The Hidden VA Loan Benefit Most Veterans Don’t Know About

In this article, we’re going to uncover the VA loan benefit that many veterans don’t know about and explain why it’s crucial for veterans and their families to be fully aware of all their homebuying options.

What Is a VA Loan and Why Does It Matter?

If you’ve served in the military, the VA loan program can open the door to homeownership in ways that civilian loans simply can’t. The program was created to help veterans, active-duty service members, and certain surviving spouses achieve the dream of homeownership. Unlike traditional mortgages, VA loans offer low-interest rates, no down payments, and no private mortgage insurance (PMI), making them a financial lifeline for many who have served our country.

For over 79 years, these loans have helped countless veterans secure homes they otherwise may not have been able to afford. Yet despite its longevity and clear advantages, many veterans aren’t aware of the full extent of the benefits available to them.

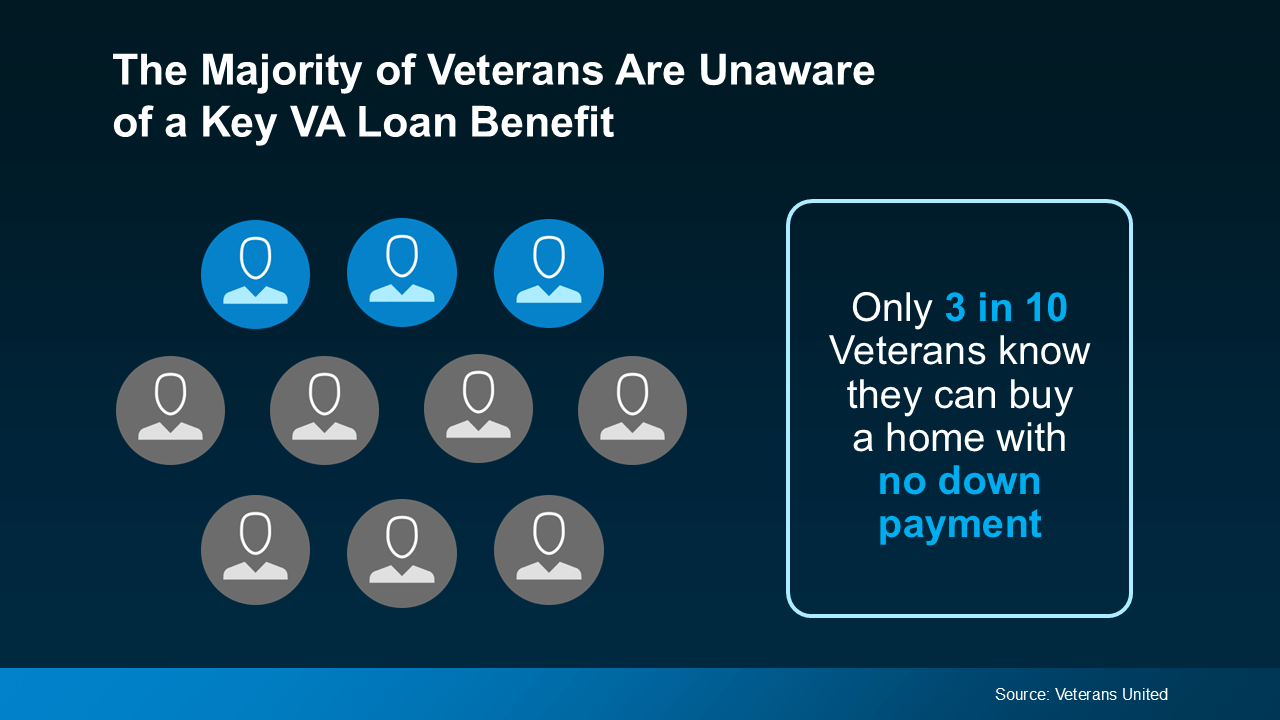

The Key VA Loan Benefit: No Down Payment Required

One of the most significant advantages of VA home loans is that they allow eligible veterans to buy a home without a down payment. While many civilian homebuyers must save for years to accumulate a sufficient down payment, the VA loan program removes this obstacle, making it easier and faster for veterans to become homeowners.

However, according to research by Veterans United, only about 30% of veterans are aware that they may be eligible for this no-money-down benefit. This lack of awareness can delay or even prevent veterans from pursuing homeownership altogether, despite having access to one of the most powerful financial tools available.

Why Are Veterans Unaware of This Benefit?

