to avoid foreclosure.

If someone is struggling to keep up with their mortgage payments, they can potentially sell their home and use the equity to pay off their mortgage and avoid the catastrophic consequences of foreclosure. In contrast, many homeowners during the 2008 crash had little to no equity, leaving them with few options.

Why Foreclosures Aren’t Likely to Surge Anytime Soon

You might still be wondering: If foreclosures aren’t surging today, what’s going to happen next? Will the rising cost of living and ongoing economic uncertainty eventually push homeowners over the edge?

While higher costs are undeniably a challenge, they are unlikely to trigger a massive wave of foreclosures. Here’s why:

1. More Homeowners Are in a Financially Stable Position

With mortgage rates still relatively low (though higher than they were a couple of years ago), many homeowners have locked in manageable payments. Furthermore, the increase in home values over the past several years has provided many people with significant equity in their properties, which gives them more financial breathing room.

2. Homeowners Have More Options to Avoid Foreclosure

Even if a homeowner struggles with their mortgage payments, they aren’t necessarily doomed to foreclosure. Today, there are more ways for people to avoid falling into foreclosure, whether by refinancing their loan, negotiating a payment plan with their lender, or even selling their home to cash out on their equity before things get worse.

3. The Market Isn’t as Volatile

Unlike the 2008 housing crash, today’s market isn’t as prone to sudden shocks. The housing market has been relatively stable in recent years, and while rising costs may make things tougher for some buyers, there isn’t the same level of risk that led to the 2008 crash.

What Does This Mean for Homebuyers and Sellers?

For homebuyers, the current market may feel like a tough one to navigate with rising interest rates and higher home prices. But it’s important to keep in mind that the likelihood of a housing market collapse or a wave of foreclosures is slim. The overall stability of the market means that there are still plenty of opportunities for buyers who are in a strong financial position.

For homeowners, the key takeaway is that, even though life is getting more expensive, your home is still a valuable asset. If you’re struggling with mortgage payments, remember that you may have more options than you think. Consider reaching out to your lender or a housing counselor to explore ways to avoid foreclosure.

Conclusion: No Need to Worry About a Foreclosure Crisis

In short, while rising living costs are undoubtedly a challenge, there’s no indication that we’re headed for another housing market crash. Homeowners today are in a much stronger financial position than they were during the 2008 crisis, thanks to substantial equity in their homes. Even if foreclosures have ticked up slightly since 2020, they are nowhere near the levels seen during the Great Recession.

The bottom line is this: While costs may be climbing, the housing market is not teetering on the brink of disaster. With a little caution and some forward planning, homeowners are in a much better position to weather the storm than they were in 2008. So, breathe easy—the current foreclosure numbers are nothing to be worried about.

Recent Posts

GET MORE INFORMATION