It’s puzzling that so many veterans don’t realize they’re eligible for this home loan benefit. There are a few possible reasons for this:

-

Misunderstandings About Eligibility: Many veterans might believe they don’t qualify because they haven’t served in combat or because they were in the military for a shorter period of time. The truth is, the eligibility requirements are often broader than many assume.

-

Not Fully Understanding the Program: Some veterans may have heard of VA loans but don’t fully understand the full range of benefits—like no down payment or lower interest rates—that come with them.

-

Lack of Awareness in the Community: Many veterans aren’t aware of the full array of resources available to them and don’t receive enough guidance or information on how to take advantage of them.

For veterans who are serious about homeownership, this gap in knowledge can be a missed opportunity to make their dreams of owning a home a reality.

Other Key Benefits of VA Home Loans

Beyond the ability to buy a home without a down payment, VA loans come with several other unique benefits that make them a powerful financial tool for veterans. Let’s explore these advantages:

Limited Closing Costs

When buying a home, closing costs can add up quickly, often creating a financial hurdle for prospective buyers. With VA loans, there are limits to the amount that can be charged for closing costs, saving you money when finalizing the sale of your home.

In addition, certain closing costs that are typically paid by buyers in other loan types (like appraisal fees or certain origination fees) may be covered by the seller, reducing your overall financial burden.

No Private Mortgage Insurance (PMI)

For many homebuyers, private mortgage insurance (PMI) is a necessary cost if they can’t make a large down payment. PMI is essentially an insurance policy for the lender in case the borrower defaults on the loan.

However, VA loans do not require PMI—even if you’re financing 100% of the home’s value. This can result in significant savings over the life of the loan, making your monthly payments lower and more affordable.

Competitive Interest Rates

Because the VA loan program is backed by the government, lenders are able to offer lower interest rates compared to conventional mortgages. This means that veterans can save a substantial amount of money in interest payments, making their long-term homeownership more affordable.

No Prepayment Penalties

Some loans come with penalties for paying off the mortgage early. However, VA loans don’t have prepayment penalties, allowing veterans to pay off their mortgage early without incurring any fees. This can save you money in interest over time if you decide to pay off your loan ahead of schedule.

The Path to Homeownership: How VA Loans Make It Easier

If you’re a veteran, you’ve already served our country. Now, it’s time for you to receive the benefits you deserve. If you’ve been wondering whether homeownership is possible without a large down payment or whether you could afford a mortgage, a VA loan might be exactly what you need to make that dream a reality.

While the process of buying a home can feel overwhelming, a trusted real estate agent and a VA loan specialist can help guide you through the steps and ensure you’re getting the best possible deal. Your team of professionals will walk you through everything from finding the right home to understanding how much house you can afford, making the homebuying process as smooth and stress-free as possible.

How to Know if You’re Eligible for a VA Loan

The eligibility criteria for a VA loan can vary depending on your service history and other factors, but generally, veterans who meet the following requirements may qualify:

- You have served at least 90 consecutive days of active service during wartime or 181 days during peacetime.

- You are an active-duty service member, a veteran, or a surviving spouse of a service member who died in service or as a result of service-connected disabilities.

- You have an honorable discharge or meet the service requirements outlined by the Department of Veterans Affairs.

If you're unsure whether you qualify, it’s easy to check your eligibility by visiting the Department of Veterans Affairs website or contacting a VA-approved lender. In many cases, veterans can also qualify for the loan if they have a less-than-perfect credit history, as the program is designed to help those who have served.

What to Do Next: Get in Touch with the Right Professionals

If you’re a veteran and you want to make homeownership a reality, now is the time to take action. Don’t let the lack of awareness keep you from accessing one of the best benefits available to you. Get in touch with a local real estate agent and a VA loan specialist who can help you explore your options and guide you through the homebuying process.

It’s crucial to have the right team in place, from understanding your eligibility to navigating the details of the loan itself. With the right support, you can buy a home with little to no down payment and start building a future in a place you can call your own.

Bottom Line: Don’t Miss Out on the VA Loan Advantage

The VA loan benefit is a powerful tool for veterans, and the fact that many are unaware of it is a missed opportunity for financial success. By taking full advantage of the program, you can secure a home without the stress of saving for a large down payment or dealing with costly private mortgage insurance.

If you’ve served our country, it’s time to leverage the benefits available to you. Get in touch with the right professionals today, and start making your homeownership dreams a reality. Don’t let this incredible opportunity slip through your fingers—take action now and build the future you deserve.

Recent Posts

GET MORE INFORMATION